Kuwait Channels Assets to Wealth Fund to Improve Cash Flow

Kuwait has completed the transfer of its remaining valuable assets to the sovereign wealth fund, in return for cash to address its budget deficit.

< 1 min

< 1 min

The transferred assets reportedly include shares in Kuwait Finance House and Zain, a telecommunications company, as well as the state-owned Kuwait Petroleum Corp., valued nominally at 2.5 billion dinars ($8.3 billion), transferred in January.

This move comes as a result of a political dead end that has prevented the government from borrowing, leading to a liquidity crisis in one of the world’s wealthiest countries. This crisis prompted Fitch Ratings to revise its outlook on Kuwait to negative, while maintaining its AA rating.

Fitch cited concerns over the rapid reduction of liquid assets and the lack of legislative approval for government borrowing as factors contributing to financial uncertainty. This follows the warning sent by S&P Global Ratings about a potential downgrade in the country’s rating within the next six to 12 months if the political standstill persists.

Despite being a high-income country, Kuwait has drained its reserves due to long periods of low oil prices. In a bid to generate funds, the government has exchanged its prime assets for cash with the $600 billion Future Generations Fund, designed to preserve the country’s wealth beyond the oil area. With the completion of these asset transfers, it remains uncertain how Kuwait will manage its eighth straight budget deficit, estimated at 12 billion dinars for the upcoming fiscal year starting in April.

Workplace disputes are increasingly forcing companies into a tough call: fight allegations or settle to avoid reputational and legal fallout. While many claims are disputed, settlements are often driven by cost, risk, and disruption—especially in an era where AI and social media can rapidly amplify accusations beyond control.

Dubai International Financial Centre (DIFC) reaffirmed the strength and resilience of its ecosystem, with global institutions across banking, insurance, wealth and innovation continuing to back Dubai and the UAE as a long-term growth hub. Despite regional uncertainty, firms are deepening their presence, supported by a stable regulatory framework, strong connectivity, and access to high-growth markets across MEASA.

In times of heightened uncertainty, investing shifts from prediction to resilience. With geopolitical risks impacting confidence, energy prices, and global growth, the focus turns to liquid, high-quality assets built to withstand multiple scenarios. As volatility rises and dispersion widens, diversification, strong fixed income positioning, and portfolio flexibility become essential to navigating an increasingly complex market environment.

Rising global bond yields and uncertainty around the US Federal Reserve are increasing market volatility, as investors reassess inflation risks, interest rates, and global economic conditions.

2 min

Government bond yields are rising across major economies including the US, UK, Europe and Japan, as investors reassess inflation risks amid higher energy prices, geopolitical tensions and growing fiscal pressures.

The move higher in sovereign yields reflects increasing market acceptance that interest rates may remain elevated for longer than previously expected, despite earlier hopes for monetary easing later this year.

Higher yields are also adding pressure to global equity markets, particularly growth and technology sectors, while increasing concerns over borrowing costs for governments and corporations carrying large debt burdens.

Lale Akoner, Global Market Strategist at eToro, said: “Markets are becoming increasingly sensitive to geopolitical risks and inflationary pressures. Rising oil prices and concerns around potential disruption in the Strait of Hormuz are reviving fears that inflation could remain stickier than expected at a time when many central banks were hoping to see further easing in price pressures.”

She added: “Bond markets are signalling that investors should prepare for a more volatile environment in the second half of the year, where elevated borrowing costs and uncertainty around monetary policy are likely to remain key themes.”

At the same time, investors are closely watching developments at the US Federal Reserve, as Kevin Warsh moves closer to potentially succeeding Jerome Powell as Fed Chair when Powell’s term ends on Friday.

According to Akoner, markets may be oversimplifying the implications of a potential Warsh-led Federal Reserve by viewing it purely through a hawkish-versus-dovish lens.

“A Warsh Fed would not necessarily represent a major tightening shock or a return to ultra-loose monetary policy,” she said. “Instead, it could signal a shift toward a more market-driven approach, relying less on balance sheet expansion and forward guidance, and more on market pricing, private capital and economic fundamentals.”

Such a shift could gradually reduce the Fed’s balance sheet and place greater responsibility on private banks and investors to absorb liquidity and government debt issuance.

For investors, this may create clearer distinctions between market winners and losers. Shorter-dated bonds could benefit from potential rate cuts once energy-related inflation pressures ease, while longer-term bonds may face continued pressure if inflation concerns and government borrowing keep yields elevated.

Financials, banks, insurers, asset managers and cyclical value sectors could stand to benefit from this environment, while speculative growth stocks, heavily indebted companies and weaker high-yield borrowers may face greater market scrutiny.

“Ultimately, a Warsh Fed could reshape how risk is priced across markets,” Akoner said. “That would likely leave investors more exposed to volatility and place a greater premium on quality, diversification and active positioning.”

The rise in global yields, combined with uncertainty over the future direction of US monetary policy, is expected to remain a key driver of investor sentiment and market performance through the remainder of the year.

Following the successful launch of its Palais Collection, MAISON de SABRÉ has unveiled a new modular handbag system offering more than 720 styling combinations.

Two coming 2027 models – the first of the “Neue Klasse” cars coming to the U.S. early next year – have been revealed.

Kuwait’s Heavy Engineering Industries and Shipbuilding Co. (HEISCO) has renewed a KD14 million ($45.4 million) credit facility agreement with a local bank to support its operational activities, marking the company’s second facility renewal this month following an earlier KD96.06 million agreement. The engineering and shipbuilding firm has also continued expanding its project portfolio in 2026, including securing a $565 million contract from Kuwait Oil Company in April.

< 1 min

The Kuwait-based Heavy Engineering Industries and Shipbuilding Co. (HEISCO) has renewed a 14 million dinars ($45.4 million) credit facilities agreement with a local bank in the Gulf state.

HEISCO said in a bourse filing, the facility will be used to finance the operational activities.

This is the second loan facility renewed by the contractor this month, with the earlier facility amounting to KD 96.06 million.

The engineering and shipbuilding firm has secured a number of contracts in the first half of this year, including one in April from the state-backed Kuwait Oil Company amounting to $565 million.

Parts for iPhones to cost more owing to surging demand from AI companies.

New research suggests that bonuses make employees feel more like a mere cog in a wheel.

Longtime crypto investors are increasingly turning to Zcash, drawn by its privacy-focused features and growing momentum as some become disillusioned with bitcoin’s mainstream evolution.

3 min

Bitcoin die-hards think they’ve found the hot new thing.

Some longtime crypto enthusiasts are souring on bitcoin as it goes mainstream, frustrated that it no longer provides the privacy they value. Others are disenchanted with how politicians and celebrities are suddenly embracing bitcoin—or they’re just fed up with the token’s slumping price.

Now, bitcoin’s early evangelists are getting behind another digital token: Zcash.

Tyler and Cameron Winklevoss are among the bitcoin pioneers betting big on the so-called privacy token, which lets users shield their transaction details.

Zcash’s emphasis on anonymity reminds some of crypto’s early days, when privacy was championed as a ticket to personal freedom.

“It feels like bitcoin circa 2013,” said Barry Silbert, founder of Digital Currency Group and Grayscale Investments, which set up the first publicly traded bitcoin fund.

This year, DCG made Zcash one of its largest holdings, according to a person close to the matter. In November, Grayscale told regulators that it plans to convert its Zcash trust into an exchange-traded fund, making it more easily accessible to everyday investors. The move helped supercharge the token’s rally.

Zcash is up about 50% over the past month and 1,140% over the past year. Bitcoin, by comparison, has gained 8% in the past month, and dropped 24% in the past year.

Also driving Zcash’s surge: receding fears that U.S. regulators will take issue with the coin’s privacy features, which some worry could be exploited for ill use. Earlier this year, the Securities and Exchange Commission said it closed a probe into the coin.

Zcash, at $8.9 billion, is a smidgen of the size of bitcoin. And tiny cryptocurrencies have a history of surging and then collapsing, a reason to be wary.

Bitcoin vs. Zcash

| Bitcoin | Zcash | |

|---|---|---|

| Creator | Unknown | Group of scientists and engineers |

| Year founded | 2009 | 2016 |

| Distinction | Biggest cryptocurrency | Shielded addresses |

| 1-yr price change | down 24% | up 1,140% |

| Market cap | $1.59 trillion | $8.9 billion |

That hasn’t stopped some of bitcoin’s best-known backers from piling in.

The Winklevoss twins said in November that they invested $50 million to help launch Cypherpunk Technologies, a digital-asset treasury company that will hold Zcash.

“This is not some newfangled project that showed up on the scene with a lot of buzzwords and marketing push,” Cameron Winklevoss said in an interview.

Despite its hot new status in cryptoland, Zcash is a decade old.

The token was founded in 2016 by a group of scientists and engineers, including from MIT and Johns Hopkins. It was essentially a copy of bitcoin, but was intended to fix what its founders saw as a privacy flaw.

Like bitcoin, it lets users send or receive funds on a public ledger. The key distinction is that Zcash gives users the option to use shielded addresses, which use encryption to hide sensitive data, such as the sender, receiver and transaction amount.

(Zcash’s name is a nod to its use of zero-knowledge proofs, which allow for transaction verifications without divulging other details.)

Users can generate “viewing keys” to share transaction details with regulators or auditors—but it’s at their discretion.

The feature could give the coin vast commercial potential. Businesses, for instance, might use it to hide sensitive information such as payrolls and supplier relationships.

Proponents say it could also counter the moves of authoritarian governments to use financial surveillance to identify dissidents—a goal tracing back to crypto’s roots.

“Zcash is what bitcoin should be. It’s what bitcoin was originally meant to be,” said Tushar Jain, co-founder of Multicoin Capital, a venture-capital firm that recently built a significant position in Zcash.

Although bitcoin users don’t have to use their real names on the blockchain, its public ledger has made the token increasingly easy to trace. Many blockchain analytics firms help law enforcement decipher “anonymous” transactions and hunt down illicit activity.

For some, the extra layer of privacy that Zcash offers is a red flag.

Authorities worry that terrorists and other malicious actors could use such privacy coins to evade sanctions and commit crimes. Regulators in other countries have prohibited or restricted the listing of privacy coins on licensed exchanges.

Blockchain analysts have noted that terrorist groups so far have largely favored bitcoin and stablecoins, partly because they are easier to trade than privacy coins, which are much smaller in size.

For all the recent excitement around Zcash, the token lacks a feature that helped fuel bitcoin’s mythic status: a mysterious creator.

Unlike Satoshi Nakamoto, one of Zcash’s founders has remained a vocal figure.

Zooko Wilcox-O’Hearn, an American computer-security specialist and cryptographer, served as CEO of Electric Coin Co., which Zcash co-founders formed to develop the coin’s blockchain.

Since stepping down from that role in late 2023, Wilcox-O’Hearn has served as the chief product officer at Shielded Labs, which helps advance Zcash.

In December, he also joined the Winklevoss twins’ Cypherpunk Technologies as a strategic adviser. So far, the Zcash hoarding company has stockpiled more than 300,000 of the tokens.

Cypherpunk’s stock has gained 17% this month but is down 10% for the year. Along with the price of bitcoin, companies that hoard digital tokens have lately lost some of their luster.

Many of the most-important events have slipped from our collective memories. But their impacts live on.

Paine Schwartz joins BERO as a new investor as the year-old company seeks to triple sales.

Workplace disputes are increasingly forcing companies into a tough call: fight allegations or settle to avoid reputational and legal fallout. While many claims are disputed, settlements are often driven by cost, risk, and disruption—especially in an era where AI and social media can rapidly amplify accusations beyond control.

3 minAn employee comes forward with embarrassing workplace allegations fraught with legal risks. For company bosses, it presents a thorny dilemma: Fight or pay?

It is a situation JPMorgan Chase JPM -0.70%decrease; red down pointing triangle found itself in weeks before a former banker filed a lawsuit filled with sensational accusations. It offered $1 million to settle his claims that a female colleague had sexually harassed and assaulted him and that co-workers had subjected him to discrimination, The Wall Street Journal reported. The bank has said it investigated the claims and doesn’t believe they have merit.

Though such deals rarely come to light, paying employees to make potential scandals go away isn’t an uncommon practice across corporate America. Companies have long offered settlements to head off litigation or avoid claims that could tarnish their reputations—even if executives conclude the allegations lack merit.

“The vast majority of settlements are business decisions,” said Bill Stein, a Los Angeles-based partner at employment law firm Fisher Phillips, who often works with companies on such matters. Some employers, wanting to avoid the time, expense and headaches of unwanted publicity and litigation, ask: “Can we just make this go away?”

The calculations over when and how much to negotiate have become more complicated now that artificial intelligence and social media can easily amplify such allegations. Often the decision-making involves external law firms, internal investigations and discussions with everyone from human-resources specialists to strategists in crisis public relations, executives and attorneys say.

Internal complaints—about anything from bullying and policy violations to performance issues and workplace violence—are surfacing with increasing frequency, data suggest. Allegations of discrimination, harassment and retaliation rose to 14.7 per 1,000 employees in 2024, up from 6.4 in 2021, according to HR Acuity, a company that helps employers track internal complaints and investigations.

“It happens every day of the week” at large companies, said Janine Yancey, an employment lawyer and founder of HR compliance firm Emtrain.

The decision on whether to offer a payout usually begins with a question: Is there truth to the claims?

Employers will often attempt to quickly investigate the matter, usually by interviewing those involved or pulling emails, texts and chat messages between colleagues on work devices. If companies find the allegations are at least partly substantiated, they are likely to offer a more generous settlement, lawyers and HR executives say.

In other cases, companies might feel the allegations are bunk—but still opt to settle. That can be for any number of reasons. Say a startup is trying to raise new funding, said Fisher Phillips’s Stein. The last thing they might want is to spook investors with a potential lawsuit.

Part of the calculation is the cost of the distraction, Yancey said. “For business executives, your time is money. These conflicts create friction and noise,” she said. The people at the center of the allegations lose sleep, stop eating and often can’t work productively. “It makes more economic sense to pay money and move on. Flat-out,” she said.

Often the employees lodging allegations prefer to settle quietly and move on too, lawyers say. If claims—especially salacious ones—become public, they can dog a person’s career, making it harder to find future jobs.

How much companies are willing to pay can vary widely. For many routine settlements, employers try to offer no more than two years’ compensation, said LeShanda Davis, a senior director of employee relations. But companies weigh many factors when determining amounts, including their degree of fault, the seniority of the people involved, the cost of litigation and the risk someone could generate significant attention with their claims.

“You’re paying for that individual to be an alum, not an adversary,” Davis said.

Some employers prefer to fight and be as public about it as they can. When a lawyer in billionaire Bill Ackman’s family office requested two years’ severance, instead of the three months offered, Ackman turned to social media for advice and affirmation, writing a 2,400-word post on X in April. The lawyer had cited an unsafe workplace, a description Ackman rejected, vowing to “fight this nonsense to the end of the earth.”

For employers, the other complicating factor is that even a settlement might not keep things quiet. A number of states, including California, now bar employers from using nondisclosure agreements to silence workers speaking out about workplace misconduct, including sexual assault, harassment and labor and safety violations.

JPMorgan’s offer to settle with the banker, Chirayu Rana, didn’t keep the claims from going viral. Rana didn’t take the $1 million—which was equivalent to less than two years of his compensation at the bank, the Journal previously reported. Instead, he ultimately went public.

After Rana filed the suit in a New York state court, AI-generated videos of Rana and the female banker quickly proliferated across the internet.

The lawyers for the female colleague, named in the lawsuit as Lorna Hajdini, have said they are entirely made up and that the two never had any sexual relations. An attorney for Rana didn’t respond to a request for comment but has said the truth would come to light in court proceedings. “Whether my client’s civil rights were violated will be determined in a court of law,” attorney Daniel Kaiser said last week.

Employment disputes rarely generate such attention or lurid claims, said Stewart Schwab, a professor at Cornell Law School. Still, the odds of a prelitigation dispute staying quiet are also likely going down in the AI and social-media era.

Now, “if it gets out,” Schwab said, “it really gets out.”

New research suggests that bonuses make employees feel more like a mere cog in a wheel.

The sports-car maker delivered 279,449 cars last year, down from 310,718 in 2024.

Dubai International Financial Centre (DIFC) reaffirmed the strength and resilience of its ecosystem, with global institutions across banking, insurance, wealth and innovation continuing to back Dubai and the UAE as a long-term growth hub. Despite regional uncertainty, firms are deepening their presence, supported by a stable regulatory framework, strong connectivity, and access to high-growth markets across MEASA.

7 minDubai International Financial Centre (DIFC) today reaffirmed the strength, resilience and long-term outlook of its ecosystem, as global clients across banking, insurance, wealth and innovation sectors expressed continued confidence in Dubai and the UAE.

Essa Kazim, Governor of DIFC, said: “Over the past few weeks, countries in the Middle East have been navigating a period of regional uncertainty together. During these times, the true strength of DIFC has been our clients and community. What defines us is a shared belief in long-term opportunities that Dubai and the UAE offer to access the 77 markets across the Middle East, Africa and South Asia.

Together, we are building the future of finance and advancing Dubai’s journey towards becoming one of the world’s top four global financial centers.”

Arif Amiri, Chief Executive Officer of DIFC Authority, said: “From global banks to FinTech disruptors, firms operating within DIFC say the current environment has not prompted retreat but rather reinforced the strategic importance of Dubai as a gateway to growth across the region. For many, the current environment serves as a reminder of why they chose DIFC in the first place: a stable and enabling legal and regulated framework, and globally connected platform capable of unlocking future growth.”

Recent milestones reinforce DIFC’s trajectory, including Dubai’s rise to 7th globally in the Global Financial Centres Index in March, which is its highest ever ranking and underscores sustained global confidence in the emirate’s financial ecosystem.

An integral part of the DIFC ecosystem are 290 banks and capital markets firms, including 17 of the world’s 19 global systemically important banks. This reflects the vital role DIFC plays in connecting major players to opportunities in the region and being the bridge between markets in the East and West. Global banking leaders from Citi, Julius Baer and Standard Chartered highlighted DIFC’s critical role as a stable platform connecting international capital with opportunity.

Ebru Pakcan, Middle East & Africa Cluster and Banking Head at Citi, noted: “At a time when geopolitical dynamics are reshaping markets, the ability to deliver cross-border solutions, maintain liquidity, and stay close to clients is critical. DIFC enables Citi to do exactly that. Citi has maintained a continuous presence in the Middle East for over six decades, recognizing its integral role in our global network.”

“Since establishing a presence at DIFC in 2006, we’ve seen the financial hub transform into a strategic platform that connects capital, clients, and opportunities across the Middle East, Africa, and South Asia. From supporting sovereign issuances and corporate funding to enabling efficient treasury and liquidity management, DIFC allows Citi to operate at the center of regional and global capital flows.”

Regis Burger, Head of Middle East & Africa and Chief Executive Officer, Julius Baer (Middle East) Ltd, highlighted: “The UAE has established itself as a leading global financial center and the foundations that underpin that position remain firmly intact. Its connectivity, business-friendly regulatory environment, tax-efficient framework, and world-class infrastructure continue to set it apart and attract investors, entrepreneurs, and institutions from around the world. DIFC has been at the heart of that story.

Julius Baer saw that potential before most. As the oldest organization in DIFC, we were here at its founding, driven by a conviction that this region would emerge as one of the world’s most important centers of wealth creation and a magnet for global capital. That belief has only deepened over two decades of being embedded in this market, across our offices in the UAE, working closely with our clients in creating and preserving their wealth and building relationships across generations.

The region is approaching a historic transfer of nearly $1 trillion in wealth across generations by 2030, and the families navigating that journey require more than financial expertise. As an organization with its own origins as a family business, Julius Baer has been through the entire business transformation cycle and understands what it takes to guide clients and their families through it.

We remain deeply committed to the UAE, the wider region, and to the clients and partners who trust us with their financial futures. That commitment does not waver in periods of uncertainty and it is precisely in these moments that our role as a wealth manager matters the most.”

Rola Abu Manneh, Chief Executive Officer, UAE, Middle East, and Pakistan at Standard Chartered, added: “We have been in the UAE for over 65 years, and DIFC has been our regional home since 2004. Our commitment to the country is firm and unchanged.

The UAE entered this environment from a position of strength, supported by robust balance sheets, strong institutions, and a well-regulated financial system.

Client activity across the UAE reflects continued engagement, with businesses using the UAE as a base to access opportunities across regional and international markets. Through our global network, we connect clients to those opportunities while ensuring continuity of service and access to banking solutions.”

The insurance industry has been growing in DIFC with gross written premiums doubling to over $4.2 billion in the last four years. Insurance leaders are emphasizing DIFC’s role in strengthening risk management capabilities across the region.

Omar Gemei, Senior Executive Officer of Marsh DIFC and Head of Global Placement & Bowring Marsh, India, Middle East & Africa, said: “Dubai has firmly established itself as a leading international hub for the insurance and risk management sector. It brings together insurers, brokers, and risk professionals to support clients facing increasingly complex and interconnected risks, underpinned by a strong understanding of the globally evolving business and regulatory landscape.

DIFC has been a key catalyst in that growth, providing a business-friendly environment that attracts global firms and supports innovation. For the insurance and risk management community, it provides access to regional markets writing global and regional business, reinforced by Dubai’s continued investment in infrastructure, talent, and regulation to further grow the sector.”

Dubai is home to the highest concentration of wealth in any Middle Eastern city and according to Henley & Partners, in 2026, the UAE has so far attracted more millionaires than any other country in the world. This has made DIFC the region’s preferred hub for wealth and asset management, with over 500 firms from the sector choosing to operate from the Centre.

Peter Clark, Chief Executive Officer, Bentley Reid, said: “Bentley Reid has been advising clients for almost fifty years, and over that time, we have successfully navigated diverse economic, market and political uncertainties. The lesson we draw from each of these episodes is that it seldom pays to make knee-jerk reactions or allow short-term turbulence to drive major strategic decisions.

Whilst the firm is a relative newcomer to DIFC, it soon became apparent that the UAE’s economic success has been built on several key fundamentals: its favorable fiscal environment, a pro-business culture, a dynamic and increasingly diverse economy, an exceptional quality of life and deep global connectivity. We are confident that this compelling mix will reassert itself as soon as the regional situation eases, rewarding those with patience and resolve.

The families, entrepreneurs and businesses who typically fare best during uncertain periods are those who focus on the long-term and return to first principles – asking themselves why they committed to a particular jurisdiction and whether those reasons still hold. In the case of Bentley Reid and the DIFC, the answer is an unequivocal yes.

This is reinforced by what we are witnessing on the ground. Very few – if any – in our HNW and UHNW network view current events as an existential threat to Dubai’s trajectory, or to their decision to make the UAE their home. This includes wealthy families planning relocations to the region; few are abandoning those plans, although some are understandably choosing to let the situation settle before finalizing their arrival.

For our part, Bentley Reid came to the DIFC for the long term. What we have seen, both leading up to the conflict and ever since, points to Dubai continuing to offer significant advantages to wealthy families and their advisers. If anything, the current environment reinforces the value of having a trusted and experienced international wealth manager at one’s side. That is exactly what Bentley Reid is here to provide.”

ICICI Prudential Asset Management Company established an office in DIFC in February this year. Nimesh Shah, Managing Director and Chief Executive Officer of ICICI Prudential Asset Management Company highlighted: “Dubai and DIFC are a natural fit for ICICI Prudential AMC’s global ambitions given their strong regulatory ecosystem, global connectivity and access to institutional investors. Our presence here reflects our confidence in India’s long-term growth story and our commitment to building enduring partnerships with global investors seeking India-focused opportunities.”

DIFC continues to be at the leading-edge for developing clear laws, regulations and operating frameworks for the digital assets and FinTech industries.

In 2020, Ripple established their regional headquarters for the Middle East and Africa in DIFC. This month, they announced a further expansion to their presence in the Centre.

Reece Merrick, Managing Director, Middle East and Africa, Ripple commented: “Ripple established its regional headquarters for the Middle East and Africa in the UAE in 2020. Since then, we have substantially grown our presence, expanding our team, signing new clients and forging innovative partnerships, to meet growing demand for digital assets infrastructure. During this time, we’ve also witnessed first-hand how much the country has strengthened its position as a global financial hub.

This doesn’t happen without a strong foundation, and the UAE provides exactly that: a forward-looking market underpinned by clear and progressive regulation that has reinforced its position as one of the leading global centers for our industry.

The local authorities have played a central role in establishing the UAE as one of the world’s leading hubs for digital assets. The clarity and ambition of the regulatory frameworks that have been put in place, combined with a mature financial ecosystem and access to institutional capital, gives companies the confidence to lay solid foundations here. That is a hard thing to build, and the UAE has achieved it, setting a benchmark not just for the wider region, but globally.”

Stake has been using its DIFC presence to develop innovative PropTech solutions, recognizing the importance of the real estate industry to the UAE. Manar Mahmassani, Co-Founder & Co-CEO, Stake commented: “Stake was born in Dubai in 2021, when global uncertainty was at its peak. Today we are the largest fractional investment platform in the world because we started here.

“When we launched Stake, choosing to set up in DIFC was a no-brainer. It wasn’t just about operating in the most credible financial jurisdiction in the region. As a start-up, DIFC gave us exactly what we needed: a launch pad and a plug-and-play co-working environment that was bustling with innovation. The address, the infrastructure, the retail and F&B, the caliber of professionals in every corner, and the proximity to our regulator, the DFSA – DIFC offered us as founders and our teams a work-play lifestyle that is genuinely second to none.

“For a FinTech like Stake, building the future of real estate investment demands regulatory clarity, access to world-class capital partners, and a standard of governance that global investors recognize instantly. DIFC delivers all three, and it has been one of the most important accelerants of our growth.”

The payments industry is significant in the UAE and Taptap Send has been using Dubai to develop their offering. Michael Faye, Chief Executive Officer at Taptap Send added: “DIFC has been a genuine home for our team, our relationships, and our ambition. It has built something rare: a world-class environment where ambitious FinTech companies can access deep talent, global connectivity, and an infrastructure that leads international standards. For Taptap Send, the UAE is exactly the right base from which to do it, connecting underserved communities to the global financial system from one of the world’s great international hubs. That ambition mirrors our own, and I can’t imagine a better place to pursue it.”

The collective voice of global financial institutions, insurers, asset managers and future-focused innovators reinforces DIFC’s position as a resilient, trusted and forward-looking financial ecosystem. Despite a complex global backdrop, firms continue to deepen their presence, guided by confidence in the Centre’s internationally credible legal and regulatory environment, global connectivity and long-term growth prospects.

As momentum builds across traditional and emerging sectors alike, DIFC remains central to enabling capital flows, fostering innovation and supporting sustainable economic expansion, further cementing Dubai’s standing as a leading global financial hub.

Parts for iPhones to cost more owing to surging demand from AI companies.

Chris Dixon, a partner who led the charge, says he has a ‘very long-term horizon’

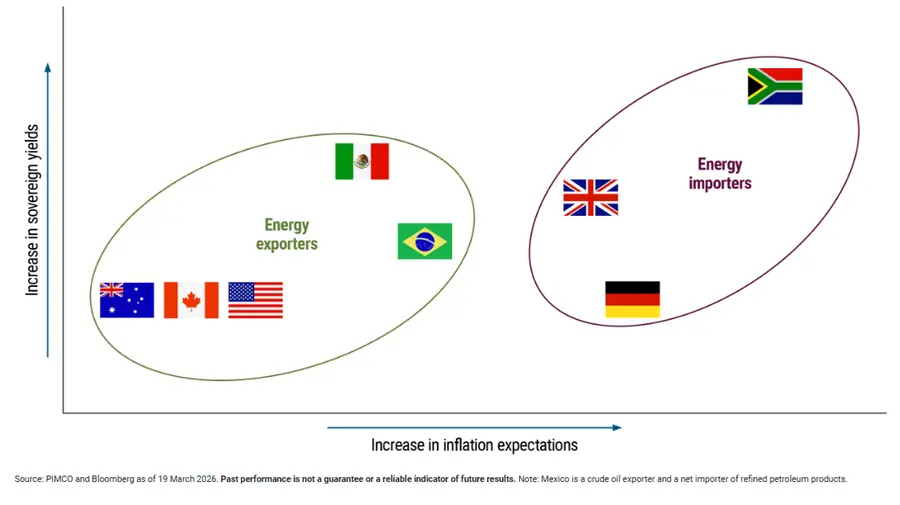

In times of heightened uncertainty, investing shifts from prediction to resilience. With geopolitical risks impacting confidence, energy prices, and global growth, the focus turns to liquid, high-quality assets built to withstand multiple scenarios. As volatility rises and dispersion widens, diversification, strong fixed income positioning, and portfolio flexibility become essential to navigating an increasingly complex market environment.

4 minAt times of intensified uncertainty and dispersion like today, investing becomes less about forecasting and more about favouring more liquid, high quality assets that can be resilient across a variety of scenarios.

Global growth has been more resilient than expected despite growing divergence below the surface. What has changed is the addition of a major new source of risk: the conflict in the Middle East. If this proves to be a short-term disruption, as markets are currently pricing, then the baseline outlook still assumes moderate global growth. However, a prolonged disruption would pose more significant challenges and increase global recession risks.

Geopolitical risks tend to transmit to the economy through changes to consumer and business confidence, financial conditions, and – most importantly today – energy prices. The Strait of Hormuz, a critical waterway for oil and energy shipments, remains effectively blocked. Similar to Russia’s invasion of Ukraine in 2022, this threatens to spark a global energy supply shock.

Energy supply shocks are stagflationary

Unlike in 2025, when divergent trends left global growth broadly unchanged, the Middle East conflict is likely to be stagflationary, lifting inflation while hurting growth. We see four main transmission channels: higher energy and food prices; disrupted supply chains and trade flows; tighter financial conditions; and lower business and consumer confidence.

Negative oil supply shocks are inflationary for all economies, while growth effects will differ. Higher energy prices are stagflationary for net oil importers – transferring income abroad through more expensive energy imports while reducing household real (inflation-adjusted) income and business real profit – and expansionary for net oil exporters.

Within developed markets, Europe, the U.K., and Japan are energy importers and face larger downside growth risks. Canada and Australia should benefit from their net energy export status. Two decades of shale production increases have turned the U.S. from a net energy importer to a slight exporter. However, the U.S. is still a large economy with an energy sector as opposed to a commodity economy. Since energy is an important input into all goods it imports, the U.S. will likely still behave as a net energy importer to some extent.

Central banks face a tug of war – but this isn’t 2022

The risk of higher inflation alongside lower growth puts central banks in a tricky spot. Conventionally, central banks tend to look through supply shocks, especially in economies that are net energy importers. After the elevated post-pandemic inflation period, however, central banks will be closely focused on the risk that a large supply shock could lead to more persistent pressures as inflation expectations and wages also adjust higher.

Yet economies are in much different positions than they were in 2022. At that time, the world was still dealing with pandemic-related pent-up demand, and governments had injected trillions of dollars into the private sector. The result was a large demand shock on top of a large supply shock. Labor markets were also extremely tight, driving both nominal wages and prices higher.

Today, by contrast, fiscal policy is tight across many regions as elevated post-pandemic sovereign debt forces restraint. Labor markets are much looser. Monetary policy is already neutral to slightly restrictive across most developed market economies.

As a result, economies are much more likely to adjust to the current shock through lower real incomes, weaker nominal wage adjustments, and greater recessionary risks.

Investment implications: resilience, quality, and liquidity

This is not an environment set up to reward bold forecasts or narrow bets. Instead, today’s conditions favour more liquid, high quality portfolios built to weather shifts in market sentiment and a range of potential outcomes.

Resilient headline growth alongside widening dispersion strengthens the case for high quality fixed income. Starting yields are much higher today than in 2022, providing cushion against inflationary tail scenarios and strengthening the role of bonds as both a return generator and a hedge against downside risks.

Markets rarely price geopolitical risk well. When there is a global shock, portfolio liquidity can allow investors to take advantage of market inefficiencies and valuation gaps that arise. As volatility rises and dispersion widens, the ability to manage downside risk and redeploy capital as conditions evolve matters more than trying to capture incremental yield by forfeiting liquidity.

High quality bonds once again play a meaningful role in portfolios and look attractive across a variety of economic scenarios. For portfolios that have drifted heavily toward equities, this is a practical moment to consider rebalancing. Yields across more liquid fixed income remain attractive, laying a solid foundation for market-driven income and return.

We prefer a modest overweight to duration and more balanced curve exposure, as yields look attractive across a range of maturities.

The case for global diversification remains strong. Differences across countries are widening, creating both risks and opportunities.

Looking across the continuum of public and private credit today, we see the greatest value in areas including U.S. agency mortgage-backed securities (MBS), investment grade issuers with stable, predictable cash flows, and high quality securitized credit.

Currency positioning matters more in this environment, particularly given the growing divergence between energy exporters and importers. Inflation-sensitive assets also deserve a more deliberate role in portfolios today. Commodities, real assets, and Treasury Inflation Protected Securities (TIPS) can help hedge real-world purchasing power and diversify returns when traditional asset relationships become less reliable. These exposures may help improve portfolio resilience.

Conclusion – recentre towards fixed income?

This is a market that rewards preparation for an uncertain set of outcomes. Higher yields, wider dispersion, and greater volatility create a favourable backdrop for active management when portfolios are built with liquidity and flexibility in mind.

For investors, this is a moment to consider recentring portfolios toward fixed income, to use global diversification and inflation tools intentionally, to treat liquidity as an asset, and to emphasise quality and resilience in the face of layered uncertainty.

Parts for iPhones to cost more owing to surging demand from AI companies.

Americans now think they need at least $1.25 million for retirement, a 20% increase from a year ago, according to a survey by Northwestern Mutual

Dubai showcases its advanced manufacturing ecosystem at Make it in the Emirates 2026, reinforcing its position as a global hub for industry, investment, and export-driven growth.

3 min

The Dubai Department of Economy and Tourism (DET) will showcase the emirate’s advanced, future-ready manufacturing ecosystem at the Dubai Pavilion during ‘Make it in the Emirates 2026’, the fifth edition of the UAE’s flagship industrial forum, taking place from 4–7 May at ADNEC Centre Abu Dhabi. The participation comes at a time when Dubai continues to demonstrate operational continuity and economic resilience, reinforcing its position as a stable and globally connected industrial hub.

Held under the theme ‘Advanced Industry. Emerging Stronger’, the forum reflects the UAE’s commitment to building a sustainable, technology-driven industrial base anchored in innovation and global partnerships. Dubai enters the forum bolstered by a standout performance, having achieved 6.4% GDP growth in Q4 2025, with total GDP reaching AED937 billion for the full year, underscoring steady economic momentum despite global headwinds. DET’s participation aligns with the goals of the Dubai Economic Agenda, D33, which targets more than doubling manufacturing value-added output in the decade up to 2033, while reinforcing Dubai’s position as a leading destination for industrial investment.

As one of the UAE’s most significant industrial gatherings, ‘Make it in the Emirates’ unites government entities, national champions, manufacturers, and SMEs to drive tangible outcomes, from offtake commitments and investment deals to technology transfer and strategic partnerships.

DET will present Dubai as a globally connected hub for advanced manufacturing, underpinned by world-class infrastructure, integrated logistics, and seamless access to international markets. Attendees will gain an understanding of how manufacturers operating in Dubai benefit from connectivity to more than 130 export destinations, supported by Comprehensive Economic Partnership Agreements and advanced customs facilitation measures that ensure reliable trade flows. At the Dubai Pavilion, DET will bring together key entities including Dubai Industrial City, National Industries Park, Dubai Integrated Economic Zones Authority (DIEZ), Dubai Chambers, Dubai Future Foundation, Food Tech Valley, and other strategic partners.

His Excellency Hadi Badri, CEO of the Dubai Economic Development Corporation (DEDC), the economic development arm of DET, said: “Dubai’s leadership has consistently taken decisive, policy-driven action to safeguard growth and stability. Our manufacturing sector reflects this approach: it is diversified, technologically advanced, and fully integrated into global value chains. Even amid regional pressures, business continuity remains seamless across logistics, trade and industrial operations. Through the Dubai Economic Agenda, D33 we are also strengthening our value proposition for manufacturers by enabling new investments and plant expansions through tailored incentive frameworks. These include support mechanisms designed to enhance cost competitiveness, reduce barriers to entry, and accelerate scale-up for high-impact projects.

Our participation in ‘Make it in the Emirates’ is an opportunity to translate that vision into partnerships and close the deals that will strengthen local manufacturing, drive economic momentum, and further reinforce Dubai’s position as a leading hub for export-led growth.”

The Dubai Pavilion will serve as a central platform to engage investors, manufacturers, and stakeholders, offering insights into the emirate’s competitive advantages. DET representatives will also participate in high-level engagements focused on industrial development, investment facilitation, and market expansion into and from Dubai.

As part of its participation, DET will highlight a range of initiatives designed to support industrial scale-up and export expansion. These include the Export Assistance Programme (EAP), which enables Dubai-based manufacturers to access international markets, and the Elite Buyer Programme, which strengthens Dubai’s position as a global sourcing hub. Additional initiatives such as Industry 4.0 enablement programmes, In-Country Value (ICV) promotion, and industry-friendly power policies will also be showcased, reinforcing Dubai’s commitment to advanced manufacturing technologies and local capacity building.

DET will also use the platform to strengthen national collaboration, working closely with the Ministry of Industry and Advanced Technology and other stakeholders to ensure alignment with the UAE’s broader national strategy. Several strategic partnerships with major entities in the logistics and banking sectors are expected to be formalised during the forum, further demonstrating sustained institutional confidence in Dubai’s industrial trajectory.

Building on the strong investment momentum of previous editions, this year’s ‘Make it in the Emirates’ represents a pivotal platform for translating D33 industrial ambitions into measurable outcomes for businesses across the emirate and beyond.

The sports-car maker delivered 279,449 cars last year, down from 310,718 in 2024.

Interior designer Thomas Hamel on where it goes wrong in so many homes.

Global markets show resilience despite a major energy shock triggered by the Strait of Hormuz closure, with oil prices surging and supply disruptions hitting several countries. Strong reserves, policy support, and the AI-driven economic boom have helped sustain growth—for now.

4 min

One of the major surprises about the gravest energy shock since the 1970s is how resilient much of the world has been so far.

The closure of the Strait of Hormuz has yanked around 13 million barrels of oil a day from global energy supplies. Blackouts have hit Pakistan, the Philippines has imposed a four-day workweek, and countries including Slovenia and Bangladesh have rationed fuel. The risk that the world sinks into recession is rising with each day the waterway remains shut. The price of Brent crude, the global oil benchmark, has risen more than 50% since the strait was closed.

Even so, in the two months since the strait was closed by Iran in response to U.S. and Israeli attacks, many of the world’s major economies have been soldiering on in contrast to the swift downturns that accompanied similar energy crises in the 1970s and 1990s. Stock markets are touching record highs.

This resilience reflects ample energy reserves, policies to help consumers, and the offsetting effects of the artificial-intelligence boom that is powering trade and business investment in the U.S. and beyond.

It also highlights an underappreciated shift in the workings of the global economy. Over the years, countries have become steadily more energy efficient, squeezing more economic activity out of each drop of oil or cubic meter of natural gas burned. The energy needed to generate a dollar of gross domestic product, adjusted for inflation, has since 2000 fallen by about a third in the U.S. and Europe and by about 40% in China, according to World Bank data.

Better energy efficiency “cushions the shock” from supply disruptions, International Monetary Fund Managing Director Kristalina Georgieva said in April. Underlining the global economy’s resilience, the IMF said that assuming energy flows through the strait resume by midyear, it expects only modestly slower growth this year than in 2025, at around 3.1% versus 3.4% last year.

Of course, a more severe test of the global economy’s durability will occur if the conflict persists and the strait stays closed. The cease-fire between the U.S. and Iran is holding, but so far there is no agreement to reopen the waterway, which is also subject to a U.S. blockade aimed at starving Iran of imports and revenue.

Poor countries that don’t have reserves to draw on and are on the sidelines of the AI boom are already struggling, with shortages closing factories and high import prices for energy straining threadbare government budgets.

If the strait remains closed into next year, the IMF warned global growth in 2026 could sink to around 2%, bringing the world economy close to recession.

When Russia’s invasion of Ukraine triggered a similar energy shock in 2022, consumer prices were already surging in big economies as pent-up demand collided with strangled supply as they reopened after the pandemic.

Central banks had little choice but to jack up interest rates almost immediately. This time around, central banks don’t face the same pressure from domestic inflation as they weigh the risks from a bump in global energy prices. Central banks in the U.S., Europe and Japan held their benchmark interest rates steady this week as they assess the effects of the war on their economies.

“The economic outlook remains highly uncertain, and the conflict in the Middle East has added to this uncertainty,” Federal Reserve Chair Jerome Powell said Wednesday.

Compared with 2022, “the starting point is more benign,” said Mansoor Mohi-uddin, chief macro strategist at the Bank of Singapore, a private bank. Government spending on defense and other priorities is also helping economic activity while the strait remains closed, he said, though he added he is concerned that higher prices and shortages could start to bite within weeks.

Since the closure of the strait, governments have swung into action to stabilize energy supplies and keep a lid on price rises for consumers.

Key to their efforts are deep reserves. Japan and Korea had around 200 days’ worth of reserves on hand in January, according to the International Energy Agency. Europe had 130 days’ supply. China’s enormous stockpile, estimated by the U.S. at around 1.4 billion barrels, is enough to power its economy for about 100 days.

For Asia especially, another counterweight to strains from the energy shock has been buoyant exports. The AI boom has meant ravenous demand in the U.S. and elsewhere for Asia-made chips, electronics and machinery to power data centers.

Exports from Japan were 12% higher in March than a year earlier. In South Korea, they rose almost 50% and in Taiwan, they rocketed 68%.

“AI is papering over the cracks,” said Stefan Angrick, head of Japan and frontier markets economics at Moody’s Analytics in Tokyo.

A deeper reason for the global economy’s resilience compared with previous energy shocks is greater energy efficiency. Advanced economies have shifted to less energy-intensive services such as finance and healthcare from more energy-hungry manufacturing.

Renewables have also played a role—both solar and wind lose less energy as heat than burning fossil fuels. Consumer appliances have been re-engineered to use less electricity and firms have squeezed out improvements in industrial processes to save energy.

German engineering giant Thyssenkrupp has improved its use of energy through measures including capturing waste heat, reducing leaks and replacing lighting and other components with newer, more energy-efficient alternatives, according to recent disclosures on its sustainability efforts.

France’s Saint-Gobain, a construction firm, said in a 2025 report that it has started using AI to monitor and adjust energy use in its fiberglass furnaces to boost efficiency, and is replacing natural gas with more efficient fuels such as hydrogen. Modeling by the IMF suggested that energy-saving measures adopted by European companies in the aftermath of the 2022 crisis reduced by about one-third the long-term damage to the European economy.

With this latest energy crisis, some economists worry about how many more shocks the global economy can take. Hits from the pandemic, energy and U.S. tariffs are causing ripples that could outlast the shocks themselves, such as weaker investment, subdued business and consumer confidence, and strained public finances, said Aaditya Mattoo, director of development research at the World Bank.

“You have this succession of shocks,” Mattoo said. Countries, especially developing ones, “face this tough trade-off between providing relief today and sustaining growth tomorrow.”

Paine Schwartz joins BERO as a new investor as the year-old company seeks to triple sales.

Following the devastation of recent flooding, experts are urging government intervention to drive the cessation of building in areas at risk.

Central Bank of the UAE has kept its base rate at 3.65%, following the US Federal Reserve’s decision to hold its benchmark rate. The UAE central bank also maintained borrowing rates at 50 basis points above the base rate, keeping monetary policy stable.

< 1 min

The Central Bank of the UAE (CBUAE) has decided to maintain the Base Rate applicable to the Overnight Deposit Facility (ODF) at 3.65%.

This decision was taken following the US Federal Reserve’s announcement today to keep the Interest Rate on Reserve Balances (IORB) unchanged.

The CBUAE has also decided to maintain the interest rate applicable to borrowing short-term liquidity from the CBUAE at 50 basis points above the Base Rate for all standing credit facilities.

The Base Rate, which is anchored to the US Federal Reserve’s IORB, signals the general stance of monetary policy and provides an effective floor for overnight money market interest rates in the UAE.

Paine Schwartz joins BERO as a new investor as the year-old company seeks to triple sales.

Saudi Aramco’s Q1 2026 net profit is forecast to reach SAR 108.8 billion, up 13.8% YoY and 56.7% QoQ, driven by higher oil prices and stronger refining margins, according to AlJazira Capital.

< 1 min

Saudi Aramco’s net profit after minority interest is expected to rise by 13.8% year-on-year (YoY) and 56.7% quarter-on-quarter (QoQ) to 108.8 billion Saudi riyals ($29.01 billion) in the first quarter of 2026, according to a report by AlJazira Capital.

The net profit is anticipated to increase by 12.6% from the adjusted net profit reported in Q4 2025.

The sequential growth in adjusted net income is likely to be driven by crude oil prices surging 24.8% QoQ, due to better refining margins and reductions in certain operating costs, wiping out the impact of lower production of 600,000 barrels per day (bpd) of crude and 700,000 barrels of oil equivalent per day of hydrocarbons.

Revenue is estimated at SAR 455.3 billion, up 6% YoY and 9.4% QoQ. The upstream revenue is expected to drive topline growth, rising 13.1% QoQ, while the downstream revenue is forecast to rise 6.8% QoQ.

The Saudi-listed oil giant’s revenue in 2026 is projected to increase to SAR 1.9 trillion, while net income is expected to rise to SAR 427 billion.

The brokerage estimates the average oil price of around $86 per barrel.

“We expect higher crude oil prices this year and flexibility to divert exports from east to west coast to reflect positively on Aramco’s revenue and earnings in 2026.”

AlJazira Capital has assigned an “Overweight” rating to Aramco stock, with a target price of SAR 29.6 per share, subject to an upward revision.

Aramco will publish its Q1 2026 results on May 1.

The sports-car maker delivered 279,449 cars last year, down from 310,718 in 2024.

Stocks slipped while oil prices climbed as U.S.–Iran tensions escalated, with Brent crude rising 5.6% to $95.48 a barrel and the S&P 500 and Nasdaq pulling back from recent highs; despite geopolitical pressure, market moves remained relatively muted, supported by strong economic data as investors turn to a busy earnings week with expectations for continued profit growth.

2 min

Stocks slipped and oil prices rose Monday, with fresh tensions between the U.S. and Iran casting a shadow over Wall Street.

Brent crude futures, the international oil benchmark, rose 5.6% to $95.48 a barrel. Major stock indexes fell, with the S&P 500 and Nasdaq composite retreating from record levels reached last week.

The latest strains between the U.S. and Iran unwound some of the optimism that swept through markets last week, culminating Friday when Iran said the Strait of Hormuz was “completely open.”

U.S. negotiators are expected to arrive in Pakistan tonight for talks with Iran this week, although Tehran has cast doubt on its participation. In a social-media post, President Trump threatened to attack Iranian infrastructure if the country doesn’t make a deal.

The tech-heavy Nasdaq fell 0.3%. The S&P 500 declined 0.2% and the Dow Jones Industrial Average fell about 5 points, or less than 0.1%.

Those declines were shallow compared to selloffs earlier in the war. Oil prices remained below its highs earlier in the conflict, when prices were around $120 a barrel. At the same time, stocks tied to the real economy rallied.

“The pretty muted response by the market tells me that the market’s in good shape,” said Sean Clark, chief investment officer at Clark Capital.

The Russell 2000 index of smaller companies gained 0.6% to close at its third straight record and notch its best 14-session performance since 2020. The Dow Jones Transportation Average, which tracks the railroads, airlines and truckers that move the goods powering the economy, rose 4%.

Walmart, a bellwether for the U.S. economy, reached a market capitalization of $1 trillion Monday, becoming the ninth-largest U.S. company, according to Dow Jones Market Data.

Elsewhere, psychedelic-drug stocks jumped after Trump signed an executive order Saturday to speed up research and patient access to new treatments for mental-health conditions. Shares of Compass Pathways, GH Research and AtaiBeckley all rose more than 17%.

Some investors said that despite worries the war would fuel a recession, strong data on jobs and earnings have offered assurance that the economy is on solid footing. Many still expect that the war will end sooner rather than later, and limit its impact on markets and the economy.

“The reality is, the present level of uncertainty in the latest conflict is not going to derail broad economic growth,” said Kieran Osborne, chief investment officer at Mission Wealth.

Nearly a fifth of S&P 500 companies report earnings this week, including Tesla, Boeing, Intel and Lockheed Martin. Early results indicate companies are on track for a sixth-straight quarter of double-digit earnings growth, according to FactSet.

Elsewhere, investors looked to Federal Reserve chair nominee Kevin Warsh’s confirmation hearing before the Senate Banking Committee on Tuesday. He plans to say that the central bank’s independence is self-enforced, and that price stability is the Fed’s “plot armor,” according to a copy of his remarks.

Following the successful launch of its Palais Collection, MAISON de SABRÉ has unveiled a new modular handbag system offering more than 720 styling combinations.

AI-driven fraud is accelerating faster than organizations can respond, with a new report by Association of Certified Fraud Examiners and SAS revealing that just 7% feel well-prepared to detect or prevent it, as deepfakes, digital forgery, and consumer scams surge worldwide; while AI adoption is rising, gaps in governance, explainability, and overall readiness continue to leave institutions exposed as threats scale faster than defenses.

4 min

As fraudsters sprint ahead with AI, organizations report they are struggling to keep pace. That’s the sobering verdict delivered in the latest fraud research by the Association of Certified Fraud Examiners (ACFE) and data and AI leader SAS: Only 7% of anti-fraud professionals say their organizations are more than moderately prepared to detect or prevent AI-fueled fraud – even as criminals hijack inexpensive and plentiful AI tools to drive social engineering schemes, digital forgery and consumer scams to record highs.

The 2026 Anti-Fraud Technology Benchmarking Report – the fourth installment in a research series debuted by the ACFE and SAS in 2019 – is based on a survey of 713 fraud fighters across eight regions worldwide.

“The data paints a worrisome picture: fraud is evolving faster than most organizations can defend against it,” said John Gill, J.D., CFE, President of the ACFE. “AI-powered threats aren’t on the horizon – they’re already here, and they’re accelerating quickly. The profession has made real strides in adopting AI, but this report is a wake-up call. Organizations that don’t strengthen their defenses against AI-charged fraud risk as others do will become bigger targets.”

As fraud risk rises globally, the UAE and Saudi Arabia are uniquely positioned to lead the next generation of fraud prevention. Strong regulatory alignment, government-led digital transformation, and modern financial infrastructure give both markets a structural advantage. With central banks CBUAE and SAMA acting as ecosystem orchestrators, the region has a rare opportunity to leapfrog legacy approaches and move directly to supporting a secure, seamless, and future-ready financial ecosystem.

“Few regions combine high growth with such strong regulatory leadership,” said Abed Hamandi, Senior Director, EMEA Consulting, Fraud and Security Intelligence Practice, SAS. “The UAE and Saudi Arabia are not constrained by legacy in the same way as many mature markets. By embracing real-time, AI-driven, and identity-centric fraud prevention, they can stop fraud before it happens, while delivering the low-friction customer experiences that modern digital economies demand.”

Industries at a crossroads – and in the crosshairs

Respondents represent more than a dozen industries, most prominently government and public sector (26%) and banking and financial services (23%), alongside meaningful participation from professional services, manufacturing, insurance, technology, education, energy and health care. Survey insights reveal that:

- Fraudsters are winning the AI race. Every AI-powered fraud modality examined has risen over the past two years, according to the anti-fraud professionals surveyed. Deepfake social engineering saw the sharpest surge, with 77% of respondents reporting a slight-to-significant increase – followed closely by consumer fraud/scams (75%), generative AI document fraud/forgery (75%) and deepfake digital injection (72%). Looking ahead, 55% expect deepfake social engineering and GenAI document fraud/forgery to increase significantly over the next 24 months.

- AI and machine learning (ML) adoption are accelerating but remain far from ideal. One-quarter of organizations (exactly 25%) now use AI/ML in their anti-fraud programs, according to respondents, up from 18% in 2024. Another 28% expect to adopt it by 2028. For organizations still on the sidelines, the window to build AI competency before competitors and criminals widen the gap is narrowing fast.

- Governance lags dangerously behind AI adoption. Nearly nine in 10 (86%) organizations rate accuracy of results as important or very important in adopting GenAI, yet less than one in five (18%) respondents say their organization tests AI models for bias or fairness. Similarly, 82% say explainability is important, but just 6% feel completely confident explaining how their AI/ML models make anti-fraud decisions. For banks, insurers and other regulated entities in particular, deploying AI in this manner risks regulatory consequences and legal liability on top of reputational damage.

- Budgets are growing – but so are constraints. More than half of respondents (55%) expect their organizations to increase their anti-fraud technology budgets over the next two years. Even so, budgetary and financial restrictions remain the leading barrier to implementation, cited as a major or moderate challenge by 84% of respondents.

Emerging tech: Promise, progress and the cost of waiting

Physical biometrics, agentic and generative AI – and yes, even quantum AI – the technologies transforming the war on fraud are maturing rapidly. But fraudsters’ readiness to exploit them is advancing in parallel, and bad actors have a tremendous advantage.

“Cybercriminals don’t have governance committees, and they don’t wait for budget cycles or regulatory clarity – they just act,” said Stu Bradley, Senior Vice President of Risk, Fraud and Compliance Solutions at SAS. “Every quarter business leaders spend evaluating a technology is another quarter lawbreakers get to weaponize it and find organizations underprepared.”

The question isn’t whether to adopt anti-fraud innovations, but rather, can organizations afford to wait? The study revealed these trends in value-proven, emerging technologies:

- GenAI is moving from aspiration to application. Although only 16% of respondents indicate their organizations currently use generative AI as an anti-fraud tool, another 58% plan to in the future. Among those already using GenAI, top applications are phishing and scam detection (49%), risk identification/assessment (46%) and report writing (45%).

- AI agents are hotter still. Nearly one in 10 (8%) of respondents say their organizations use agentic AI for fraud fighting, and nearly one-third (31%) more expect to deploy it by 2028 – the highest near-term adoption expectation of any emerging technology category examined.

- Physical biometrics leads emerging tech adoption – while many neglect the benefits of automation and the cloud. The use of physical biometrics is now the most widely adopted emerging technology in anti-fraud programs gauged in the study, used by nearly half of organizations (45%) surveyed – up from roughly one-third (34%) in 2022. In contrast, cloud-native fraud detection platforms and automation remain significantly underutilized, used by only 10% and 29% of organizations, respectively.

- Quantum computing’s impact on the anti-fraud battlefield is closer than most expect. Most respondents (62%) expect quantum computing and quantum AI to materially impact fraud detection and prevention by 2030 – and a surprising 11% say it already is.

Ready or not…

Whatever their level of preparedness, organizations across sectors face the same AI-accelerated fraud threats. The differentiator? Their ability to fight back. Fraud fighters must be equipped with the right data and technology – and also the appropriate speed, scale and governance – to combat modern-day risks.

Two coming 2027 models – the first of the “Neue Klasse” cars coming to the U.S. early next year – have been revealed.

Private credit is rapidly moving into consumer lending as banks pull back, with fintechs like Bilt turning to firms such as Goldman Sachs, KKR, and Blue Owl Capital to fund billions in loans through forward-flow deals; while this model fuels growth and flexibility, rising economic pressures and investor caution are beginning to test the durability of this credit boom.

5 min

When Wells Fargo told the fintech Bilt that it would no longer be the lender for its rent-rewards credit card, Bilt scrambled to find another large bank partner. When that failed, Bilt wound up with private-credit funding.

In February, Bilt struck a deal to move roughly $1.2 billion of credit-card balances with funding arranged by a group including Blue Owl Capital OWL 2.07%increase; green up pointing triangle and Stone Point Capital as well as Goldman Sachs GS 2.88%increase; green up pointing triangle and TD TD 1.19%increase; green up pointing triangle, according to people familiar with the deal.

The companies also agreed to fund hundreds of millions of dollars of credit-card balances that Bilt cardholders will incur in the future, the people said.

Consumer debt has become one of the hottest categories in private credit, increasingly sought after by funds and investment arms of insurance companies on the hunt for high-yielding investments.

Private credit is in focus on Wall Street right now because of the loans that fund managers have made to software and other companies, often as part of private-equity buyouts, that are now running into trouble. Investors are pulling money away.

In consumer debt, the private-credit engine is powering a variety of companies including financial-technology firms to turn out more and more loans.

Imagine a Harley-Davidson customer at the dealer who takes out a loan to purchase a new motorcycle. The loan is provided by Harley-Davidson Financial Services, which has a deal to sell about two-thirds of its new loans to KKR KKR 1.55%increase; green up pointing triangle and the bond giant Pimco. Funds run by those firms get a debt security backed by the hog, and Harley gets to make another loan to the next customer quickly. The customer sees no apparent difference, as Harley continues servicing the loan.

The same thing is happening when consumers purchase a mattress with financing from buy-now-pay-later firm Affirm AFRM 7.00%increase; green up pointing triangle, sign up for a student loan from Sallie Mae or borrow for their ATV from Octane Lending.

Private-credit funds held $350 billion of consumer-loan balances last year, compared with less than $200 billion in 2019, according to estimates from Jefferies. Those sums are a mixture of previously originated loans that lenders unload to private credit and increasingly so-called forward-flow arrangements, which involve agreements to buy future loans that haven’t been originated, similar to the Bilt and Harley pacts.

Much of this debt is personal loans that are often unsecured and that consumers can use for almost anything they want to buy.

Last year, about a quarter of newly originated personal loans were funded by private-credit forward-flow arrangements, up from about 6% the year before, according to Jefferies. The funding mechanism is also picking up for auto and private student loans.

“Private credit is looking to broaden its addressable market, which has historically been skewed towards the commercial side,” said Mike Taiano, vice president in the financial institutions group at Moody’s Ratings. “It’s a diversification play to some degree.”

Making this funding possible has been the steady stream of capital coming from investors into private-credit funds and insurers that need to be invested quickly.

Fintechs and other nonbanks are attracted to these deals because they lack large balance sheets and need to grow by originating more loans. They can remain “capital light” and less levered since they are unloading large chunks of debt, often at a premium.

Among the deals: TPG TPG 3.93%increase; green up pointing triangle this year agreed that it would buy around $2.4 billion of mostly personal loans from OneMain Financial, which lends to people who typically don’t have high credit scores. Late last year, KKR entered into a partnership with private student loan lender Sallie Mae that involves buying at least $2 billion of new loans each year for three years.

Blue Owl now has a dedicated asset-backed finance strategy after buying alternative asset manager Atalaya in late 2024. It entered into nearly $18 billion of forward-flow agreements last year across several lenders including PayPal, SoFi and LendingClub, according to data tracked by Jefferies.

Insurance companies, many of which are now owned by or affiliated with private investment funds, are also expanding. Affirm last year signed forward-flow agreements for roughly up to $9.75 billion from Liberty Mutual Investments, the investment firm of Liberty Mutual; PGIM, the asset-management business of Prudential Financial; and New York Life. The funding is being used for Affirm’s monthly installment loans.

Some private-credit executives say consumer debt can be less risky, pointing to the current relatively low delinquency rates on credit cards and other consumer loans. They also find comfort knowing the credit-score and other underwriting requirements around the loans that they buy from consumer lenders.

Others are bearish on consumers, especially those who don’t have mortgages. They point to inflation, wage stagnation and a slowing job market, all of which can reduce consumers’ ability to pay off debts.

The chase for consumer loans has also contributed to the recent headline concerns. A mortgage lender in the U.K., Market Financial Solutions, grew rapidly in recent years pledging its loans to private-credit firms. But it imploded this year, and firms have accused it of using loans as collateral several times.

Stone Ridge Asset Management, which has an interval fund with consumer and small-business loans from fintech lenders, has faced particularly high redemption requests.

A fintech addiction

Nonbank lenders have traditionally relied on warehouse financing, which functions like a line of credit, to make loans to consumers. Forward flow is an extra mechanism to fund loans. In an ideal scenario, the mix of funding sources gives the lender the ability to originate more or larger loans to consumers.

Octane Lending, which finances motorcycles, ATVs, RVs and other outdoor recreational equipment, entered into up to $700 million of agreements with New York Life, Equitable and a unit of MetLife. Octane expects north of $2 billion in new agreements from insurers to come together by the end of the second quarter.

The goal, said Chief Executive Officer Jason Guss, is to continue growing at a reasonable pace without getting overlevered itself. He also wants his firm to have capital on the sidelines in case of an economic slowdown.

“Quite a few fintechs are addicted to forward flow,” said Jordan Miller, CEO of fintech Yendo, which issues credit cards backed by collateral including people’s cars and homes and receives much of its funding from private credit.

It isn’t all upside, fintech and private-credit executives say. Providers of forward-flow arrangements can pull those deals easily—citing reasons ranging from increased delinquencies to macroeconomic conditions.

In the Bilt deal, the credit-card debt was moved to Fidem Financial, which acts as a balance sheet and gets funding for the program from Goldman, TD, Blue Owl and Stone Point. (Stone Point is also an owner of Fidem.)

Shortly before the Bilt deal was scheduled to be finalized in early February, Blue Owl raised concerns: It wouldn’t continue with the deal, it told parties involved in it, unless several things occurred.

Blue Owl wanted a guarantee that would involve its receiving the first tens of millions of dollars of profit generated by the credit-card program and wanted to dig more into the feasibility of Bilt’s forward-looking projections, according to people familiar with the matter.

Blue Owl blessed the deal on the eve before the card program was scheduled to transfer its balances away from Wells Fargo.

New research suggests that bonuses make employees feel more like a mere cog in a wheel.

Daman Investments and AllianzGI have signed an MoU to introduce risk-based, target-driven investment options to the UAE’s end-of-service savings program, expanding beyond capital-protected solutions. The move combines local market expertise with global investment capabilities to offer employees greater flexibility and support the evolution of workplace savings in the UAE.

2 min

Daman Investments (PSC), a leading asset manager in the UAE, has signed an MoU with Allianz Global Investors (“AllianzGI”), one of the world’s leading active asset managers, to collaborate on offering risk-based investment options as part of the MOHRE-approved Daman Investments End-of-Service Program.

This initiative will expand the existing program, which currently provides a capital-protected savings solution for end-of-service benefits, by introducing additional investment options designed to give employees greater choice in how their savings are managed.

The collaboration will combine Daman’s understanding of the UAE’s regulatory and workplace savings landscape with AllianzGI’s global expertise in long-term investment and retirement solutions. The two firms already share an established relationship, having previously launched the first onshore feeder fund in the UAE.

Daman selected AllianzGI as its preferred partner for this initiative based on its superior offering and strong track record in target driven investment solutions, which can be customized to local needs and can bring together public and private market exposure for long-term investment outcomes.

Commenting on the initiative, Shehab Gargash, Founder & Chairman of Daman Investments, said: “We are honored to be among the select MOHRE-approved service providers for End-of-Service benefits management in the UAE. Our collaboration with Allianz Global Investors reaffirms our commitment and belief in the strength and resilience of the UAE economy.”

Ahmed Khizer Khan, CEO of Daman Investments, added: “The UAE continues to make important progress in modernizing workplace savings frameworks. Through this collaboration, we aim to build on the foundation of our End-of-Service program by introducing additional investment options that support the evolving needs of employers and employees.”