Fed Raises Rates but Nods to Greater Uncertainty After Banking Stress

Officials voted unanimously to increase their benchmark short-term rate by a quarter percentage point

5 min

5 min")

The Federal Reserve approved another quarter-percentage-point interest-rate increase but signalled that banking-system turmoil might end its rate-rise campaign sooner than seemed likely two weeks ago.

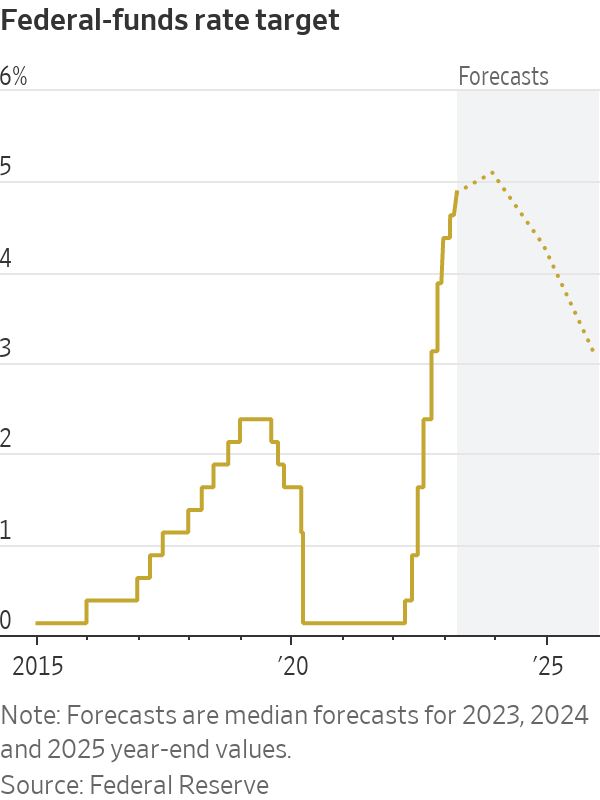

The decision Wednesday marked the Fed’s ninth consecutive rate increase aimed at battling inflation over the past year. It will bring its benchmark federal-funds rate to a range between 4.75% and 5%, the highest level since September 2007.

Officials sent a hint that they might be done raising interest rates soon in their post meeting policy statement. “The committee anticipates that some additional policy firming may be appropriate,” the statement said. Officials dropped a phrase used in their previous eight statements that said the committee anticipated “ongoing increases” in rates would be appropriate.

The policy statement said it was too soon to tell how much recent banking stress would slow the economy. “The U.S. banking system is sound and resilient,” the statement said. “Recent developments are likely to result in tighter credit conditions for households and businesses and to weigh on economic activity, hiring, and inflation. The extent of these effects is uncertain.”

All 11 voters on the rate-setting Federal Open Market Committee agreed to the decision.

New projections showed 17 out of 18 officials who participated in the meeting expect the fed-funds rate to rise to at least 5.1% and to stay there through December, implying one more quarter-point increase. The quarterly projections were little changed from those released in December.

Fed officials have at times over the past year acknowledged the risk of being forced to simultaneously fight two problems—financial instability and inflation. Several have said they would use emergency lending tools, along the lines of those unveiled this month, to stabilise credit markets so they could continue to raise interest rates or hold rates at higher levels to combat inflation.

At a news conference after the decision, Fed Chair Jerome Powell said officials had considered holding rates steady but opted to raise them given signs of still-high inflation and economic activity.

Various estimates of how much the banking stress could slow the economy amount to “guesswork, almost, at this point,” Mr. Powell said. “But we think it’s potentially quite real. And that argues for being alert as we go forward.”

That turmoil offers the strongest evidence yet of spillovers from higher interest rates to the broader economy. The upheaval has served as a stiff reminder of the perils Fed officials, regulators, lawmakers and the White House face trying to corral inflation that soared to a 40-year high last year.

U.S. policy makers cushioned the economic shock created by the Covid-19 pandemic in 2020 and 2021 by providing extensive financial aid and cheap money. Congress and the White House have largely delegated to the Fed the task of taming price pressures.

The fed-funds rate influences other borrowing costs throughout the economy, including rates on mortgages, credit cards and auto loans. The Fed has been raising rates to cool inflation by slowing economic growth. It believes those policy moves work through markets by tightening financial conditions, such as by raising borrowing costs or lowering prices of stocks and other assets.

Two weeks ago, Mr. Powell suggested officials would debate whether to raise rates by a quarter-point or a bigger half-point after reports showed hiring, spending and inflation were stronger early this year than they thought at the time of their Jan. 31-Feb. 1 meeting. “Nothing about the data suggests to me that we’ve tightened too much,” he said on March 7 before the Senate Banking Committee.

An astonishing run on the $200 billion Silicon Valley Bank changed everything. SVB’s depositors were heavily concentrated in the tight knit world of venture capital and startup firms, which were burning cash and withdrawing deposits as the once-highflying technology sector cooled.

On March 8, SVB said it was looking to raise capital from investors and that it would record a loss on longer-dated securities whose values had fallen as interest rates shot up. Nearly a quarter of the bank’s deposits fled over the next day and the bank was taken over by regulators on March 10.

To avoid a broader panic, federal authorities guaranteed the uninsured deposits of the California lender and a second institution, New York’s Signature Bank. The Fed also began offering loans of up to one year to banks on more generous terms as a precaution.

Banking-sector tremors are likely to lead to a pullback in lending because banks will face increased scrutiny from bank examiners and their own management teams to reduce risk taking. Banks could also see earnings squeezed if they feel pressure to raise deposit rates, which could further crimp lending.

That would mean fewer loans to consumers to buy cars, boats, homes and other big-ticket items, and less credit for businesses to hire, expand or invest, raising the risk of a steeper economic downturn.

Banks with fewer than $250 billion in assets account for roughly 50% of U.S. commercial and industrial lending, 60% of residential real estate lending, 80% of commercial real estate lending, and 45% of consumer lending, according to Goldman Sachs.

“I think we’re looking at a sizeable credit crunch,” said Daleep Singh, a former executive at the New York Fed who is now chief global economist at PGIM Fixed Income.

Since officials’ previous meeting, the economy had shown surprising strength, leading to concerns that aggressive rate rises over the previous year hadn’t done enough to slow the economy and lower inflation. Central bankers are concerned that prices will keep rising rapidly if consumers and businesses expect them to.

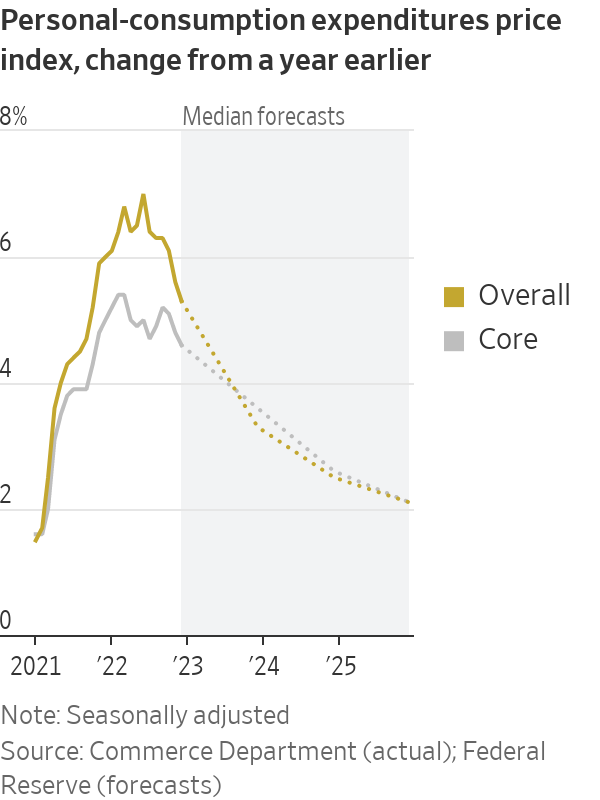

Inflation fell to 4.7% in January from 5.2% in September, as measured by the 12-month change in the personal-consumption expenditures price index excluding food and energy, the Fed’s preferred gauge. Economists expect the government to report next week that the inflation rate was unchanged in February.

Banking stress had led to questions in the past week over whether the Fed would even raise rates at all.

Some analysts fretted that a timeout on rate rises would risk so-called financial dominance, in which monetary policy becomes overly focused on avoiding market stress to the detriment of fighting inflation. A big market rally, in which stock prices rise and borrowing costs fall, could spur more demand and fan price pressures.

“They’d like to avoid that,” said William English, a former senior Fed economist who is a professor at Yale School of Management.

Others said the Fed would have been hard-pressed not to raise interest rates given recent strength in the economy and aggressive measures taken to shore up confidence in the banking system.

“Right now pausing would cause disruption,” said Donald Kohn, a former Fed vice chair. Deciding against raising rates would “signal that they don’t have confidence in their financial stability tools.”

Jan Hatzius, chief economist at Goldman Sachs, disagreed. It would have been better for the Fed to move cautiously given the highly uncertain environment that resulted from the banking stress, he said. “If more issues crop up after Wednesday, that’s also not going to be very confidence inspiring,” he said.

Fed officials have tried to signal their interest-rate moves deliberately over the past year to avoid the kind of market turmoil set off in 1994, when the Fed doubled its short-term benchmark rate from 3% to 6% in a 12-month span.

That rapid tightening hammered stocks and bonds and indirectly contributed to the demise of Kidder Peabody & Co., the bankruptcy of Orange County, Calif., and Mexico’s peso devaluation, which required a bailout from the U.S. and the International Monetary Fund.

After skipping on a rate increase in December 1994, as the peso crisis intensified, the Fed made a final rate increase in early 1995.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Chris Dixon, a partner who led the charge, says he has a ‘very long-term horizon’

Americans now think they need at least $1.25 million for retirement, a 20% increase from a year ago, according to a survey by Northwestern Mutual

The G80 Sport makes its entrance, displaying dynamic design details and elevated automative capabilities.

2 min

Juma Al Majid LLC, the exclusive dealer for Genesis in the UAE, has launched the G80 – a cutting-edge luxury sedan. Merging tradition with innovation, this model embodies Genesis‘ relentless pursuit of superior design, state-of-the-art technology, and unmatched luxury.

The new G80 marks a significant milestone in introducing Korean automotive excellence to the UAE, highlighting the brand’s commitment to providing exceptional experiences.

Meticulously crafted, the redesigned G80 adheres to the ‘Athletic Elegance’ design philosophy synonymous with Genesis. This luxury vehicle features refined details and cutting-edge specifications, combining comfort and style to elevate every driving experience to new heights.

“The debut of the all-new G80 in the UAE market propels our vision to converge advanced technology and refined elegance”, stated Suliman Al Zaben, Director of Genesis, UAE. “This launch is a step forward for Genesis in the UAE market and strengthens our efforts to offer ultimate luxury, innovation, and unique design to our incisive customer base.”

With a new dual-mesh design, the G80’s exterior enhances the sophisticated appearance of the Two-Line Crest Grille, paired with iconic Two-Line headlamps featuring Micro Lens Array (MLA) technology. This highlights Genesis’ commitment to harmonizing advanced technology with elegant design. The five 20-inch double-spoke wheels exude a dynamic aesthetic, resembling sleek aircraft lines, complementing the car’s parabolic side profile. Rear diffusers conceal mufflers adorned with distinctive V-shaped chrome trim inspired by the Crest Grille, embodying an eco-conscious ethos in today’s technology-driven era.

The G80 reinforces Genesis’ design philosophy in its interiors, inspired by the uniquely Korean concept of the Beauty of White Space, integrated with state-of-the-art technology to create cosmetic brilliance for users. The 27-inch-wide OLED display seamlessly combines the cluster and AVN (Audio, Video, Navigation) screen in a horizontal layout, extending to the center fascia, showcasing its flair for innovative technology. The touch-based HVAC (Heating, Ventilation, and Air Conditioning) system offers ease of control, while the redesigned crystal-like Shift By Wire (SBW) ensures a comfortable grip, infusing a sense of luxurious convenience.

With its dual-layered Crest Grille and expanded air intakes, the G80 Sport package delivers a dynamic and sporty spirit. Exclusive interior options, such as a D-cut steering wheel and carbon accents, enhance its sporty allure. Equipped with Rear Wheel Steering (RWS) and Electronic Limited Slip Differential (E-LSD), the G80 Sport 3.5 twin turbo model is built for stable control during high-speed maneuvers.

Fitted with advanced safety and convenience features, this luxury sedan includes Remote Smart Parking Assist 2, Lane Following Assist 2, and a Fingerprint Authentication System. The three-zone HVAC system provides customized climate control for all passengers. With two powertrain options – a 2.5 turbo engine delivering 300 horsepower and 43.0 kgf·m of torque, and a 3.5 twin turbo engine producing 375 horsepower and 54.0 kgf·m of torque – superior driving dynamics ensure a silent and luxurious driving experience.

Chris Dixon, a partner who led the charge, says he has a ‘very long-term horizon’

Americans now think they need at least $1.25 million for retirement, a 20% increase from a year ago, according to a survey by Northwestern Mutual