The Luxury Home Market Confronts Its New Reality: Not Enough Buyers and Sellers

Sales at the high end continue to decline, as homeowners pull back on listing properties and would-be buyers grapple with high interest rates and recession fears

8 min

8 min

When Joan Dangerfield, wife of the late comedian Rodney Dangerfield, first walked into her Los Angeles home in the early 2000s, she knew immediately that she would buy it. The Art Deco-style estate, perched in the coveted Bird Streets above L.A.’s Sunset Strip, had dramatic views spanning Downtown Los Angeles to the ocean and Catalina Island.

“I stepped 3 feet into the house and I knew it was the place for me,” said Dangerfield, who paid $6.25 million for the property. “It swept me away.”

Roughly two decades later, Dangerfield, 70, is trying to sell the home—and finding that would-be buyers aren’t as eager as she once was. The $17.8 million listing for her property has been active since February and while she has received several full-price offers, they have come with complicated contingencies, such as requiring her to provide seller financing, she said.

“I figured it would sell in a week, but didn’t quite work out that way,” she said of the house, which is comparably priced with other homes in the area. “It was a shock for me to just watch it sit there on the market.”

Luxury sellers across the country are finding themselves in similar circumstances, as the high-end real-estate market faces a perfect storm of rising interest rates, recession fears and population shifts in the wake of the Covid-19 pandemic.

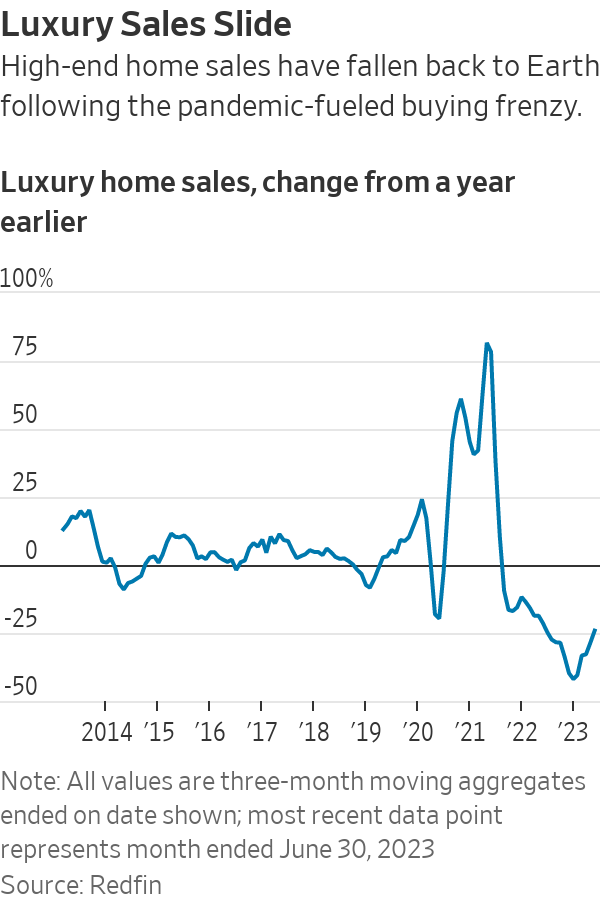

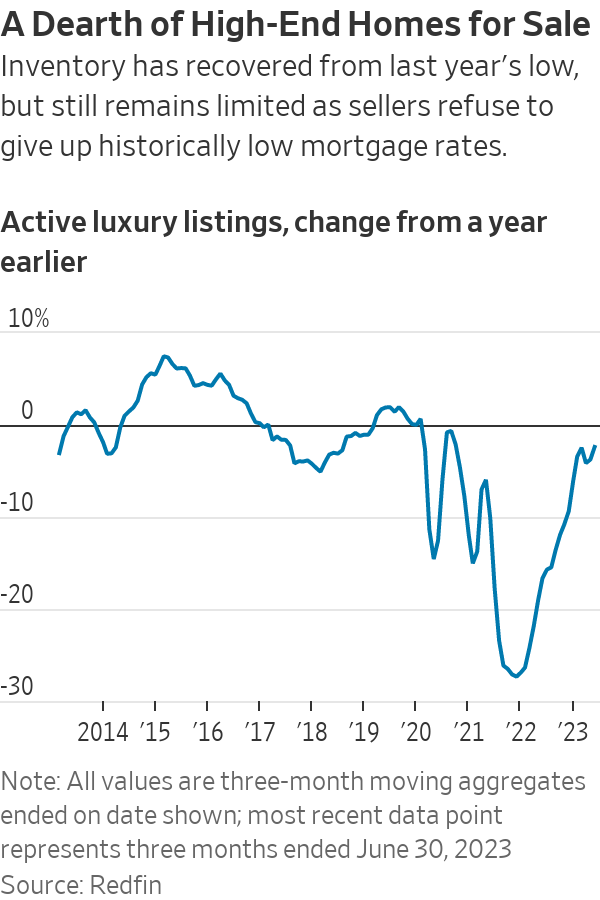

Sales of luxury homes nationwide, defined as the top 5% of homes based on estimated market value, declined by 24.13% in the three months ended June 30, compared with the same period last year, according to a new report by brokerage Redfin. Inventory of luxury homes was down 2.39% during that same period, while the median sales price for a luxury home was up by 4.55%. In many metros, homeowners appear to have pulled back on listing homes in light of the market shift. New luxury listings were down by 17.08% year-over-year in the three months ended June 30, Redfin’s data shows.

Sales of non luxury homes also fell during the same period, but that drop—19.42%—was smaller than the decline in the luxury market, according to Redfin.

“The luxury market is definitely hurting in terms of transactions,” said Daryl Fairweather, Redfin’s chief economist. “Even when you compare it to the rest of the market, it’s looking like luxury has really cooled off.”

The report marks the continuation of a market slide that began in earnest last spring, following an unprecedented deal-making frenzy during the pandemic. Redfin’s data shows that sales began to plummet significantly as early as June 2022, as buyers began to grapple with inflation and a volatile stock market. In the first quarter of 2023, luxury sales volume was down by 33.3% year-over-year.

Some of the biggest drops in sales volume over the three months ended June 30 were in markets that seemed unstoppable during the pandemic. The Miami metro area saw the largest drop in activity, for instance, with a 40.14% year-over-year reduction in luxury transaction volume for the three months ended June 30, according to Redfin.

Other metro areas with large drops included Nassau County on New York’s Long Island, where luxury sales volume dropped 39.34% year-over-year, followed by New York City, down 35.98%, Los Angeles, down 36.17%, and Chicago, which was down 34.13%.

Real-estate agents and industry experts said the luxury market’s performance has been uneven. That often comes down to pricing: In areas where sellers have capitulated to the declining market and dropped prices, transaction activity is holding relatively steady. But in markets where sellers are clinging to pandemic-era prices, activity has taken a nosedive.

In the San Francisco area, for instance, where median sales prices for luxury homes were down by 12.73%, there was only a 4.04% drop in transaction volume. “Because the prices have fallen, it’s opened up the opportunity for people who say, ‘I might finally be able to buy,’ ” Fairweather said.

In contrast, in markets like New York, Chicago and Los Angeles, prices have remained consistent or even risen slightly from last year, but transaction activity is way down. “There’s less demand, but it’s not enough of a pullback in demand to draw down prices,” Fairweather said.

In Miami, industry insiders say it is lack of supply, not lack of demand, that has caused the drop in activity. That’s thanks in large part to the mass migration to Miami and buying frenzy during Covid. “People who are going to sell have already sold,” Fairweather said, noting that new luxury listings in the Miami area were down by 33.1% year-over-year in the three months ended June 30. “There are definitely people who are moving to Miami who want to buy homes, but there are not necessarily homes for sale.”

Heigo Paartalu is among those buyers frustrated by a lack of inventory properties.

Paartalu, a Cigarette boat dealer and CEO of YachtWay, a digital boat show company, said he and his wife purchased a modern, five-bedroom house on Hibiscus Island, a gated island in Miami Beach, for $6 million in late 2021. The home value shot up 25% after about a year, so they cashed out and sold the house for $7.5 million in early 2023. Now, with a budget of around $10 million, they are looking for a waterfront property in the area without luck. “The inventory is very low and we’re not seeing the prices come down, which is what we were hoping for,” he said. The couple is currently renting in Miami’s Edgewater neighbourhood for $24,000 a month.

Jeff Miller of ONE Sotheby’s International Realty, Paartalu’s broker, said some homeowners aren’t selling because prices have gotten so high they won’t be able to buy something else in the area. Others don’t want to walk away from low mortgage rates. “It’s creating a huge shortage in our supply of available inventory and homes,” he said.

Even with a limited supply of inventory in Miami, Dina Goldentayer of Douglas Elliman said buyers have more leverage than they did last year for things like home inspections and closing credits. “I’m no longer taking the position of, ‘Take it or leave it,’ ” she said. “There are clear shifts that are making it seem like a normal market.”

In Los Angeles, the issues in the luxury market go far beyond an inventory crunch. Real-estate agent Juliette Hohnen of Douglas Elliman estimated that her business is down roughly 50% in that market from this time last year. At the height of the pandemic-fuelled market, she said, she had signed as many as 10 deals in a month. This July, she has only one so far. She chalked up the drop to rising interest rates, an outward migration from Los Angeles to lower-tax states, the introduction of a new mansion tax and more recently, the strike by both the actors’ and writers’ unions. She said she was slated to show an Oscar-winning writer around L.A. homes this month, but he called off his search in favour of renting amid the strikes.

The rising interest rates are keeping inventory low and stymying sales activity, Hohnen said. “Anyone who bought in the last few years has got these crazy low interest rates, usually between two and three percent,” she said. If those buyers sell now, they’ll be incurring rates that are almost double and potentially taking a loss on the sale.

Hohnen said she bought a $2.525 million home in 2021 in the Sag Harbor area of the Hamptons, securing an interest rate of just 1.875% for an adjustable-rate mortgage. Normally, she would buy, renovate and flip, but not this time, she said. “I’m never going to sell that house. I could never afford it if I was buying now. The monthly expenses on a new house would be too high.”

Dangerfield said she didn’t foresee how detrimental the mansion tax would be for her home’s prospects. The new measure, which was implemented April 1, requires sellers to pay 4% on sales of homes priced between $5 million and $10 million, and 5.5% on sales of properties at $10 million or above. “We were flooded with shoppers in March. Then, things just came to a screeching halt. It was such a change in the amount of people coming to view the home that it felt like it wasn’t even on the market,” she said.

One of Dangerfield’s agents, Marcy Roth of the Eklund Gomes team at Douglas Elliman, said the ULA tax “tainted buyer sentiment,” especially when combined with other issues like rising interest rates. “Everything is muddy and offers are complicated,” she said. “There aren’t a lot of quick, clean deals.”

In Chicago, real-estate agent Katherine Malkin of Compass said the city’s downtown area and so-called Gold Coast have been most affected by the slowdown. She said quality of life concerns like crime and an outward migration of some of the city’s businesses has put a damper on sales. Citadel, for instance, the hedge fund headed by billionaire Ken Griffin, recently left the city and moved to Miami. Other businesses that recently relocated their headquarters from Chicago include Boeing.

“You have businesses that are leaving because of the taxes,” Malkin said, noting that some prominent Chicago philanthropists and entrepreneurs have also left the city in the past few years. “They went to Florida, they went to Texas, they went to states that had a much lower tax circumstance. That’s been a difficult thing for people to grasp.”

Some sellers, Malkin said, have been reluctant to lower prices significantly—median luxury sales prices were actually up by more than 6.82% in Chicago in the three months ended June 30—which has been a further drag on sales. “No person of means wants to give their property away when they feel that they’ve invested in it,” she said.

When sellers have capitulated to the market, it has led to activity, Malkin said. She said one of her clients, who public records identify as private-equity executive John Weaver “Jay” Jordan II, recently lowered the price of a roughly 20,000-square-foot townhome in the Gold Coast neighbourhood to $15.75 million from the $18.75 million it listed for in 2020. While the home hasn’t yet sold, the price cut resulted in a new wave of interest, Malkin said. Jordan, who paid $1.8 million for the house in 1996 and remodelled it extensively, didn’t respond to a request for comment.

Although luxury median sale prices in the New York metro area are up by 7.69% for the three months ended June 30 compared with the year-earlier period, the slower pace of sales has allowed some opportunistic buyers to ink great deals. Vanessa Lucin of the Corcoran Group recently worked with buyers who paid $6 million for an Upper West Side apartment that was first listed for $7.495 million in June 2022. The roughly 3,383-square-foot apartment has two private balconies and is currently configured as a four bedroom, according to StreetEasy. Lucin said the couple is relocating to New York from California and began searching in January, when the market had slowed from its Covid peak. “There was another offer on the table but it wasn’t going anywhere,” she said.

Daniel Parker, co-head of Compass New Development Marketing Group, said some recent condo closings reflect deals struck during the more robust market in 2021 and 2022. In pockets of the city, such as Billionaires’ Row and Hudson Yards, developers have offered significant discounts. “They are embracing the market we have rather than the market they wish we had,” he said.

However, there are signs of life. Agents in New York reported a recent pickup in big-ticket deals this summer; in particular, large downtown condos have been the “golden sweet spot” of the market, said luxury real-estate agent Donna Olshan. A string of mega deals downtown over the past few weeks include the $52 million off-market sale of a penthouse at 150 Charles Street, the $50 million off-market sale of penthouse at 151 Wooster Street, and a signed contract for a penthouse asking $52 million at One High Line in Chelsea.

Sylvia Hughes, Lucin’s client, said she and her husband, John Hughes, saw several apartments before making an offer on their new four-bedroom on the Upper West Side. “I think the seller was motivated. This apartment had languished,” she said. By the time they saw it, the original $7.495 million asking price had been reduced to $6.195 million and their offer of $6 million was accepted. “I was beginning to wonder if we should have offered less.”

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

KnowBe4 and AWS have signed a multi-year strategic agreement to strengthen digital workforce security, helping organizations protect both employees and AI agents while simplifying the deployment of cybersecurity solutions through AWS Marketplace.

Don’t just hear about the future of longevity, experience it. Revive ME returns to Abu Dhabi, bringing together the innovators, leaders, investors, policymakers, and visionaries shaping the next era of healthy lifespan. This is where breakthrough science meets transformative innovation. Where meaningful conversations spark collaboration, new ideas become actionable opportunities, and the global longevity ecosystem comes together under one roof.

A coalition of 12 U.S. attorneys general has filed a lawsuit seeking to block Paramount Skydance’s proposed $110 billion acquisition of Warner Bros. Discovery, arguing the deal would reduce competition in the entertainment industry. Paramount says the merger would strengthen its ability to compete with streaming giants such as Netflix. Read more via the link in our bio.

Spain defeated defending champions Argentina 1-0 after extra time to lift their second FIFA World Cup title. Ferran Torres’ decisive goal sealed victory in a dominant display, ending Lionel Messi’s World Cup career and capping Spain’s remarkable era as reigning world, European and Olympic champions.

4 min

Ninety minutes of the World Cup final had come and gone, and Argentina—the defending champion, unbeaten at any major tournament since 2019, and blessed by the existence of Lionel Messi—hadn’t managed a single shot.

And yet, on a baking afternoon in front of a hostile crowd, a vastly superior Spain couldn’t find a way to punish them. Even when Argentina was reduced to 10 men, the wave of Spanish jerseys kept crashing into the same resolute defense. Nerves crept in, and as the match entered extra time, Spain began to fear that this final would go down as un robo, a robbery.

Instead, it will be retold as something far more epic than that. This was the day when Spain downed Argentina 1-0 and won the World Cup for the second time.

“Even against 10 men at the end we had to suffer,” Spain coach Luis De La Fuente said. “But, we like to suffer, and I’ll say it again, we were prepared for everything.”

Sixteen years after first lifting the trophy in South Africa, La Roja demonstrated without a doubt that no country commands the world’s most popular sport quite like Spain. With an approach so complete, so technically sound that its players look permanently untroubled, they have shown the world how it looks when cool competence is elevated to high art.

It’s no coincidence that Spain is now a simultaneous Olympic, European, and world champion, or that it currently holds both the men’s and women’s World Cups. This is a nation that has worked out how to develop soccer players as plentifully as it grows oranges and lemons.

When the breakthrough finally came, it arrived with Spain’s 20th shot of the match. After 104 games, the largest World Cup in history had required an extra half-hour to decide its champion and now, in the 16th minute of extra time, Ferran Torres was the man to enter the history books. After a high ball to the back post, headed down by Nico Williams, the 26-year-old Torres lashed it home.

This was the one effort that Argentina goalkeeper Emiliano Martinez, who set a World Cup final record for saves, couldn’t keep out.

But if Spain’s tactics revolved around control, patience, and invention, Argentina’s approach to Sunday focused more squarely on intimidation. And with a permissive referee running the show, Argentina took every inch of latitude—at least until Enzo Fernandez was ejected in second-half stoppage time for a second yellow card.

Over 120 minutes, the defending champions produced just one shot on target but committed 25 fouls. And Messi found himself with precious little to work with—in the first 15 minutes, he had touched the ball just once on the opening kickoff.

Back in 2010, the Netherlands had tried a similar tack against Spain in a World Cup final. Faced with a peak version of the pretty-passing, high-possession, tiki-taka style, the Dutch realized that they simply couldn’t out-soccer La Roja. Their response was to make the match as physical as possible and hope for the best. That time, Spain found a winner in the 26th minute of extra time.

On Sunday, the decisive moment arrived slightly earlier, as the center of the soccer universe migrated to an NFL bowl in a New Jersey parking lot. All at once, it contained President Trump, the King of Spain, and half the royalty of American entertainment.

Mostly, though, the stands heaved with fans from Argentina. Just as they did in Qatar—and more recently in Atlanta and Dallas and Kansas City—supporters in sky blue and white swarmed the stadium, outnumbering Spain fans by at least three-to-one. This is a country where adoration of the national team is so fervent that many fans build their financial planning around the World Cup, taking out loans to buy tickets every four years. It’s also the country with the most psychologists per capita in the world. These facts are perhaps not unrelated.

“The fans are absolutely crazy, different to other countries,” Argentina’s Martinez said before the game. “Seeing them celebrate at 2 a.m. in the cold Argentine weather means a lot.”

But there would be no repeat of those scenes on Sunday night as it lost a World Cup final for the fourth time in its history. Instead, Argentina could only look on as Messi’s World Cup career came to a close with his second defeat in three finals, 12 years after losing his first against Germany.

Only now, the country that defined Messi’s club career over two decades at FC Barcelona, was the one doling out the punishment.

New research suggests that bonuses make employees feel more like a mere cog in a wheel.

Paine Schwartz joins BERO as a new investor as the year-old company seeks to triple sales.

Customers can now configure their ideal BMW through natural conversations using the new BMW plugin in ChatGPT. Instead of navigating menus, users simply describe what they’re looking for—whether it’s performance, space, all-wheel drive, or budget—and receive personalized vehicle and configuration recommendations. The AI can refine options, compare models, and link directly to the BMW Configurator or similar in-stock vehicles, making the car-buying journey faster and more intuitive.

2 min

BMW is expanding its digital customer communications by making its vehicle configurator available directly via OpenAI’s ChatGPT. Using the BMW plugin in ChatGPT, customers can now engage in a natural conversation to configure their dream car. The plugin combines the dialogue capabilities of generative AI with the BMW product and configuration knowledge base, and is available on both mobile devices and desktop computers.

Dialogues rather than menu navigation.

Generative artificial intelligence is changing the way people search for information online and make decisions. Dialogue-based systems are increasingly replacing traditional navigation via search engines or websites. Picking up on this trend, BMW is the first car manufacturer to offer digital vehicle advice directly via ChatGPT.

Generative AI meets BMW knowledge base.

The BMW plugin in ChatGPT is focused on AI dialogues. Instead of step-by-step navigation through menus and submenus, users describe their requirements in natural language – for example, in terms of spaciousness, ground clearance, powertrain or intended use. They are then given suggestions of suitable models and configurations based on this information. This also makes it very easy to compare different configurations.

The recommendations can be adjusted, compared and refined at any time in the dialogue. Factors like running costs, driving dynamics, colour, model or all-wheel drive can be specifically taken into account during the consultation. For complex specification requirements in particular, dialogue-based interaction opens up new, easy and intuitive ways to refine individual vehicle configurations. The desired vehicle specification can then be opened in the BMW Configurator. Customers can also view stock vehicles that have a similar spec.

All recommendations are based on the latest BMW Configurator data. Should any questions arise that go beyond its database, ChatGPT can also access up-to-date information from the internet, to the extent the relevant functions are available and enabled.

Easy access via ChatGPT.

The BMW plugin is integrated directly into ChatGPT. On chatgpt.com, it can be accessed by going to the “Plugins” menu item and then searching for “BMW”. On mobile devices, access is much the same when logged in, via the “Plugins” option in the main menu.

Following the successful launch of its Palais Collection, MAISON de SABRÉ has unveiled a new modular handbag system offering more than 720 styling combinations.

The sports-car maker delivered 279,449 cars last year, down from 310,718 in 2024.

Parents and educators across the United States are increasingly calling for the return of longer school recess periods, as growing evidence highlights their role in improving children’s mental well-being, concentration, and social development. With several states introducing laws to expand recess time, experts argue that play is no longer a luxury but a fundamental part of learning and academic success.

4 min

When Kathryn Truman’s son Sawyer enrolled in kindergarten, she was surprised to discover his school only gave him 20 minutes of recess a day. The 40-year-old nurse worried he wouldn’t get enough of a mental and physical break.

Truman wasn’t the only one who felt this way. She teamed with other parents to help revive recess throughout Tennessee, which went on to pass a law last year requiring at least 40 minutes of recess in elementary schools. Now, Truman is looking to expand recess in middle schools and helps lead a nonprofit—Say Yes to Recess—with chapters in 20 states.

“Of course we want our kids to be good at math and reading, but what kind of people will they grow up to be? That’s determined at recess,” said Truman, explaining the benefits for children’s social development.

In Michigan, Shanel Talbert said she got involved in the fight for recess when her daughter’s elementary school reduced it last year. While her daughter wasn’t struggling academically, Talbert could see that she was burned out from her seven-hour school day.

Talbert and other parents launched a petition, calling for at least 60 minutes of recess, that has garnered over 1,300 signatures. They are working with a state legislator on a bill that would require 40 minutes of recess in elementary school, which Talbert said they thought was more likely to pass.

Morning and afternoon recesses were common in U.S. elementary schools during the post-World War II decades. But as pressure mounted on schools to improve test performance in the 2000s, many reduced or eliminated recess in favor of more instructional time in subjects such as reading and math. States often prescribe minimum instructional hours, and recess generally doesn’t count.

Chicago Public Schools was among the first big-city school districts to restore daily recess in 2012, after many of its elementary schools did away with it. But the effort was slow to catch on broadly.

Pediatricians have been sounding the alarm, saying recess has both mental and physical benefits. In May, the American Academy of Pediatrics expanded its endorsement of recess beyond elementary schools to include middle and high schools. Research suggests that at least 20 minutes a day with multiple breaks is best, the AAP says.

Catherine Ramstetter, co-author of that recommendation, said recess helps children remember information and learn better. It also allows young children to develop interpersonal skills.

Ramstetter upholds the Finnish model in which students typically get 15 minutes of recess multiple times a day. “The importance of recess as time to connect with one another cannot be understated,” she said. “Adults ideally are not intervening in the play but close by so they can intervene when necessary.”

In Oklahoma, legislators recently pushed for more recess time as part of an effort to improve learning and test results that has also included banning cellphones during school and emphasizing phonics, according to Republican state Sen. Ally Seifried.

Seifried drafted a law that passed in April requiring 40 minutes of daily recess in kindergarten through fifth grade, up from 20 minutes. “Parents who had little boys definitely recognized the importance of this,” she said.

Krissy West, a school physical therapist and mother from New Hampshire, started advocating for more recess last year, after seeing her daughter Daisy get overwhelmed, sometimes resulting in tantrums after school.

“She would say that [her] whole body is just ready to run,” said West. As a coping mechanism later on, her daughter, now 10 years old, would ask the teacher for permission to take bathroom breaks, time she would then use to take a walk through the hallways.

A bill West championed, which would have required 45 to 60 minutes of recess for K-6 students, was defeated on New Hampshire’s House floor earlier this year amid concerns it would violate existing teacher contracts by requiring extra staff.

The “Say Yes to Recess” initiative calls for at least 60 minutes of screen-free time daily when children get to pick their activities, and that it isn’t withheld as punishment. The hourlong recommendation is based on research from Texas Christian University on the optimal time needed for children to reduce stress and anxiety, improve test scores and fight obesity.

West and other parents have helped push for change locally at Valley View Community School in Farmington, N.H. This past academic year, the elementary school added a 25-minute recess block starting from 7:30 a.m., when parents can drop their children off. The start of classes was moved 10 minutes later to help accommodate it.

West said recess first thing in the day isn’t ideal and noted part of it became optional in practice because some children wouldn’t arrive until later. But she is encouraged that the school is trying to find solutions.

The school’s principal, Mark Dangora, said adding more downtime is still a work in progress. He is trying to bring daily recess time to a total of 50-55 minutes. Losing a bit of class time, so far, hasn’t affected learning, he said.

“Children need play,” said Dangora.

Two coming 2027 models – the first of the “Neue Klasse” cars coming to the U.S. early next year – have been revealed.

Parts for iPhones to cost more owing to surging demand from AI companies.

KnowBe4 and AWS have signed a multi-year strategic agreement to strengthen digital workforce security, helping organizations protect both employees and AI agents while simplifying the deployment of cybersecurity solutions through AWS Marketplace.

< 1 minKnowBe4, a leader in digital workforce security, securing both AI agents and humans, today announced it has signed a multi-year strategic collaboration agreement (SCA) with Amazon Web Services (AWS) to help organizations worldwide adapt to an evolving cybersecurity landscape, while simplifying how they procure, deploy and scale security solutions.

As cyber threats become more sophisticated and AI adoption accelerates, workforces are expanding to include both humans and AI agents. At the same time, security teams are under pressure to improve outcomes and operate more efficiently. By accessing KnowBe4’s industry-leading portfolio in AWS Marketplace, customers can streamline procurement and accelerate deployment at a time when speed is more critical than ever.

“Today’s workforce consists of both humans and AI agents working side by side, and securing both is the defining challenge of this moment,” said Marco Muto, SVP of Strategy at KnowBe4. “This agreement reflects a shared commitment from KnowBe4 and AWS to meet that challenge together. We’re jointly investing in the go-to-market, our technology, and the broader industry ecosystem to ensure our customers have what they need to stay ahead of an evolving threat landscape. When two industry leaders align around a common mission, customers win.”

KnowBe4 will collaborate with AWS on global go-to-market initiatives, sales enablement and customer adoption programs designed to help organizations proactively manage risk across their evolving workforce while simplifying procurement in AWS Marketplace. It also creates new opportunities for KnowBe4’s global ecosystem of channel partners, helping to align security investments with broader cloud strategies.

Following the successful launch of its Palais Collection, MAISON de SABRÉ has unveiled a new modular handbag system offering more than 720 styling combinations.

Many of the most-important events have slipped from our collective memories. But their impacts live on.

Don’t just hear about the future of longevity, experience it. Revive ME returns to Abu Dhabi, bringing together the innovators, leaders, investors, policymakers, and visionaries shaping the next era of healthy lifespan. This is where breakthrough science meets transformative innovation. Where meaningful conversations spark collaboration, new ideas become actionable opportunities, and the global longevity ecosystem comes together under one roof.

< 1 minAbu Dhabi will welcome healthcare innovators, investors, policymakers, researchers, and technology leaders when Revive ME 2026 returns to ADNEC Marina on 11–12 November 2026, bringing together the latest advances in longevity science, regenerative medicine, biotechnology, AI-powered healthcare, and personalised wellness.

Positioned as the Middle East’s premier longevity and health technology exhibition and conference, the two-day event aims to showcase how scientific breakthroughs and emerging technologies are transforming the future of healthy ageing. Building on the success of its inaugural edition, Revive ME 2026 will provide a platform for collaboration between clinicians, startups, investors, research institutions, healthcare providers, and government stakeholders to accelerate innovation across the sector.

Visitors can expect an extensive exhibition featuring next-generation health technologies, live product demonstrations, expert-led conference sessions, startup showcases, networking opportunities, and discussions exploring the future of preventive healthcare, precision medicine, regenerative therapies, digital health, biotechnology, and artificial intelligence. The event is designed to foster partnerships that drive innovation while addressing one of healthcare’s fastest-growing global priorities: extending healthy lifespan.

As governments and private sector organisations continue investing in healthcare innovation, events such as Revive ME reinforce Abu Dhabi’s position as a regional hub for medical technology, life sciences, and future-focused healthcare solutions. By bringing together global experts under one roof, the exhibition seeks to encourage knowledge exchange, investment, and cross-sector collaboration that can shape the next generation of health and wellness technologies.

Registration for Revive ME 2026 is now open.

Following the successful launch of its Palais Collection, MAISON de SABRÉ has unveiled a new modular handbag system offering more than 720 styling combinations.

Chris Dixon, a partner who led the charge, says he has a ‘very long-term horizon’

A coalition of 12 U.S. attorneys general has filed a lawsuit seeking to block Paramount Skydance’s proposed $110 billion acquisition of Warner Bros. Discovery, arguing the deal would reduce competition in the entertainment industry. Paramount says the merger would strengthen its ability to compete with streaming giants such as Netflix. Read more via the link in our bio.

< 1 minParamount Skydance won’t be able to buy Warner Bros. Discovery without a fight.

California Attorney General Rob Bonta said Monday he is leading a coalition of 12 attorneys general filing a lawsuit challenging the $110 billion acquisition of Warner Bros. by Paramount.

The complaint alleges the merged companies would control about one-third of theatrical motion pictures, and nearly one-third of basic cable programming. That would inflict “substantial harm on movie theaters, basic cable distributors and, ultimately, audiences nationwide.”

“Consolidation here not only leads to higher prices—it also leads to fewer opportunities for important stories to come to life, and fewer ways for audiences to encounter stories, ideas, and perspectives beyond their own experiences. In this country, no one is above the law,” Bonta said.

Paramount fired back that the complaint distorts settled antitrust law and is based on a misrepresentation of competition in the entertainment industry.

“The combination of Paramount and WBD will create a stronger, well-capitalized, creative-first media company that is better positioned to compete with companies like Netflix that have come to dominate the industry for audiences, premium content, and creative talent,” Paramount said.

Warner Bros. declined to respond to a Barron’s request for comment.

Despite the complaint, Paramount stock was up 2.5% to $9.65 while Warner Bros. stock had gained 3.8% to $27.61.

Many of the most-important events have slipped from our collective memories. But their impacts live on.

Americans now think they need at least $1.25 million for retirement, a 20% increase from a year ago, according to a survey by Northwestern Mutual

King Saud bin Abdulaziz Airport in Al Baha welcomed nearly 700,000 domestic passengers by mid-2026 and earned two international accreditations from Airports Council International for accessibility and customer experience.

< 1 min

King Saud bin Abdulaziz Airport in Al Baha Region, one of the airports operated by Cluster2 Airports, served nearly 700,000 passengers on domestic flights between the beginning of 2025 and the end of the first half of 2026, reflecting continued growth in air travel across the region, according to the Saudi Press Agency (SPA).

The strong passenger traffic underscores the airport’s growing role in supporting domestic connectivity and facilitating travel to and from Al Baha, as Saudi Arabia continues to invest in modernizing its aviation infrastructure and enhancing regional accessibility.

During the same period, the airport achieved two significant international recognitions from Airports Council International (ACI). It was awarded the Level 1 Accessibility Enhancement Accreditation, recognizing its efforts to improve accessibility and create a more inclusive travel experience for all passengers, including people with disabilities and those with reduced mobility.

In addition, King Saud bin Abdulaziz Airport received the Level 2 Airport Customer Experience Accreditation, reflecting its commitment to continuously improving passenger satisfaction through enhanced services, operational efficiency, and customer-focused initiatives.

The latest milestones reinforce the airport’s efforts to align with international aviation standards while supporting Saudi Arabia’s broader objectives of strengthening the quality, accessibility, and competitiveness of its airport network.

Two coming 2027 models – the first of the “Neue Klasse” cars coming to the U.S. early next year – have been revealed.

Interior designer Thomas Hamel on where it goes wrong in so many homes.

Porsche delivered 122,306 vehicles globally in the first half of 2026, down 16% year-on-year, as demand was impacted by the end of production of its combustion-powered 718 models and reduced EV incentives in the US. Despite the decline, the 911 recorded a 19% increase in deliveries, while the Cayenne remained the brand’s best-selling model.

3 min

Dr. Ing. h.c. F. Porsche AG delivered a total of 122,306 vehicles to customers in the first half of 2026 (previous year: 146,391), representing a decline of 16 per cent. The main reasons include the end of production of the combustion-engined 718, strong demand for the all-electric Macan in the same period last year, and the expiration of tax incentives for electric and hybrid vehicles in the United States.

At the same time, the 911 model line continues to enjoy strong customer demand. In the first half of this year, deliveries increased by 19 per cent compared to the previous year. This was driven by sustained demand and the phased introduction of various derivatives last year. Across all model lines, there was a balanced mix of derivatives, with a significant proportion of GTS, Turbo and GT models. Overall, the sales structure remained well balanced across the individual sales regions.

“With around 122,000 customer deliveries in the first half of 2026, we are below the same period last year but in line with our expectations,” says Matthias Becker, Member of the Executive Board for Sales and Marketing at Porsche AG. “We have been delivering the Cayenne Electric to our customers since the end of June and we are pleased with the positive feedback from our dealer network. The recently unveiled new products, such as the 911 GT3 S/C and the Taycan’s E-Shift system featuring virtual gear changes, will also delight Porsche fans around the world. We are already receiving very positive feedback from the industry media.”

North America remains the largest sales region

Among the sales regions, North America remains at the top with 37,712 deliveries. The decline of around 13 per cent can be attributed, among other factors, to the expiration of tax incentives for electric and hybrid vehicles as well as the end of production of the combustion-engined 718. Porsche’s home market of Germany recorded 14,938 deliveries, down six per cent compared to the same period last year. In Europe (excluding Germany), Porsche delivered 30,278 cars in the first half of the year, a decline of 14 per cent. The main reasons include the end of production of the combustion-engined 718 and the strong performance of the Macan Electric in the previous year.

In China, 14,501 vehicles were delivered to customers, a decrease of 32 per cent. The main reasons remain the challenging market environment and Porsche’s continued focus on value-oriented sales. In the Overseas and Emerging Markets region, Porsche delivered 24,877 cars, representing a decline of 18 per cent. Contributing factors again included the end of production of the combustion-engined 718, as well as the conflict in the Middle East.

Cayenne is the strongest model line

Among the model lines, the Cayenne achieved the highest demand with 38,141 deliveries (-9 per cent). The Cayenne Electric has been gradually introduced to markets since the end of June, with customers now receiving the first deliveries.

The iconic 911 sports car was delivered to 30,534 customers between January and June, representing an increase of 19 per cent compared to the same period last year.

A total of 35,315 Macan models were delivered. Of these, 19,695 examples were combustion-engined models, which Porsche continues to offer alongside the electric version in most countries outside the EU. Production of the combustion-engined Macan will continue until the end of July 2026. The Macan Electric accounted for 15,620 units. In total, this represents a decline of 22 per cent for the Macan model line compared to the previous year. The key factors behind this include the slower-than-expected ramp-up of electromobility, the strong performance last year, and the expiration of tax incentives for electric and hybrid vehicles in the US.

In the first half of the year, 9,308 examples of the Panamera model line were delivered to customers. The decline of 38 per cent was primarily due to a temporary product gap in China, one of the strongest Panamera markets. This gap was closed with the introduction of the market-specific Panamera Pure edition, which launched in April.

The 718 Boxster and 718 Cayman achieved 2,789 deliveries, down 73 per cent from the previous year. Production of the 718 model line ended in October 2025. In total, 6,219 Taycan models were delivered in the first half of the year, a decline of 25 per cent.

Looking ahead to the remainder of the year, Becker continues: “We are consistently aligning our offering with customer demand and further sharpening our model portfolio. In the autumn, we will present additional details of our Strategy 2035 as part of our Capital Markets Day.”

Paine Schwartz joins BERO as a new investor as the year-old company seeks to triple sales.

Following the devastation of recent flooding, experts are urging government intervention to drive the cessation of building in areas at risk.

For the first time in the modern history of the FIFA World Cup, the world’s top four ranked teams—France, Spain, England, and Argentina—have all reached the semifinals. Two blockbuster clashes now await as football’s biggest stars battle for a place in the final.

3 min

When the World Cup kicked off over a month ago, the gargantuan 48-team event was billed as the equivalent of 104 Super Bowls.

But it turns out this tournament has actually played out like another classic institution of American sports.

With Cinderella runs, a sprawling bracket, and survive-and-advance drama nearly every day, it’s clear that what we’ve really experienced is a summer version of March Madness. And this one has delivered an epic Final Four of blue bloods who have all proven they can go the distance: France, Spain, England, and Argentina.

Never before in the modern history of the World Cup have the top-four ranked teams in the world all reached the semifinals. It’s even more remarkable considering the fact that the largest ever field means that each have played an extra round. That’s one extra opportunity for a fluke, a referee’s decision, or a Cape Verde to break against them.

“It’s a privileged space in football, not an easy feat,” Argentina coach Lionel Scaloni said. “We will try to make it to the end with every last drop of sweat.”

What makes this lineup so compelling is that the two semifinals couldn’t feel more different, with something for every kind of sports fan. On one side is France vs. Spain, a highbrow matchup for the soccer purists. On the other is England vs. Argentina, a shot of pure adrenaline, straight to the veins.

In other words, it’s cinéma d’auteur vs. a blockbuster disaster movie in dazzling, deafening IMAX.

The first semifinal, in Dallas on Tuesday, pits two of the most technically and tactically sophisticated teams at the tournament against each other in a duel that feels more like a chess match.

Led by Kylian Mbappé and his eight goals, Les Bleus have proven to the world that they have the most overpowering attack in soccer, with a suffocating defense to match—they haven’t conceded in any of the past three games. Spain, meanwhile, has allowed just one goal all tournament and proven that the guys it can bring off its bench are better than the starters on practically any other team in the world.

The other half of the bracket definitely won’t be mistaken for a chess match. This one is closer to a bout of no-holds-barred mud wrestling, with a side of psychological warfare.

England vs. Argentina is the latest installment in one of soccer’s most ferocious grudge matches, a cocktail of sporting controversy and colonial history that will be waged by two sides who have chaos-balled their way through the tournament, staggering from one opponent to the next while mixing brief moments of outrageous skill with long periods of absolute agony.

In the quarterfinals, both teams needed to survive nerve-shredding periods of extra time that could easily have sent them tumbling out of the tournament. England survived its clash with Norway with a virtuoso performance by its 23-year-old hotshot, Jude Bellingham. And Argentina advanced past Switzerland despite a quiet night from its 39-year-old genius in residence, Lionel Messi.

But ahead of the semifinal, all the talk will be about a different Argentina genius—the one whose “Hand of God” goal has gone unforgiven by England fans for 40 years, Diego Maradona.

But if Maradona was English soccer’s public enemy no. 1, his successor hasn’t had a chance to traumatize 60 million English men and women all at once. At least, not yet. In 20 years at the top of the game, Messi has never before faced the Three Lions. That will finally change on Wednesday in Atlanta.

“It is always special to play against the big teams,” Messi said. “It never happened to me against England, it’s the first time, so it’s going to be a special match, a World Cup semifinal.”

Two coming 2027 models – the first of the “Neue Klasse” cars coming to the U.S. early next year – have been revealed.

eToro has unveiled a new AI-first mobile app designed to deliver smarter, more personalized investing. Powered by its proactive AI agent, Tori, the platform also introduced agentic trading, sub-accounts, a new desktop trading platform, expanded crypto self-custody tools and a growing app ecosystem to enhance the investing experience.

3 min

etoro, the trading and investing platform, today unveiled a new mobile app at its ‘Intelligence in Motion’ event in London. etoro is moving beyond the app itself, to be wherever investors are. The company shared updates including agentic trading and sub-accounts, a new desktop platform for active traders, a growing app store, and new tools for crypto self-custody.

Retail investors’ expectations have evolved. They want an investing experience that’s smart, accessible, and tailored to their needs. One that proactively surfaces relevant information when it matters most, instead of leaving them to dig for it. The new app is etoro’s answer. At its center is Tori, etoro’s proactive AI agent, working alongside the collective knowledge of etoro’s community of millions. Together, they give investors human insight, supercharged by AI.

“Our AI is built on the real decisions and track records of millions of investors. An intelligence that’s hard to replicate,” said Yoni Assia, Co-founder and CEO of etoro. “By bringing AI and our community together, we’re helping people invest with greater knowledge and confidence. For nearly two decades we’ve worked to give everyone a seat at the table, this is the next step.”

At the London showcase, the etoro team revealed:

Reimagining investing & wealth management

A new AI-first app: A completely rebuilt mobile app, designed to feel faster and more personal. It brings clearer portfolio views, richer asset pages, advanced charts, and more ways to tailor the experience to how you invest.

Proactive insights with Tori: Tori doesn’t wait to be asked. It surfaces portfolio insights, market signals, and the reasons behind a price move, right when they matter.

Tori, wherever you are: Investors can get Tori’s insights via WhatsApp and Apple Watch. So they can check their portfolio and respond to market developments without opening the app at all.

A sub-account for every goal: New sub-accounts let investors separate what they’re investing for: a child’s future, a house deposit, a long-term retirement fund, and manage each side by side.

Sharper data, built around you: Redesigned asset pages bring professional-grade charts and analytics to every investor, letting them customize exactly what data they see first.

Enhanced trading capabilities

etoro edge: A new desktop app for active traders, with professional-grade charting, and analytics built for heavy trading.

Agent-powered portfolios: Investors can build or copy AI agents that trade around the clock on their behalf, each running inside their own sub-account. Tori keeps every agent organized in one place and investors stay in control throughout.

A growing app ecosystem

The etoro App Store is growing: Investors can browse and add to a growing range of trading and analytics applications, built by partners, developers, quants, and everyday users. etoro’s Builders’ Portal provides structured access to APIs and other development resources.

Future-proofing for an on-chain world

Instant self-custody wallets: Investors who want direct ownership of their crypto can set up a secure digital wallet in seconds, right from Tori. No separate app, no complicated setup. It gives them direct control of their assets and access to decentralized finance (DeFi), powered by Zengo, the self-custody technology now part of etoro.

A refreshed brand

The launch comes with a refreshed etoro brand: a new logo, a new look, and a new tagline, “Know better.” It reflects eToro’s focus on helping people make clearer, better-informed financial decisions.

“Agentic trading is accelerating, and our App Store is growing fast. The world of finance never stops changing, and for nearly two decades we’ve harnessed each shift early, from social investing to crypto, and now AI. And each time, we’ve put that technology to work levelling the playing field faster for everyday investors,” concludes Yoni Assia.

A London showcase

The announcements were unveiled at ‘Intelligence in Motion’, a live event in London for clients, Popular Investors, partners, etorians, influencers, and media.

Two coming 2027 models – the first of the “Neue Klasse” cars coming to the U.S. early next year – have been revealed.

Dubai made ambition visible.

These ten creators made it watchable — to a combined audience of tens of millions across the Gulf and the world.

7 min

Dubai has done something no older city has managed: it has made ambition visible without making it vulgar. The hypercars, the hotel suites, the front rows at Paris Fashion Week populated by Gulf-based creators — none of it feels accidental. The luxury ecosystem the Gulf has built across Dubai and Doha in a single generation is now documented daily by a cohort of creators whose combined reach would dwarf the circulation of every major print luxury title in the world.

The ten creators on this list are the ones whose work most faithfully represents what the Gulf’s actual luxury landscape looks like — not what it aspires to be, but what it already is. They are not simply the most followed accounts in the UAE or Qatar. They are the ones with the clearest editorial eye, the most genuine access to the world they document, and the audiences that trust them to deliver it accurately.

| Dubai and Doha’s luxury creators did not follow the Gulf’s ambition. In many cases they preceded it — making the world aware of what these cities were becoming before the cities themselves had fully arrived. |

1. Huda Kattan – @hudabeauty · Founder of Huda Beauty

Huda Kattan is the most followed person in the Gulf, the founder of a global cosmetics company with retail presence across 140 countries, and a creator whose 50 million Instagram followers represent one of the largest single audiences built by any individual operating from a Dubai base. The Huda Beauty story — a creator who turned a personal beauty obsession into a global brand from a Dubai apartment — is the defining luxury success story of the region’s social media era.

A Kanebridge News Middle East feature on Huda Kattan is not primarily about her follower count. It is about what she represents: proof that the Dubai platform, applied to genuine product excellence and real creative taste, produces something of extraordinary and lasting commercial value. That is a story that belongs in the publication covering what the Gulf has built.

2. Supercar Blondie – @supercarblondie · Alexandra Hirschi

2. Supercar Blondie – @supercarblondie · Alexandra Hirschi

Alexandra Hirschi — Supercar Blondie — is the most influential automotive content creator in the world. Operating from Dubai, which provides first-to-market access to many of the region’s most extraordinary car reveals, she has built an audience exceeding 12.8 million on Instagram and considerably larger combined reach across platforms. In 2026, she secured exclusive first-drive access to three hypercars valued above two million US dollars each — including a limited-production electric hypercar reveal in Dubai that surpassed 40 million cross-platform views.

The cars she covers — Bugattis, Koenigseggs, bespoke Rolls-Royces, machines valued at prices that most people will never encounter — are precisely the vehicles that Kanebridge News Middle East’s affluent Gulf readership follows closely. The editorial alignment between her content and the publication’s luxury coverage is direct, and the audience overlap is among the most significant of any creator on this list.

3. Nour Arida – @nourarida · Fashion & Luxury Creator

3. Nour Arida – @nourarida · Fashion & Luxury Creator

There are luxury influencers who attend fashion weeks, and there are those who are invited back the following season because the houses want them there. Nour Arida is the second kind. Present at Milan and Paris Fashion Weeks in 2026 on the strength of genuine relationships with luxury fashion houses — not paid placements but editorial invitations — she has built a profile that is recognized as much by the industry as by her audience.

Her children’s label Generation Peace expanded in 2026 into premium department stores across the UAE, Qatar and Saudi Arabia. The combination of high-fashion editorial credibility and regional commercial enterprise is the exact profile that Kanebridge News Middle East’s luxury editorial is built to cover — she is not simply aspirational, she is building something real.

4. Ola Farahat – @olafarahat · Luxury Fashion, UAE

4. Ola Farahat – @olafarahat · Luxury Fashion, UAE

Ola Farahat has built a 1.2 million-strong Instagram following through luxury fashion content that reflects genuine knowledge of the brands, the quality levels and the cultural context of high-end dressing in the UAE. The content is not an inventory of logos. It is an exercise in taste — and that distinction is what her audience of Dubai’s fashion-literate consumers consistently responds to.

In a market saturated with luxury brand content, the creators who communicate taste rather than simply consumption are the ones that attract the audiences that matter to luxury brands and to the editorial publications that cover them. Ola Farahat’s audience is exactly that audience.

5. Alanoud Badr (Fozaza) – @fozaza · Fashion Designer, UAE

Alanoud Badr — known as Fozaza — brings a fashion designer’s eye to content that spans her own collections, luxury brand collaborations and the broader fashion landscape of the UAE. With 780,000 followers, she has built an audience that understands the difference between someone who buys luxury and someone who creates within it.

For Kanebridge News Middle East’s luxury editorial, her designer credentials provide an angle that distinguishes a profile of her work from the standard luxury lifestyle feature. This is not a review of what she wears — it is an examination of what the fashion industry in Dubai and the Gulf has produced in a creator who is genuinely, professionally inside it.

6. Khalid Al Ameri – @khalidalameri · Emirati Creator (Luxury Crossover)

6. Khalid Al Ameri – @khalidalameri · Emirati Creator (Luxury Crossover)

Khalid Al Ameri appears in both the Finance and Luxury categories of this list because his content resists the kind of neat categorisation that most creator lists impose — and that resistance is precisely the point. His 3 million-plus followers engage with a content world that spans business, family, Emirati culture, and the experience of wealth in Dubai at the intersection of tradition and radical modernity.

For the luxury editorial specifically, his value is this: he makes the Emirati experience of Dubai — which is genuinely different from the expatriate experience, and genuinely different from the tourist experience — accessible and comprehensible to a global audience. That cultural translation is a form of luxury editorial that most publications covering the Gulf have not produced. Kanebridge News Middle East should be the one that does.

7. Asmaa Ibraheem – @asmaaibraheem · Fashion & TV Presenter, UAE

7. Asmaa Ibraheem – @asmaaibraheem · Fashion & TV Presenter, UAE

Asmaa Ibraheem is a UAE television presenter and fashion influencer whose luxury sensibility has earned her the Star of the Night Award at the EMIGALA Awards and the Falcon of the Year recognition from the Distinctive International Arab Festivals Award. Her content moves between editorial fashion, luxury lifestyle and event coverage across the Gulf’s most significant social occasions.

The broadcast credibility underlying her social media presence gives her content a register that purely digital creators have rarely achieved — an authority that comes from being recognized by the Gulf media establishment as well as the digital one. For Kanebridge News Middle East’s print edition, that dual credibility makes her an ideal profile subject.

8. Karen Wazen – @karenwazen · Entrepreneur & Luxury Fashion Creator, UAE

8. Karen Wazen – @karenwazen · Entrepreneur & Luxury Fashion Creator, UAE

Karen Wazen is a Dubai-based entrepreneur, fashion and lifestyle creator, and founder of the globally recognized Karen Wazen Eyewear brand. With millions of followers across social media, she has established herself as one of the Middle East’s most influential luxury personalities through collaborations with leading fashion houses, appearances at international fashion weeks, and a brand that has grown from the Gulf into international markets. Her content blends luxury fashion, beauty, travel and entrepreneurship, reflecting a modern vision of Middle Eastern elegance.

The commercial success behind her social media presence gives her influence a depth that extends well beyond digital content. By building an internationally recognized luxury brand while maintaining a strong editorial presence, Karen Wazen represents the evolution of the creator economy in the Gulf. For Kanebridge News Middle East’s luxury editorial, she embodies the intersection of creativity, entrepreneurship and global luxury that defines the region’s new generation of business leaders.

9. Joelle Mardinian – @joellemardinian · Founder, Joelle Group

9. Joelle Mardinian – @joellemardinian · Founder, Joelle Group

Joelle Mardinian built her audience before the influencer category existed — through television, through the Joelle Group clinics and salons operating across the Gulf, and through a media presence that the regional beauty and lifestyle establishment has recognized for more than a decade. The depth of brand loyalty she has built is something that purely digital creators have rarely achieved.

For Kanebridge News Middle East’s luxury editorial, she represents the established layer of the Gulf’s creator economy, a figure who maintained her audience through every shift in platform and format by producing consistent quality and genuine cultural resonance across the GCC. That longevity in the Gulf market is its own form of luxury credibility.

10. Tony Kairouz – @tonykairouz · Luxury Travel & Lifestyle Creator

10. Tony Kairouz – @tonykairouz · Luxury Travel & Lifestyle Creator

Tony Kairouz is a Dubai-based luxury travel and lifestyle creator whose content showcases the region’s most exclusive hotels, fine dining destinations, private aviation experiences and premium automotive culture. Through cinematic storytelling and high-production visuals, he has built a following that looks to his platform for inspiration on luxury travel, hospitality and elevated living across the UAE and beyond. His collaborations with leading hospitality and luxury brands have positioned him among the region’s recognised voices in aspirational travel content.

The visual quality and editorial consistency of his content distinguish him from conventional travel creators, presenting luxury as an experience rather than simply a destination. His audience reflects the affluent, internationally minded demographic that follows Dubai’s evolving luxury landscape, making him a strong fit for Kanebridge News Middle East’s luxury coverage and its readership interested in premium lifestyle, travel and hospitality.

The sports-car maker delivered 279,449 cars last year, down from 310,718 in 2024.

DMCC has unveiled DMCC Cyber, a dedicated cybersecurity hub under its new DMCC Tech platform, as its technology community surpasses 4,000 companies. The initiative strengthens Dubai’s digital economy by connecting businesses across AI, cybersecurity, blockchain, gaming, and emerging technologies within one integrated ecosystem.

2 min

DMCC, the leading international business district that drives the flow of global trade through Dubai, has launched DMCC Cyber, a dedicated cybersecurity vertical, as it formally establishes DMCC Tech, its overarching technology platform bringing together the specialized centers and communities driving the digital economy.

The announcement comes as DMCC’s technology sector surpasses 4,000 companies, making it the largest and fastest-growing segment within its business district. As the community has grown in scale and maturity, DMCC has continued to develop increasingly specialized platforms that address the evolving needs of technology businesses while creating greater opportunities for collaboration and innovation.

DMCC Cyber represents the latest step in that evolution. Home to more than 200 cybersecurity companies, the new vertical is dedicated to businesses operating across cyber resilience, digital trust, data protection, identity, and governance, risk and compliance. It complements DMCC’s existing specialist centers, recognizing the increasingly critical role cybersecurity plays in enabling digital business and protecting the infrastructure that underpins the global economy.

A technology company builds the systems, platforms, and applications that move value, information, and services across the digital economy. A cybersecurity company protects those systems, safeguarding the data, infrastructure, and trust on which every digital business depends.

Ahmed Bin Sulayem, Executive Chairman and Chief Executive Officer, DMCC, said: “Technology has become the largest and fastest-growing sector in our business district, reflecting Dubai’s position as one of the world’s leading destinations for innovation and high-growth businesses. As that community has expanded, so too has the need for more specialized platforms that support different segments of the technology economy. DMCC Tech brings these communities together under a single ecosystem, while DMCC Cyber reflects the growing importance of cybersecurity in an increasingly digital world. Together, they strengthen our ability to help technology companies establish, connect and scale internationally from Dubai, with direct access to one of the world’s most dynamic business communities.”

DMCC Cyber joins the DMCC AI Centre, DMCC Crypto Centre, and DMCC Gaming Centre under the DMCC Tech platform, with DMCC Quantum set to follow. Together, these specialized centers and verticals provide technology companies with direct access to one of the world’s most connected business communities, linking them to more than 26,000 member companies operating across global trade, finance, commodities, and emerging technologies.

The platform is already home to globally recognized companies including CrowdStrike, PwC, CYFIRMA, and FPT Software, reflecting the scale, diversity, and international reach of DMCC’s technology community.

DMCC Tech spans the full breadth of the digital economy, bringing together specialist centers and verticals across artificial intelligence, cybersecurity, blockchain, gaming, and emerging technologies. The platform also extends to the frontiers of innovation, including the rapidly developing space economy, where advances in satellites, earth observation, and space-derived data are reshaping industries from trade and finance to logistics and resource management.

As these technologies become increasingly embedded in the global economy, DMCC Tech provides the platform for commercial growth, while DMCC Cyber helps strengthen the resilience and security of the critical digital infrastructure on which they depend.

Parts for iPhones to cost more owing to surging demand from AI companies.

A major World Cup controversy has erupted after Folarin Balogun’s suspension was reportedly overturned ahead of the USA’s round-of-16 clash with Belgium. The decision, said to follow President Trump’s intervention with FIFA President Gianni Infantino, has sparked debate over political influence, sporting integrity, and FIFA’s disciplinary process.

3 min

The most stunning controversy of the 2026 World Cup erupted on Sunday after it emerged that President Trump personally intervened to have U.S. striker Folarin Balogun reinstated for the team’s round-of-16 game against Belgium following his red card in the previous round.

Trump called FIFA president Gianni Infantino last week, urging him to review Balogun’s automatic one-game suspension, according to people familiar with the matter.

Trump told Infantino that everyone was telling him the decision was wrong and Infantino promised to look into the matter. Later, the FIFA president called the U.S. president back and told him the suspension would be reversed and Balogun would be free to face Belgium on Monday, one of the people said.

Balogun, 25, was due to sit out the do-or-die contest in Seattle after being controversially ejected for stepping on an opponent’s ankle during the Americans’ 2-0 victory over Bosnia and Herzegovina. Under normal tournament rules, that triggered an automatic ban—and U.S. Soccer and FIFA officials said after the game that there were no provisions for an appeal.

The sudden reversal, unprecedented in the modern history of the World Cup while a tournament was under way, immediately touched off a furor about political interference and sporting integrity. Infantino had spent nearly a decade in the buildup to the tournament courting favor with Trump, who calls him a friend and has regularly hosted him inside the Oval Office.

“Thank you to FIFA for doing what was right, and reversing a great injustice!” President Trump posted on Truth Social.

The Belgian soccer association said it was “astonished” by the U-turn and that it was “investigating all potential options” ahead of Monday’s game.

“The decision is in direct contradiction with the provisions of the FIFA World Cup 2026 Competition Regulations,” the federation added.

FIFA cited a little known provision, known as Article 27, that allowed its Disciplinary Committee to use its discretion to suspend Balogun’s ban for 12 months. Despite the opaque and unusual nature of the decision, the organization declined to elaborate further on its reasoning. The U.S. team, which was involved in the disciplinary review according to a person familiar with the process, found out that Balogun would be eligible around 7:30 a.m. Pacific time on Sunday.

This isn’t the first time that FIFA has deployed Article 27 to rescue a high-profile player from exclusion.

Last November, superstar Cristiano Ronaldo received a red card in Portugal’s penultimate qualifying match for deliberately elbowing an Irish player—which would have come with a three-match suspension, and cost him two matches of the World Cup group stage. But within days, FIFA’s Disciplinary Committee adjusted his punishment to a one-year probationary period.

Now Balogun has also been granted the same clemency.

Balogun had put the U.S. up against Bosnia with his third goal of the tournament. But in the 64th minute, he was sent off after a video review that lasted several minutes. That meant the Americans had to finish the game with only 10 men and face the prospect of taking on Belgium without him.

Immediately, American fans were the ones calling foul. Even though Balogun had stepped on Tarik Muharemović’s leg, there was no indication he did it on purpose.

“For me, never it’s a red card,” U.S. coach Mauricio Pochettino said. “It was a normal action in football that happened by accident. But it’s not intentional.”

The decision was especially harsh in contrast to an incident earlier in the tournament when Argentine superstar Lionel Messi committed a similar foul against an Algerian player—and went unpunished.

The undermanned Americans were able to close out the game against Bosnia, but Pochettino was left with the daunting task of finding a replacement for his most effective weapon.

Then, barely 24 hours before they played for a place in the quarterfinals, the tournament co-hosts became the beneficiaries of FIFA’s ultimate discretion.

Paine Schwartz joins BERO as a new investor as the year-old company seeks to triple sales.

BMW has unveiled the next-generation X5, introducing five powertrain options for the first time—including petrol, diesel, plug-in hybrid, all-electric, and an upcoming hydrogen variant. Built on Neue Klasse technologies, the new X5 also features a redesigned look, advanced digital features, and an electric range of up to 845 km for the iX5.

5 min

The new BMW X5 adds another chapter to its story of success. The fifth generation of the BMW X5 impresses with technical innovations, a stunning new design and the integration of future-oriented technologies from the Neue Klasse. This underlines its exceptional status and reinforces its leading position in a segment that it originally established.

First model from the brand with five different drive system types.

As the first Sports Activity Vehicle (SAV) from the brand and founding father of the eminently successful BMW X family, the trendsetting BMW X5 has been shaping the future in innovative style since its introduction in 1999. Embodying that very same aspiration, the new BMW X5 is the first model from the brand to come to market with a choice of five different drive system types.

In addition to variants with petrol or diesel combustion engines, including 48V mild hybrid technology, and plug-in hybrid models, the fifth generation of the successful model does not just encompass the first all-electric BMW iX5. The BMW iX5 Hydrogen is also set to celebrate its market launch – at a later stage – as the first hydrogen-powered BMW production vehicle. The powertrain encompasses the fuel cell system, in-car hydrogen storage with the new BMW Hydrogen Flat Storage technology and an innovative high-voltage battery. The third generation of the fuel cell system enables a particularly compact design within a high-performance, efficient drive system with a range of up to 750 kilometers.

The new BMW iX5 – the first battery-electric BMW X5 – is launching with the sixth generation of BMW’s eDrive technology. This means longer ranges of up to 845 kilometers in the BMW iX5 60 xDrive, fast charging, 800V technology and practical bidirectional charging. This is thanks to new cylindrical cells with a height of 120 millimetres, installed in the high-voltage battery and in use for the first time in the new BMW iX5.

“With its imposing presence and flawless symbiosis of comfort and driving pleasure, the BMW X5 became a global bestseller,” says Dr. Joachim Post, Member of the Board of Management of BMW AG responsible for Development. “And now the latest generation also benefits from the technologies in the Neue Klasse and the widest possible range of drive systems. As a result, I’m sure the new BMW X5 will set the benchmark in its class once again and write the next chapter in its success story.”

New design: unmistakable presence from every perspective.

The new BMW X5 also takes a major leap forward in terms of design. Viewed from any perspective, the clear, monolithic and powerful appearance of the car embodies the confident presence that underlines its leading position in the segment, becoming one of the key faces of the brand. This is in large part down to the effortless melding of classic SAV proportions with the forward-looking BMW design language of the Neue Klasse to produce a harmonious, distinct end result.

The next generation of the distinctive X exterior is characterized by the upright design of the front end, the vertically aligned BMW kidney Iconic Glow and the new “double-X” light icons, making their first appearance in a BMW. The clearly structured side view of the BMW X5 is particularly impressive, thanks in large part to the innovative door handles, the BMW Winglets. These combine progressive design with functional convenience: recessed handles requires the lightest of touches to open the electrically powered doors.

Naturally, all models offer broad scope for tailoring the design, including eleven exterior paint colors and a precisely curated wheel range that now boasts 23-inch rims. The new BMW X5 M60e xDrive creates visual highlights emphasizing its role as the sporting flagship, while the M Sport package and the M Sport package Pro provide a range of distinctive features.

High-quality M Performance Parts available.

In addition, high-quality M Performance Parts are available for the BMW X5. Highlights of the range include striking exterior items such as the M Performance front splitter carbon fibre, M Performance roof spoiler black high-gloss, M Performance rear diffuser aramid and M Performance exterior mirror caps aramid. Also available are M Performance summer and winter complete wheels in 21- and 23-inch formats. The cabin can likewise be given an even sportier look with items such as the M Performance floor mats.

Spacious, natural and innovative: redesigned interior combines feel good atmosphere with digital user experience.

One glance at the redesigned interior immediately reveals the extremely high quality of the new BMW X5. The interior impresses with clear structures and uncluttered surfaces, producing a harmonious sense of space and calmly providing subtle support for classic BMW driver orientation.

The outstanding visual and haptic quality of the interior is also underlined by the new decorative surfaces constructed from materials such as slate and glass that generate an atmosphere of elemental sophistication. BMW is the first carmaker worldwide to offer slate as an optional decorative surface.

The BMW X5 incorporates core technologies from the Neue Klasse in the form of the new BMW Panoramic iDrive display and operating system, underpinned by BMW Operating System X. These include the Central Display in free-cut design, the BMW 3D Head-Up Display, the BMW Passenger Screen available as an optional extra in the BMW X5 for the first time, the BMW Panoramic Vision with a projection surface extending across the full width of the windscreen and the new multifunction steering wheel. This results in an all-encompassing digital user experience centered around both the driver and their passengers.

The BMW X5 combines fascinating new technologies with a genuinely feel-good interior atmosphere. This is expressed in the lighting animations provided by the ambient light strip, a central element that creates an inviting wrap-around effect from door to door to generate a harmonious atmosphere.

BMW X5 combines a high level of comfort with BMW typical driving dynamics and intelligent driver assistance systems.

As the sportiest SUV in its segment, the BMW X5 has long set standards in terms of driving dynamics – and the latest generation of the BMW X5 is equally impressive in its this respect. This is due in no small part to the adaptive suspension fitted as standard and axle load distribution close to 50:50. Optional extras include Adaptive Chassis Control, as well as the Adaptive Chassis Control Professional with roll stabilization initially available for every all-electric and plug-in hybrid model. This system leads the way when it comes to blending BMW’s characteristic driving dynamics with maximum ride comfort.

BMW Symbiotic Drive provides intelligent support tailored to individual driving behavior. The advanced Level 2 driver assistance systems and active safety functions are designed down to the smallest detail for seamless interaction between assistance and human driving. In the BMW iX5 models, and in the upcoming BMW iX5 Hydrogen, the Heart of Joy also enables a very special experience: BMW Soft-Stop, which executes the smoothest stopping action every provided by BMW.

Production and premiere in Spartanburg.

The market launch of the first variants of the new BMW X5 is scheduled for late November 2026, with the all-electric and plug-in hybrid versions to follow in early 2027. Production of the new models will ramp up some months ahead of this, with BMW Group Plant Spartanburg (USA) initiating series production of the fifth-generation BMW X5 in August 2026.

Plant Spartanburg has been producing the X5 ever since it was launched – founding a new market segment – in 1999. And now the facility is celebrating a new premiere: the new BMW iX5 will be the first all-electric vehicle to be manufactured there. The new factory for sixth-generation high-voltage batteries built for this model variant adjacent to BMW Group Plant Spartanburg requires no fossil fuels for normal operations. This is just one of many examples of the BMW Group’s rigorous approach to minimizing CO2e emissions during production.

Two coming 2027 models – the first of the “Neue Klasse” cars coming to the U.S. early next year – have been revealed.