China’s 40-Year Boom Is Over. What Comes Next?

The economic model that took the country from poverty to great-power status seems broken, and everywhere are signs of distress

10 min

10 min")

For decades, China powered its economy by investing in factories, skyscrapers and roads. The model sparked an extraordinary period of growth that lifted China out of poverty and turned it into a global giant whose export prowess washed across the globe.

Now the model is broken.

What worked when China was playing catch-up makes less sense now that the country is drowning in debt and running out of things to build. Parts of China are saddled with under-used bridges and airports. Millions of apartments are unoccupied. Returns on investment have sharply declined.

Signs of trouble extend beyond China’s dismal economic data to distant provinces, including Yunnan in the southwest, which recently said it would spend millions of dollars to build a new Covid-19 quarantine facility, nearly the size of three football fields, despite China having ended its “zero-Covid” policy months ago, and long after the world moved on from the pandemic.

Other localities are doing the same. With private investment weak and exports flagging, officials say they have little choice but to keep borrowing and building to stimulate their economies.

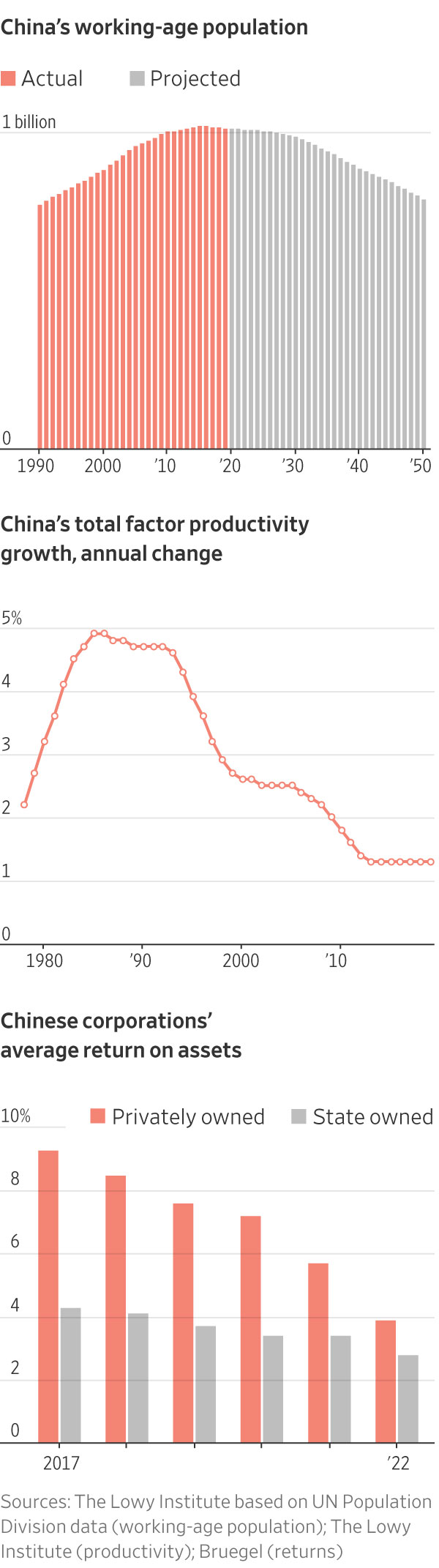

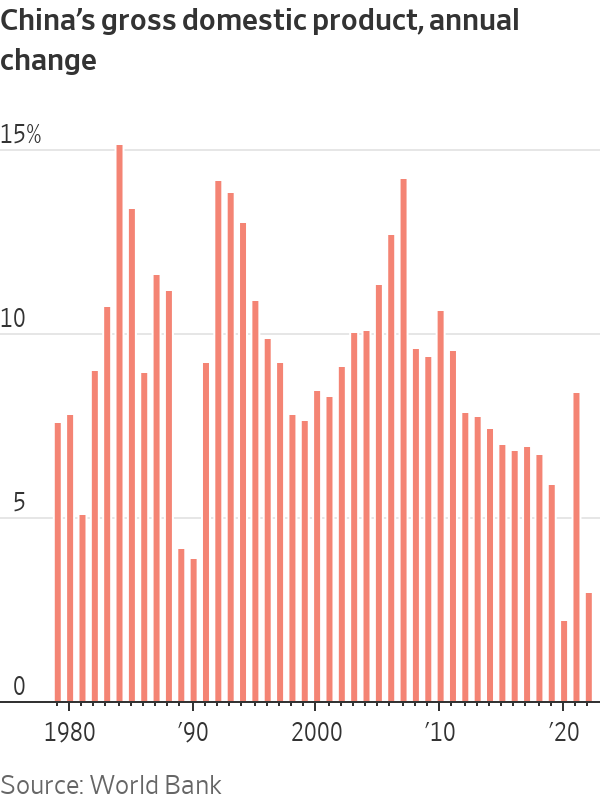

Economists now believe China is entering an era of much slower growth, made worse by unfavourable demographics and a widening divide with the U.S. and its allies, which is jeopardising foreign investment and trade. Rather than just a period of economic weakness, this could be the dimming of a long era.

“We’re witnessing a gearshift in what has been the most dramatic trajectory in economic history,” said Adam Tooze, a Columbia University history professor who specialises in economic crises.

What will the future look like? The International Monetary Fund puts China’s GDP growth at below 4% in the coming years, less than half of its tally for most of the past four decades. Capital Economics, a London-based research firm, figures China’s trend growth has slowed to 3% from 5% in 2019, and will fall to around 2% in 2030.

At those rates, China would fail to meet the objective set by President Xi Jinping in 2020 of doubling the economy’s size by 2035. That would make it harder for China to graduate from the ranks of middle-income emerging markets and could mean that China never overtakes the U.S. as the world’s largest economy, its longstanding ambition.

Many previous predictions of China’s economic undoing have missed the mark. China’s burgeoning electric-vehicle and renewable energy industries are reminders of its capacity to dominate markets. Tensions with the U.S. could galvanise China to accelerate innovations in technologies such as artificial intelligence and semiconductors, unlocking new avenues of growth. And Beijing still has levers to pull to stimulate growth if it chooses, such as by expanding fiscal spending.

Even so, economists widely believe that China has entered a more challenging period, in which previous methods of boosting growth yield diminishing returns.

Some of these strains were apparent before the pandemic. Beijing was able to keep growth ticking over by borrowing more and relying on a booming housing market, which in some years accounted for more than 25% of China’s gross domestic product.

The country’s initial success in containing Covid-19, and a surge in pandemic spending by U.S. consumers, further masked China’s economic troubles. The housing bubble has since popped, Western demand for Chinese products has ebbed and borrowing has reached unsustainable levels.

The outlook has darkened considerably in recent months. Manufacturing activity has contracted, exports have declined, and youth unemployment has reached record highs. One of the country’s largest surviving property developers, Country Garden Holdings, is on the cusp of a possible default as the overall economy slips into deflation.

Japan-like slowdown?

Without more aggressive stimulus from Beijing, and meaningful efforts to revive private sector risk-taking, some economists believe China’s slowdown could snowball into prolonged stagnation akin to what Japan has experienced since the 1990s, when the bursting of its real-estate bubble led to years of deflation and limited growth.

Unlike Japan, however, China would be entering such a period before reaching rich-world status, with per capita incomes far below more advanced economies. China’s national income per person reached about $12,850 last year, below the current threshold of $13,845 that the World Bank classifies as the minimum for a “high-income” country. Japan’s per capita national income in 2022 was about $42,440, and the U.S.’s was about $76,400.

A weaker Chinese economy could also undermine popular support for Xi, the most powerful Chinese leader in recent decades, though there is no current indication of organized opposition. Some U.S. analysts worry Beijing could respond to slower growth by becoming more repressive at home and more aggressive abroad, raising the risks of conflict, including potentially over the self-governing island of Taiwan.

At an Aug. 10 political fundraiser, President Biden called China’s economic problems a “ticking time bomb” which could spur its leaders to “do bad things.”

Beijing fired back with a commentary by its official Xinhua News Agency, saying Biden “intends to take smearing China as part of his ‘grand strategy’ to shoot America’s economic troubles.” The commentary also described China’s economic recovery this year as robust, despite some challenges.

Chinese officials have taken some modest steps to revive growth, including cutting interest rates, and have pledged to do more if conditions worsen. The State Council Information Office, which handles media inquiries for China’s leadership, didn’t respond to questions.

“Certain Western politicians and media have exaggerated and hyped up the current difficulties in China’s post-Covid economic recovery,” a Foreign Ministry spokesman said on Aug. 16. “Facts will prove them wrong.”

‘Chinese Century’

The transition marks a stunning change. China consistently defied economic cycles in the four decades since Deng Xiaoping started an era of “reform and opening” in 1978, embracing market forces and opening China to the West, in particular through international trade and investment.

During that period, China increased per capita income 25-fold and lifted more than 800 million Chinese people out of poverty, according to the World Bank—more than 70% of the total poverty reduction in the world. China evolved from a nation racked by famine into the world’s second-largest economy, and America’s greatest competitor for leadership.

Academics were so enthralled by China’s rise that some referred to a “Chinese Century,” with China dominating the world economy and politics, similar to how the 20th century was known as the “American Century.”

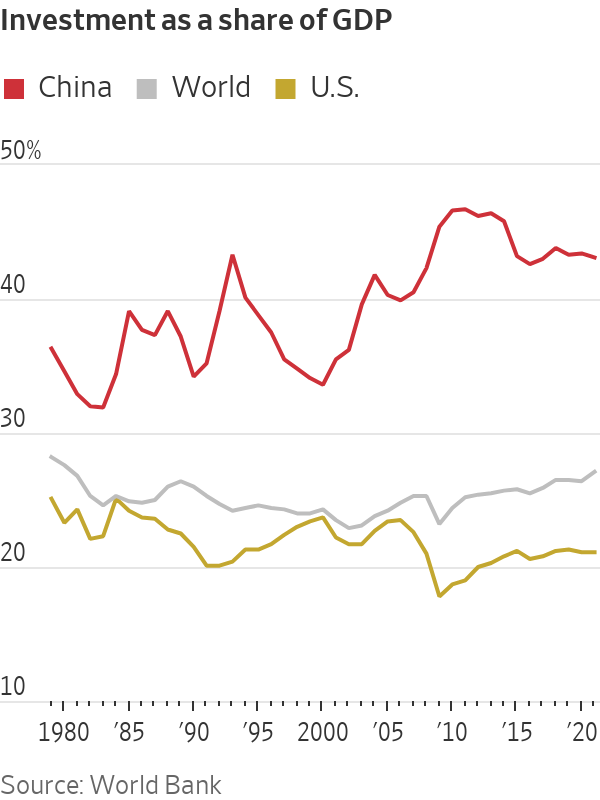

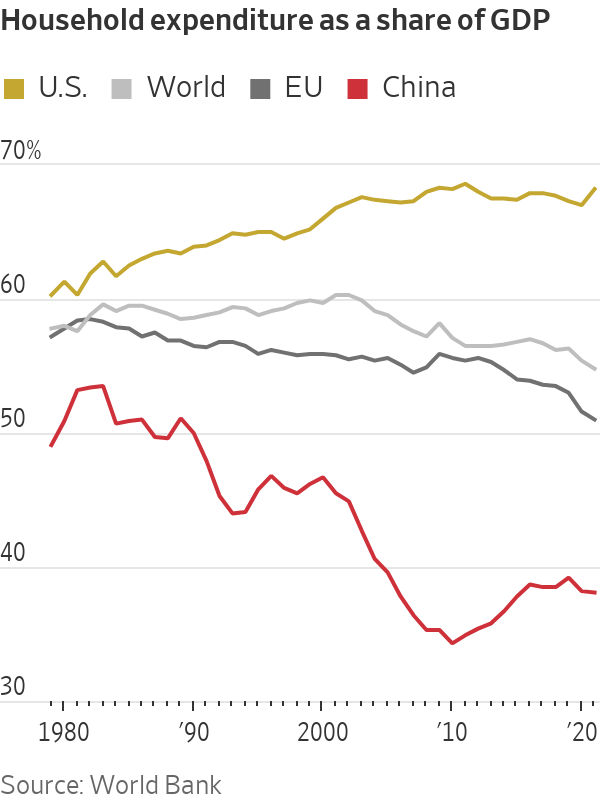

China’s boom was underpinned by unusually high levels of domestic investment in infrastructure and other hard assets, which accounted for about 44% of GDP each year on average between 2008 and 2021. That compared with a global average of 25% and around 20% in the U.S., according to World Bank data.

Such heavy spending was made possible in part by a system of “financial repression” in which state banks set deposit rates low, which meant they could raise funds inexpensively and fund building projects. China added tens of thousands of miles of highways, hundreds of airports, and the world’s largest network of high-speed trains.

Over time, however, evidence of overbuilding became apparent.

About one-fifth of apartments in urban China, or at least 130 million units, were estimated to be unoccupied in 2018, the latest data available, according to a study by China’s Southwestern University of Finance and Economics.

A high-speed rail station in Danzhou, a city in China’s southern province of Hainan, cost $5.5 million to build but was never put into use because passenger demand was so low, according to Chinese media reports. The Hainan government said keeping the station open would incur “massive losses.” Efforts to reach the local government were unsuccessful.

Guizhou, one of the poorest provinces in the country with GDP per capita of less than $7,200 last year, boasts more than 1,700 bridges and 11 airports, more than the total number of airports in China’s top four cities. The province had an estimated $388 billion in outstanding debt at the end of 2022, and in April had to ask for aid from the central government to shore up its finances.

Kenneth Rogoff, a professor of economics at Harvard University, said China’s economic ascent draws parallels to what many other Asian economies went through during their periods of rapid urbanisation, as well as what European countries such as Germany experienced after World War II, when major investments in infrastructure boosted growth.

At the same time, decades of overbuilding in China resembles Japan’s infrastructure construction boom in the late 1980s and 1990s, which led to over investment.

“The leading point is they are running into diminishing returns in building stuff,” he said, “There are limits to how far you can go with it.”

With so many needs met, economists estimate China now has to invest about $9 to produce each dollar of GDP growth, up from less than $5 a decade ago, and a little over $3 in the 1990s.

Returns on assets by private firms have declined to 3.9% from 9.3% five years ago, according to Bert Hofman, head of the National University of Singapore’s East Asian Institute. State companies’ returns have retreated to 2.8% from 4.3%.

China’s labor force, meanwhile, is shrinking, and productivity growth is slowing. From the 1980s to the early 2000s, productivity gains contributed about a third of China’s GDP growth, Hofman’s analysis shows. That ratio has declined to less than one sixth in the past decade.

Deepening debt

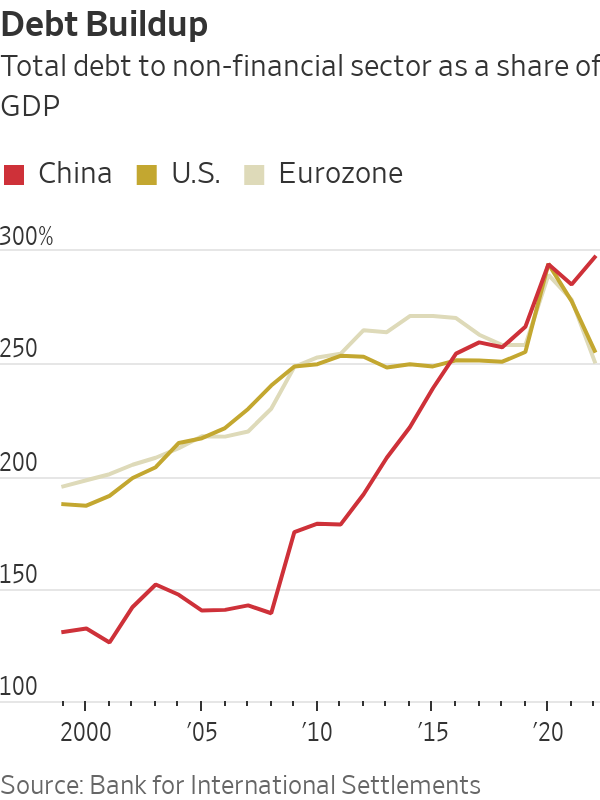

The solution for many parts of the country has been to keep borrowing and building. Total debt, including that held by various levels of government and state-owned companies, climbed to nearly 300% of China’s GDP as of 2022, surpassing U.S. levels and up from less than 200% in 2012, according to Bank for International Settlements data.

Much of the debt was incurred by cities. Limited by Beijing in their ability to borrow directly to fund projects, they turned to off-balance sheet financing vehicles whose debts are expected to reach more than $9 trillion this year, according to the IMF.

Rhodium Group, a New York-based economic research firm, estimates that only about 20% of financing firms used by local governments to fund projects have enough cash reserves to meet their short-term debt obligations, including bonds owned by domestic and foreign investors.

In Yunnan, location of the giant quarantine centre, heavy infrastructure spending lifted growth for years. Officials spent hundreds of billions of dollars including on Asia’s tallest suspension bridge, more than 6,000 miles of expressways and more airports than many other regions in China.

The projects boosted tourism and helped expand trade of Yunnan products including tobacco, machinery and metals. From 2015 to 2020, Yunnan was one of the fastest-growing regions in China. Growth has weakened in the past few years. The slumping property market has hit local finances hard, as revenue from land sales dries up.

Yunnan’s debt-to-revenue ratio climbed to 151% in 2021, breaching a 150% level designated as alarming by the IMF, and up from 108% in 2019, according to Lianhe Ratings, a Chinese rating agency. Fitch Ratings earlier this year said financing firms used by the province to fund infrastructure construction were risky because of the size of their borrowings and the government’s strained finances.

Yet Yunnan has continued to hatch big schemes. In early 2020, the Yunnan government said it planned to spend nearly $500 billion on hundreds of infrastructure projects, including a more than $15 billion program aimed at diverting water from parts of the Yangtze River to the dry centre of the province.

A February plan issued by Wenshan, a city in Yunnan, listed the “permanent” quarantine centre as one of several measures aimed at promoting economic stability. Once the government officially put out a bid in June for its construction, local residents questioned the use of funds.

“It’s such a waste of money,” wrote one user of Weibo, a popular microblogging platform in China.

A Yunnan official confirmed the plan to build the quarantine facility, which is expected to be completed at the end of this year, but declined to comment further.

Tighter control

In Beijing’s corridors of power, senior officials have recognised that the growth model of past decades has reached its limits. In a blunt speech to a new generation of party leaders last year, Xi took aim at officials for relying on borrowing for construction to expand economic activities.

“Some people believe that development means investing in projects and scaling up investments,” he said, while warning, “you can’t walk the old path with new shoes.” Xi and his team so far have done little to shift away from the country’s old growth model.

The most obvious solution, economists say, would be for China to shift toward promoting consumer spending and service industries, which would help create a more balanced economy that more resembles those of the U.S. and Western Europe. Household consumption makes up only about 38% of GDP in China, relatively unchanged in recent years, compared with around 68% in the U.S., according to the World Bank.

Changing that would require China’s government to undertake measures aimed at encouraging people to spend more and save less. That could include expanding China’s relatively meager social safety net with greater health and unemployment benefits.

Xi and some of his lieutenants remain suspicious of U.S.-style consumption, which they see as wasteful at a time when China’s focus should be on bolstering its industrial capabilities and girding for potential conflict with the West, people with knowledge of Beijing’s decision-making say.

The leadership also worries that empowering individuals to make more decisions over how they spend their money could undermine state authority, without generating the kind of growth Beijing desires.

A plan announced in late July to promote consumption was criticised by economists both in and outside China for lacking details. It suggested promoting sports and cultural events, and pushed for building more convenience stores in rural areas.

Instead, guided by a desire to strengthen political control, Xi’s leadership has doubled down on state intervention to make China an even bigger industrial power, strong in government-favoured industries such as semiconductors, EVs and AI.

While foreign experts don’t doubt China can make headway in these areas, they alone aren’t enough to lift up the entire economy or create enough jobs for the millions of college graduates entering the workforce, economists say.

Beijing has spent billions of dollars to try to build up the country’s semiconductor industry and reduce its dependence on the West. That has resulted in expanded production of less-sophisticated chips, but not the advanced semiconductors produced by companies such as Taiwan Semiconductor Manufacturing. Among the projects that failed were two high-profile foundries that received hundreds of millions of dollars in government support.

Last week, just as Beijing released a barrage of disappointing economic data, the party’s premier journal, Qiushi, published a speech made by Xi six months earlier to senior officials, in which the leader emphasised the importance of focusing on long-term goals instead of pursuing Western-style material wealth. “We must maintain historic patience and insist on making steady, step-by-step progress,” Xi said in the speech.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

To mark its 30th anniversary, Parmigiani Fleurier has unveiled the Carillon Tourbillon, a limited-edition timepiece of just five pieces that combines a tourbillon with a four-note chiming mechanism; inspired by a 19th-century pocket watch restored by the Maison.

Salesforce reported record first-quarter fiscal results, with revenue rising 13% year-on-year to $11.1 billion and strong growth across its AI business. The company’s Agentforce and Data 360 annual recurring revenue reached nearly $3.4 billion, prompting Salesforce to raise its full-year revenue outlook as demand for AI-powered enterprise solutions continues to accelerate.

Saudia is set to receive 12 new aircraft throughout 2026 as part of its fleet expansion strategy aimed at boosting capacity, improving efficiency, and strengthening global connectivity. The move supports the airline’s long-term growth plans and Saudi Vision 2030, with Saudia’s fleet expected to reach 161 aircraft by the end of the year.

OMODA & JAECOO is showcasing how AI-powered humanoid robots and autonomous parking technologies could support the UAE’s smart city ambitions. Through its AiMOGA robotics platform and VPD self-parking system, the company is exploring future applications across airports, malls, public services, and urban mobility ecosystems.

3 min

As the UAE continues accelerating its transformation into one of the world’s leading smart city ecosystems, OMODA & JAECOO is highlighting the growing role humanoid robots and AI-powered smart mobility technologies could play in shaping future urban experiences through its AiMOGA intelligent robotics platform and advanced VPD (Valet Parking Driver) technology.

Developed jointly with the AiMOGA team, the company’s humanoid and intelligent service robots are already being deployed across real-world public service environments globally, showcasing how artificial intelligence, robotics, and smart mobility technologies are increasingly converging beyond traditional automotive applications.

The latest demonstrations include the deployment of AiMOGA’s intelligent traffic robot “Wuyou” for real-world street patrol and traffic guidance duties, as well as humanoid robots supporting international sporting events through multilingual interaction, public assistance, and venue guidance services.

OMODA & JAECOO has also demonstrated its advanced VPD (Valet Parking Driver) technology during the Chery International Business Summit in China, showcasing how AI-powered driverless self-parking systems could support future smart mobility ecosystems. The technology enables vehicles to autonomously locate parking spaces, self-park, and return to drivers through intelligent summon functions — offering future convenience for busy urban environments, shopping destinations, hotels, airports, and smart city infrastructure.

OMODA & JAECOO says these technologies represent the next phase of intelligent mobility ecosystems — where AI-powered systems move beyond vehicles and become integrated into future smart city infrastructure.

The initiative aligns closely with the UAE’s broader ambitions around artificial intelligence, smart mobility, and intelligent urban development. Potential future applications could include AI-powered assistance at airports, malls, tourism destinations, public transportation hubs, and major events.

The AiMOGA robots are powered by technologies derived from intelligent automotive systems, including autonomous navigation, environmental perception, multimodal sensing, AI interaction systems, and cloud-connected data platforms.

Humanoid robot “Mornine” is capable of multilingual interaction in 11 languages and can assist with hosting, customer guidance, and public engagement, while quadruped robot “Argos” has demonstrated autonomous navigation and assistance capabilities across complex public environments.

OMODA & JAECOO says the project reflects its wider “Human-Vehicle-Road-Cloud” ecosystem vision, where intelligent technologies used in advanced vehicles can also support broader smart living and public service scenarios.

AiMOGA robots are currently operating in more than 30 countries and regions worldwide and have already been deployed across more than 100 real-world scenarios including showrooms, exhibitions, urban services, and public interaction environments.

The robotics initiative comes as OMODA & JAECOO continues expanding its global footprint following the company’s milestone of surpassing 1 million cumulative global vehicle sales within just three years. In the UAE, the brand has also crossed 5,000 vehicle sales while rapidly strengthening its retail and aftersales presence across the country.

OMODA & JAECOO currently operates multiple showrooms across Dubai, Abu Dhabi, Sharjah, Ras Al Khaimah and Fujairah, offering an expanding line-up of intelligent and new energy vehicles including the OMODA C5, OMODA C7, JAECOO J7 SHS (Super Hybrid System), and the flagship JAECOO J8 SHS. The company says advanced intelligent technologies including VPD will gradually become available in select future models.

Commenting on the company’s future intelligent ecosystem vision, Shawn Xu, CEO of OMODA & JAECOO Automobile International, said: “Artificial intelligence and robotics are becoming an increasingly important part of future mobility ecosystems. Through AiMOGA and our intelligent driving technologies, we are exploring how smart systems developed for vehicles can also support future urban services, public interaction, and smart city experiences. The UAE is one of the world’s most forward-looking markets in AI and smart mobility, making it an important market for our future ecosystem vision.”

The company believes future smart cities will increasingly rely on AI-powered collaboration between humans, intelligent vehicles, and robotics systems to improve efficiency, convenience, and user experiences.

As Dubai and Abu Dhabi continue investing heavily in AI and future urban technologies, humanoid robotics and intelligent autonomous mobility technologies could emerge as major pillars of future smart city ecosystems across the region.

The sports-car maker delivered 279,449 cars last year, down from 310,718 in 2024.

New research suggests that bonuses make employees feel more like a mere cog in a wheel.

Inditex, the owner of Zara, reported stronger sales growth in May, with revenue rising 11.5% despite higher costs and economic uncertainty linked to tensions in the Middle East. The fashion giant said its diversified supply chain has helped maintain operations, while all of its nearly 480 stores across the region remain open.

2 min

Spanish fashion giant said sales growth picked up last month despite a difficult market environment for apparel companies as the war in the Middle East pushes up raw-material and shipping costs.

The group, home to high-street labels like Zara, Massimo Dutti and Bershka, said Wednesday that sales rose 11.5% on a constant-currency basis in May compared with the prior-year period. That marked an acceleration from the sales increase of just shy of 9% it booked for its first quarter through April 30 to a total of 8.75 billion euros ($10.18 billion).

“We are very pleased with the strong evolution of sales,” finance chief Andres Sanchez Iglesias said during a call.

May’s performance confirms the group’s ability to step up market-share gains at a time when European demand has become more challenged, analysts at Jefferies wrote in a note. “Today investors were looking for reassurance that the group is well set to navigate through the toughening global backdrop which has emerged over the past three months,” they said.

Apparel retailers face the impact of higher costs caused by the war in the Persian Gulf, along with worsened consumer sentiment. Companies are also grappling with the volatility of oil prices, a raw material used in the fashion industry for the production of clothing in synthetic fibers such as polyester and as a lubricant for manufacturing machinery.

“We have been able to rapidly adapt our supply chain to ensure uninterrupted product flow to our stores globally,” Sanchez said. The diversification of Inditex’s operations and supply chains enabled the group to adapt its transportation methods and choose between air, sea, or land transport, depending on the most viable option, he said.

The stock was up 5.4% in European morning trading.

The company said that all of its roughly 480 stores in the Middle East region, which are operated under a franchise, remain open and that it hasn’t seen any major impact from energy-driven price inflation.

For the year through January 2027, Inditex said it continues to anticipate a broadly stable gross margin compared with a year earlier.

Parts for iPhones to cost more owing to surging demand from AI companies.

Following the successful launch of its Palais Collection, MAISON de SABRÉ has unveiled a new modular handbag system offering more than 720 styling combinations.

AWS has launched the Agentic Shopping Assistant, a new AI-powered solution that enables retailers to build their own conversational shopping experiences in as little as 60 days. Based on technology developed for Amazon’s AI shopping tools, the platform helps brands deliver personalized product recommendations, strengthen customer engagement, and maintain direct relationships with shoppers in the age of AI-driven commerce.

3 min

As Amazon has continually iterated to create a leading AI shopping assistant, it gave us valuable insights about what capabilities, tools, and features matter most to the over 300 million customer who used it last year. Amazon’s AI shopping assistant drove nearly $12 billion in incremental sales for Amazon last year alone. Last week, Amazon announced Alexa for Shopping, an even more capable next iteration bringing together Rufus and Alexa+.

Today, AWS announces a new AI retail solution that brings learnings and expertise gained from building Alexa for Shopping for the first time to retailers outside Amazon, packaged into the Agentic Shopping Assistant on AWS.

AI-powered shopping assistance, built for the retail industry

The solution provides a technical foundation with architecture guidance, starter code, and support from AWS experts and system integrator partners, allowing them to launch their own conversational shopping experiences in weeks—rather than the years it would take starting from scratch. It is tailored to each retailer’s specific catalog, customer base, and shopping environment. Each deployment is customized to match the retailer’s brand voice and domain expertise.

Why retailers need their own AI shopping presence

Chat agents can surface recommendations based on shoppers’ needs, making it easier for customers to navigate retailers’ catalogs.

As AI agents become the primary interface for shopping decisions, retailers face a critical choice: build their own AI presence or risk becoming dependent on general-purpose answer engines that don’t serve their brand or customers. The business case is compelling: conversational shopping sessions convert at 3.5 times the rate of traditional keyword search.

Retailers already possess deep vertical knowledge about their products, customers, and categories that no general-purpose AI can match. A specialty retailer knows its offerings better than any intermediary. Restaurant chains understand their menus and customer preferences in ways no platform can replicate, and no one knows their products better than consumer packaged goods (CPG) brands. The Agentic Shopping Assistant on AWS gives retailers the proven technology foundation to act on that knowledge while maintaining direct customer relationships.

How Kate Spade built an AI shopping assistant with AWS

Kate Spade used this solution to create its own conversational shopping experience. On April 13, Tapestry launched the Kate Spade AI Gift Concierge, the first production-ready retail AI assistant built with Amazon Bedrock AgentCore, purpose-built for the moment in shopping when emotions run high but confidence runs low: gift buying.

Recognizing that 53% of shoppers report stress during gift purchases, the agent engages shoppers in natural dialogue about occasion, recipient, and style to translate uncertain intent into curated, confident product recommendations. The experience was grounded in how people shop for gifts—informed by real shopper behavior and insights drawn from the questions customers asked Amazon’s Alexa for Shopping and the answers that drove successful outcomes. The result is an interaction model that feels less like search and more like talking to someone who knows the brand and knows how to give a great gift.

Built on the Haiku 4.5 model with Amazon Bedrock providing observability, authentication, and evaluations, the team moved directly into production and completed roughly 2.5 months of rigorous testing before becoming customer-facing. As Yang Lu, chief information and digital officer at Tapestry, shared at launch: “We are excited about the possibilities agentic commerce can bring to our customers. AWS brought the recipe, but together we built the customization our consumers needed.”

What’s included: AWS services, architecture, and deployment timeline

An AI-powered style advisor recommends products through natural conversation—the kind of experience validated by more than 300 million Alexa for Shopping customers.

The Agentic Shopping Assistant on AWS is built on AWS services such as Amazon Bedrock, AgentCore, and OpenSearch, validated through billions of real shopping interactions on Amazon.com. Amazon serves as “Customer Zero” for AWS, meaning every component has been tested in one of the world’s most demanding retail environments.

However, each brand’s deployment is customized to match their specific catalog, customer base, shopping environment, and brand voice. Retailers get the Retailers get a technical foundation refined through years of powering AI shopping on Amazon.com, while keeping their competitive advantages from proprietary customer insights, domain knowledge, and brand relationships. Instead of launching and operationalizing from scratch, retailers can deploy this proven solution in roughly 60 days with hands-on guidance from the AWS Generative AI Innovation Center team.

How retailers can get started

Retailers can’t afford to wait to build conversational shopping capabilities as customer expectations shift. The Agentic Shopping Assistant on AWS provides the proven foundation, and retailers bring the domain expertise that makes their shopping experience unique.

New research suggests that bonuses make employees feel more like a mere cog in a wheel.

Two coming 2027 models – the first of the “Neue Klasse” cars coming to the U.S. early next year – have been revealed.

To mark its 30th anniversary, Parmigiani Fleurier has unveiled the Carillon Tourbillon, a limited-edition timepiece of just five pieces that combines a tourbillon with a four-note chiming mechanism; inspired by a 19th-century pocket watch restored by the Maison.

7 min

THE MAISON’S SOUND SIGNATURE

For its 30th anniversary, Parmigiani Fleurier unveils a creation that does more than mark a milestone. It reveals an essential part of its history, its culture, and its singular way of conceiving haute horlogerie.

With the Carillon Tourbillon, the Maison opens one of its most intimate realms: that of sounding time. A place where restoration, mechanical memory, and attentive dialogue with materials and contemporary invention converge.

This atelier piece, limited to five examples, is born of a conviction that has accompanied Parmigiani Fleurier since its origins: before creating, one must understand. Understand historic objects, their architecture, their energy, their inner logic. Understand what time has deposited within them, then transform that knowledge into a contemporary expression.

Inspired by an early nineteenth-century Perrin Frères pocket watch, from the Sandoz Collection, restored in the ateliers of Parmigiani Fleurier in 2000, the Carillon Tourbillon does not reproduce a form from the past. It carries forward an intelligence: that of sound, gesture, balance and horological construction.

Entirely conceived, developed, constructed, assembled and finished within the Maison, it bears the vision of Michel Parmigiani and the savoir-faire of the watchmakers, constructors, artisans and finishers of the Manufacture.

The Carillon Tourbillon is more than an anniversary piece. It is a way for Parmigiani Fleurier to reveal to the world what lies at the founding of its haute horlogerie: a creation born of restoration, nourished by transmission, constructed from within, and guided by an intimate pursuit of mechanical and aesthetic harmony.

PERRIN FRÈRES : FROM RESTORATION TO RESONANCE

At the origin of the Carillon Tourbillon lies a seminal piece: a pocket watch signed Perrin Frères, made in Neuchâtel in the early nineteenth century, from the Sandoz Collection, and restored in the workshops of Parmigiani Fleurier in 2000.

This historic masterpiece was not approached as a model to reproduce, but as a living object to understand. It carried within it a knowledge of sound, energy, balance and mechanical architecture, extending even to the serpentine presence of its gongs, an immediately recognisable formal signature that the Carillon Tourbillon reinterprets within a contemporary construction.

This lineage illuminates one of Parmigiani Fleurier’s deepest convictions: history is never a static archive. It is a source of creation.

UNDERSTANDING AS THE FIRST ACT OF CREATION

Understanding before drawing. Restoring before inventing. Listening to the inner logic of objects before proposing a new expression.

A restorer before becoming a creator, Michel Parmigiani shaped his perspective through close contact with historic timepieces, automata, clocks and chiming mechanisms.

From this practice emerged a singular way of thinking about watchmaking from within: through the hand, through memory, through the mechanical intelligence of objects.

The Carillon Tourbillon emerges directly from this lineage: that of a Maison that learned to create by first learning to understand. It expresses a vision of haute horlogerie in which complexity is never an effect, but a necessary architecture.

Michel Parmigiani remained closely involved throughout its development, working alongside the watchmakers and constructors, guiding, refining and transmitting a vision of mechanics as an architecture that is legible, enduring and profoundly mastered.

This piece does not merely bear the signature of the Maison. It is the expression of its most intimate culture.

FROM TOWER TO WRIST: THE INTIMACY OF SOUNDING TIME

From medieval bell towers to the great chiming watches, the carillon belongs to a singular history: that of time made audible.

Once, it gave rhythm to the life of the city. Reimagined within the intimate space of a timepiece, it becomes a personal experience. The tradition of the carillon reminds us that sound is never a mere effect: it carries memory, gesture, continuity.

In the Carillon Tourbillon, this culture of sound leaves the public realm to inhabit the space of the wrist. Time no longer imposes itself. It reveals itself, on demand, through the vibration of a miniature architecture.

The Carillon Tourbillon is unmistakably a Parmigiani Fleurier creation of today. Its language neither looks to the past with nostalgia nor seeks demonstrative effect. It expresses its modernity through the clarity of its construction and through its relationship with volume, transparency and light.

The redesigned white gold case, the vertical gadroons inspired by the classical columns so dear to Michel Parmigiani, the glass box sapphire crystal, the visible hammers on the dial side and the hand-hammered Morning Blue dial; the aesthetic signature of the thirtieth anniversary places the piece firmly within a contemporary expression. One of its most recognisable gestures lies in its four serpentine gongs. Directly inspired by the Perrin Frères pocket watch restored by Parmigiani Fleurier, their long undulating curves embrace the architecture of the Carillon Tourbillon, giving it its visual identity, structuring space and marking the reading of the hours.

Here, acoustics become form.

Between silver and azure, the Morning Blue dial enters into dialogue with this architecture without ever dominating it. Its deliberately restrained proportions free the space required for the presence of the hammers and the unfolding of the gongs.

Here, mechanics do not add themselves to form: they structure it.

Yet within this contemporary presence remains a profound memory: that of gesture, of sound, of restored objects, and of the watchmakers who conceived of time as a living material.

The Carillon Tourbillon embodies a rare tension: a contemporary creation, shaped by the intelligence of the past

VIRTUOSITY HELD IN RESERVE

The piece also expresses a distinctly Parmigiani Fleurier philosophy of visibility.

The tourbillon and the power-reserve indicator are positioned on the reverse of the watch, where the movement opens fully to the eye. On the dial side, the reading remains clear, balanced, almost silent.

Virtuosity does not seek immediate effect. It reveals itself through depth, through observation, through use, through time spent with the object.

This restraint does not diminish the chiming complication. It stages it with precision.

On the dial side, the hammers are visible in both their function and in their mechanical choreography. They reveal the very instant in which time is about to become sound.

Around them, the serpentine gongs envelop the piece like memory turned into architecture. Their presence introduces an almost musical tension between silence and release, between anticipation and vibration.

A CALIBRE TUNED FOR RESONANCE

The calibre is a true demonstration of craftsmanship, composed of 456 components meticulously assembled by hand. Its construction is based on a highly sophisticated mechanical architecture built around two superimposed barrels, ensuring the transmission of power through the gear train and guaranteeing an exceptional 12-day power reserve, a rarity in a timepiece incorporating a chiming complication.

The third barrel, dedicated to the striking mechanism, is automatically rewound when the striking slide is activated, and only when the minute repeater is engaged.

The construction of the calibre has also been conceived to make the mechanics fully legible in motion. The components related to the striking mechanism are positioned on the case back side, offering the eye a view of the mechanism unfolding at the very moment when it transforms time into sound. The open architecture reveals the inner logic of the complication: the circulation of energy, the cadence of the hammers, the vibration of the gongs.

The mechanism incorporates a regulating flywheel, ensuring a constant flow of energy and a perfectly regular cadence. This essential component provides a fluid chime, without acceleration or slowing, for an acoustic experience mastered from the first strike to the last.

In the Carillon Tourbillon, the movement is therefore not only a motor. It becomes an instrument. It measures, it stores, it releases, it regulates, it gives sound to time.

A MELODY IN FOUR NOTES

The four gongs compose a complete and nuanced chime: one low-pitched gong for the hours one high-pitched gong for the minutes two additional gongs, each with its own note, for the quarters

Together, they create a four-note melody – distinctive, harmonious and immediately recognisable.

The striking mechanism is equipped with an integrated regulating flywheel, ensuring a constant flow of energy and a perfectly regular cadence.

This essential component guarantees a fluid chime, free from acceleration or slowing, for an acoustic experience that remains controlled from the first strike to the last.

A CASE BUILT FOR RESONANCE

The white gold case extends the lineage of the Armoriale, with its vertical gadroons inspired by the classical columns so dear to Michel Parmigiani.

This choice continues an acoustic sensibility deeply rooted in his approach to haute horlogerie: in a chiming timepiece, the case does more than house the movement; it contributes to the transmission of sound — its density, clarity and resonance.

White gold offers here a controlled resonance, in harmony with the spirit of the Carillon Tourbillon.

Reimagining this architecture to accommodate a dial, a tourbillon and a carillon striking mechanism transforms the aesthetic language of the Armoriale into a complete horological construction.

Integrated into the case band, the striking slide calls for a gesture that is simple, direct and almost ceremonial.

MADE FOR TRANSMISSION

Produced in only five examples, the Carillon Tourbillon belongs to a different temporality from that of novelty.

Its rarity is not a launch statement. It is the natural consequence of a creation that demands time, hands, attentive listening and an almost confidential mastery.

This piece is conceived for transmission, for collections that look beyond the instant, for those who recognise in a horological creation not only an achievement but a culture.

With the Carillon Tourbillon, Parmigiani Fleurier does more than celebrate thirty years of existence. The Maison reveals one of the deeper sources of its creative philosophy: a vision of haute horlogerie born of restoration, nourished by transmission, constructed from within, and capable of transforming complication into culture.

Thirty years after its founding, Parmigiani Fleurier’s voice in time continues to resonate.

THE SERPENTINE SIGNATURE

The four serpentine gongs constitute one of the most recognisable signatures of the Carillon Tourbillon. Visible beneath the glass box sapphire crystal, they trace long undulating curves that envelop the piece and give the acoustic architecture its singular presence.

This form derives directly from an element observed on the Perrin Frères pocket watch restored by Parmigiani Fleurier. Reinterpreted within a contemporary creation, it becomes more than a historical recollection: it becomes a principle of construction, at once acoustic, aesthetic and spatial.

The serpentine curves accompany the reading of the hours and inscribe sound within the very form of the watch. They lend the chiming mechanism a fluid, almost organic presence, perceptible even in silence.

Here, the gong is not merely an acoustic component. It becomes sign, structure and memory.

MAKING RESONANCE VISIBLE

The movement, too, becomes a field of expression.

Its components are adorned with the mezzo vibrato decoration, a language previously explored by Parmigiani Fleurier on the dial of the Armoriale, the Maison’s emblematic Objet d’Art and now transposed into the very heart of the movement.

Executed entirely by hand by the engravers, surface after surface, this slow and demanding work brings the material to life.

Here, the gesture leaves the surface of the dial to enter the mechanical architecture itself. It acts as a visual resonance of the chiming mechanism: what the carillon makes heard, the mezzo vibrato makes visible.

MORNING BLUE, HAMMERED INTO LIGHT

The Morning Blue dial, crafted in hand-hammered white gold, extends this dialogue between material, light and vibration.

Between silver and azure, the Morning Blue tone engages with the metal without ever concealing it.

This hammered texture forms one of the defining aesthetic signatures of Parmigiani Fleurier’s thirtieth anniversary, in continuity with the Toric Anniversary creations.

It expresses a shared idea of the hand: a living gesture, never standardised, through which each surface carries its own subtle variation.

The sports-car maker delivered 279,449 cars last year, down from 310,718 in 2024.

Many of the most-important events have slipped from our collective memories. But their impacts live on.

Salesforce reported record first-quarter fiscal results, with revenue rising 13% year-on-year to $11.1 billion and strong growth across its AI business. The company’s Agentforce and Data 360 annual recurring revenue reached nearly $3.4 billion, prompting Salesforce to raise its full-year revenue outlook as demand for AI-powered enterprise solutions continues to accelerate.

3 minSalesforce (NYSE: CRM), the world’s #1 AI CRM, today announced results for its first quarter fiscal 2027 ended April 30, 2026.

First Quarter Financial Highlights

- Current remaining performance obligation of $33.6 billion, up 14% year-over-year (“Y/Y”) and 13% in constant currency (“CC”)

- Remaining performance obligation of $67.9 billion, up 11% Y/Y

- First quarter subscription & support revenue of $10.6 billion, up 14% Y/Y and 12% in CC, including $428 million Informatica contribution

- First quarter revenue of $11.1 billion, up 13% Y/Y and 12% in CC, including $444 million Informatica contribution

- First quarter GAAP operating margin of 21.1% and non-GAAP operating margin of 34.8%

- First quarter GAAP diluted net income per share of $2.42, up 52% Y/Y and non-GAAP diluted net income per share of $3.88, up 50% Y/Y

- First quarter operating cash flow of $6.7 billion, up 3% Y/Y, and free cash flow of $6.6 billion, up 4% Y/Y

- Returned $27.5 billion to shareholders, including $27.1 billion in share repurchases and $365 million in dividends

- Entered into $25 billion accelerated share repurchase (“ASR”), with upfront share delivery of 103 million shares representing approximately 80% of total shares expected to be repurchased, with final settlement expected in Q3 FY27

“This was an outstanding quarter for Salesforce — record revenue, record deals, and cash flow,” said Marc Benioff, Chair and CEO, Salesforce. “Agentic AI is the biggest growth opportunity for our customers, and for Salesforce. We’re the #1 Agentic CRM, with Agentforce now powering every Customer 360 application and helping tens of thousands of businesses across every industry transform into Agentic Enterprises. With more than $1 billion in Agentforce ARR, $3.4 billion in combined AI and data ARR, and 3.8 billion Agentic Work Units delivered for our customers, Salesforce has never been more essential.”

“We remain confident in delivering organic revenue acceleration in the second half of FY27, driven by growth in Sales, Service, Slack, Agentforce, and Data 360,” said Robin Washington, President and Chief Financial and Operating Officer, Salesforce. “We are executing against our profitable growth framework and remain on track to deliver on our FY30 targets while maximizing shareholder value.”

Salesforce Company Highlights

- Agentforce and Data 360 annual recurring revenue (“ARR”) reaches nearly $3.4 billion, up over 200% Y/Y, including $1.1 billion Informatica Cloud ARR and $1.2 billion Agentforce ARR, up 205% Y/Y

- 3.8 billion Agentic Work Units (“AWUs”) delivered to date across Agentforce and Slack, growing 111% quarter-over-quarter (“Q/Q”)

- Bookings from Agentforce One Edition and Agentforce for Apps, premium SKUs anchored in Sales and Service including the value from Agentic capabilities, grew nearly 60% Y/Y

- Processed more than 28.6 trillion tokens to date, up 152% Q/Q

- More than 50% of Agentforce and Data 360 bookings came from existing customers in Q1

- In Q1, Data 360 ingested 52 trillion records, up 136% Y/Y, including 35 trillion via Zero Copy, up 277% Y/Y, and processed 12 terabytes of unstructured data

- Processed nearly 1 trillion API calls across Core products in Q1

- Slack Model Context Protocol (“MCP”) surpassed 1 million active users within six weeks of launch

- Public Sector Industry Cloud ARR surpasses $2 billion, up 23% Y/Y in Q1, with Public Sector AWUs up nearly 400% Q/Q

Guidance

- Initiates second quarter FY27 revenue guidance of $11.27 billion to $11.35 billion, up 10% – 11% Y/Y and 10% in CC, including slightly above 4pts Informatica contribution

- Raises midpoint of full year FY27 revenue guidance, now expects full year FY27 revenue of $45.9 billion to $46.2 billion, up 11% Y/Y and 10% – 11% in CC, including approximately 3pts Informatica contribution

- Maintains full year FY27 subscription & support revenue growth guidance of slightly under 12% Y/Y and approximately 11% in CC, including approximately 3pts Informatica contribution

- Updates full year FY27 GAAP operating margin guidance of 20.6%, and maintains non-GAAP operating margin guidance of 34.3%

- Updates full year FY27 operating cash flow growth guidance and free cash flow growth guidance to approximately 4% – 5% Y/Y to reflect the impact of the $25 billion debt issuance for the ASR

Salesforce’s guidance includes GAAP and non-GAAP financial measures.

Parts for iPhones to cost more owing to surging demand from AI companies.

Paine Schwartz joins BERO as a new investor as the year-old company seeks to triple sales.

Saudia is set to receive 12 new aircraft throughout 2026 as part of its fleet expansion strategy aimed at boosting capacity, improving efficiency, and strengthening global connectivity. The move supports the airline’s long-term growth plans and Saudi Vision 2030, with Saudia’s fleet expected to reach 161 aircraft by the end of the year.

2 minSaudia, the national flag carrier of the Kingdom of Saudi Arabia, continues its fleet expansion through ongoing planned deliveries of 12 new aircraft throughout 2026, reinforcing its long-term transformation strategy focused on growth, operational efficiency, and enhanced global connectivity.

The continued fleet expansion strengthens Saudia’s position as a leading global airline by increasing operational capacity, improving network flexibility, and supporting the development of new international destinations while enhancing the overall guest experience.

This growth reflects Saudia’s strategic commitment to fleet modernization in line with global aviation standards and evolving guest expectations. Through the integration of next-generation aircraft and advanced cabin products, Saudia continues to enhance its role in connecting the world to the Kingdom.

Following the introduction of Saudia’s first Airbus A321XLR, the Airbus A321neo further enhances the airline’s narrow-body capabilities. The aircraft features 20 Business Class seats and 168 Guest Class seats, with upgraded cabin design aimed at improving comfort, efficiency, and onboard experience.

The aircraft are equipped with high-speed inflight connectivity and improved seating, supporting both guest experience and operational performance.

His Excellency Engr. Ibrahim Al-Omar, Director General of Saudia Group, said: “Saudia’s fleet expansion strategy reflects a disciplined approach to building the capacity, efficiency, and readiness needed for the airline’s next phase of growth. In a highly competitive aviation sector, modernizing and growing the fleet must be guided by clear market insight, network requirements, and alignment with national priorities under Saudi Vision 2030. This level of planning also extends to operational readiness, ensuring that each new aircraft entering service is supported by the required operational and maintenance capabilities”.

He added: “Preparing the workforce for fleet expansion is just as important as preparing the aircraft themselves. Saudia has already graduated new cohorts of pilots, cabin crew, and maintenance specialists through training programs aligned with the highest international aviation standards, ensuring operational readiness as new aircraft continue to join the fleet. With Saudia’s fleet expected to reach 161 aircraft by the end of the year, additional cohorts are currently undergoing training to support future deliveries. This reflects Saudia’s continued commitment to developing national talent and strengthening local content capabilities”.

Saudia’s ongoing fleet expansion supports the Kingdom’s aviation and tourism ambitions under Saudi Vision 2030 by increasing global connectivity, enabling tourism growth, and strengthening Saudi Arabia’s position as a global aviation hub.

Two coming 2027 models – the first of the “Neue Klasse” cars coming to the U.S. early next year – have been revealed.

Chris Dixon, a partner who led the charge, says he has a ‘very long-term horizon’

The global smartphone market is facing its sharpest decline on record, with shipments expected to fall 14% in 2026, according to IDC. While Android devices could see a 20% drop, Apple is outperforming rivals thanks to stronger supply chain positioning and growing anticipation around its upcoming AI-powered iPhone updates.

2 min

Smartphone Slump. The smartphone has run into tough times. Sales of everyone’s favorite device could see the largest decline on record this year, according to market tracker IDC.

Worldwide smartphone shipments are expected to decline 14% in 2026 to 1.09 billion units, according to IDC. That’s down from IDC’s February forecast of a 12.9% decline and would mark the steepest annual contraction in smartphone history, the research firm said.

There’s one potential ray of light: While the industry outlook might be getting worse, estimates for Apple, AAPL +0.82%, iPhone sales are actually improving.

IDC now expects iPhone shipments to decline 5.2% this year, better than the previous forecast for an 8.1% decline. Handsets powered by Android, by contrast, could see a 20% year-over-year shipment drop, according to IDC.

The expected decline in smartphone shipments is being driven in part by the elevated cost of memory, a critical component in the buildout of artificial intelligence data centers. There’s a global shortage of most components used to power AI, like memory, as demand far outpaces supply. That’s led to soaring costs, a boon for memory makers like Micron Technology and a headwind for phone makers.

In recent months, other factors have emerged that are challenging smartphone sales.

“The U.S.-Iran war has added a fresh layer of cost pressure for smartphone OEMs, driven by rising oil prices and transportation costs,” Nabila Popal, IDC senior research director, wrote in the firm’s latest report. Combined with higher memory costs, these pressures are leading to vendors reducing shipments, raising prices, and concentrating on pushing out higher priced phone tiers, Popal added.

“That’s elevating smartphone [average selling prices] to a record $550, up $100 from last year,” she said.

Apple was better prepared than peers for the global chip shortage, according to IDC.

“Apple has done three things that few of its competitors have managed: it secured memory supply early, it built a portfolio strong enough to drive a remarkable turnaround in China, and it positioned the iPhone 17 to capture demand exactly when consumers in developed markets are extending replacement cycles and trading up,” Francisco Jeronimo, vice president for worldwide client devices at IDC, wrote.

Analysts expect Apple to show off highly anticipated AI updates at the company’s Worldwide Developers Conference, which kicks off on June 8. Apple is also expected to launch an expensive foldable iPhone this year. Strong demand for high performing AI and a physical redesign of the iPhone could bring in new customers and lead existing ones to update their current devices.

Apple shares have risen 15% this year. The stock was up 0.7% Wednesday afternoon, on pace to close at a record.

Parts for iPhones to cost more owing to surging demand from AI companies.

Americans now think they need at least $1.25 million for retirement, a 20% increase from a year ago, according to a survey by Northwestern Mutual

Rolls-Royce Motor Cars has unveiled five exclusive Black Badge Cullinan commissions created in collaboration with renowned artist Cyril Kongo, transforming each motor car into a one-of-one contemporary artwork. The collection features hand-painted interiors, bespoke Starlight Headliners inspired by the “Kongoverse,” and striking exterior details that reflect the bold and expressive spirit of Black Badge.

6 min“Creativity and imagination are the forces that define Rolls-Royce, shaping motor cars that are as individual as their owners. Our Private Offices, where clients co-create the most complex Bespoke commissions, directly reflect this belief. It was conversations within these spaces where the desire for bold contemporary art was identified among a uniquely daring and likeminded group of Rolls-Royce collectors. To bring this idea to life, we collaborated with Cyril Kongo, whose expressive, uncompromising style resonated perfectly with the spirit of Black Badge. What followed was an unprecedented collaboration, with Kongo working with and among our Bespoke Collective of designers, craftspeople and engineers to bring these extraordinary motor cars to life. Five unique Black Badge Cullinan Private Commissions are the result, each a unique work of art in its own right ,and represents the complete fusion of two unmistakable creative worlds”, Domagoj Dukec, Director of Design, Rolls-Royce Motor Cars.

“When I first saw Black Badge Cullinan, I felt compelled to create my own interpretation of the universe it belonged to – what I call ‘The Kongoverse’. It is a place of fantasy, mathematical formulas, symbols, pyramids, atoms and imagined planets. Rolls-Royce welcomed these ideas and gave them form – that’s what made it special. It was a conversation, using my visual language and Rolls-Royce’s way of making, with the motor car itself as the canvas. To bring that to life in collaboration with the brand’s artisans has been an extraordinary experience,” Cyril Kongo, Artist.

Rolls-Royce Motor Cars presents Black Badge Cullinan by Cyril Kongo; five exuberant Private Commissions featuring veneer and leather interior surfaces individually hand-painted by world-renowned multi-disciplinary artist, Cyril Kongo. All five motor cars share the same creative theme, but each features a unique expression of Kongo’s work. This project has been curated through the marque’s Private Offices in New York, Seoul, and the original Private Office at the Home of Rolls-Royce in Goodwood.

Black Badge Cullinan is a powerful canvas for Kongo’s work. As the darker, more subversive alter-ego of Rolls-Royce, Black Badge is the most daring expression of the brand. This mirrors the intensity of Kongo’s art, which appears on the Starlight Headliner, picnic tables, fascia, and Waterfall between the rear seats.

Using the interior surfaces of Black Badge Cullinan, Kongo brought ‘The Kongoverse’ – the artist’s aesthetic universe conceived for the collaboration with Rolls-Royce – to life within the motor car. This unique expression is shaped by destiny, imagination, and the power of individuality: themes that became central to Kongo during this landmark project.

An Unprecedented Collaboration

“What made this collaboration so special was the constant conversation between my universe and Rolls-Royce’s. Every idea was treated with care and curiosity. I was fully immersed in the brand’s creative studio,” Cyril Kongo, Artist.

To bring his vision to life, Rolls-Royce embraced Kongo as a member of the marque’s Bespoke Collective of designers, engineers and artisans. Though the marque has a rich heritage of collaborating with leading creatives, this project represents an unprecedented depth of co-creation. From the outset, Kongo was embedded within the Bespoke Collective, working alongside the Rolls-Royce teams at the Home of Rolls-Royce. He was involved in every stage of the project’s conception, design and realisation, with a dedicated space created for him, where Kongo painted each element by hand.

“The way we worked together with Cyril Kongo was unprecedented. Six months before production began, we brought him to the Home of Rolls-Royce at Goodwood and immersed him in our world, meeting our specialists and craftspeople, sharing our tools and techniques, and placing our full paint palette at his disposal. When we came to co-create the motor cars, we set up dedicated workspaces within our Bespoke facilities, where Cyril and our specialists worked hand-in-hand, integrating his artistic language into each element. The collaboration fostered a continuous exchange of ideas and a shared spirit of curiosity and creative confidence. This fully embedded, in-house approach gave Cyril the freedom to explore his vision in the moment, true to the spontaneous nature of his art,” Phil Fabre de la Grange, Head of Bespoke, Rolls-Royce Motor Cars.

Vivid Worlds: Adventures in the Kongoverse

“My art reflects the infinite power of imagination – picturing worlds that do not exist, but which could. To bring this vision to life with a Rolls-Royce was unforgettable,” Cyril Kongo, Artist.

Each motor car shares the same interior color treatment: a Black foundation with vivid bursts of color. For the first time, the interior is divided into four distinct zones, each defined by a contrasting colorway: Phoenix Red for the driver’s seat, Turchese for the front passenger’s seat, and Forge Yellow and Mandarin for the rear. These colors are expressed through stitching, piping, seat inserts and the ‘RR’ monograms on the headrests, as well as the lambswool carpets. From this shared palette, Kongo hand-painted five individual interior artworks, transforming each motor car into a true one-of-one collector’s piece.

Starlight Headliner: The Kongoverse, written in stars

A hand-painted Starlight Headliner – a roof lining creating the impression of a serene night sky within the motor car with 1,344 fiber-optic ‘stars’ – is the focal point of each Black Badge Cullinan by Cyril Kongo. In each artwork, Kongo introduces imagined planets and constellations alongside references to quantum physics – a subject that has fascinated him since sharing a studio with his brother, who is a physicist. Equations and formulae are embedded within his compositions, symbolizing the infinite potential of the imagination: a theme echoed in the infinity symbol, which codifies all Rolls-Royce Black Badge motor cars.

To realize his vision, Interior Surface Centre craftspeople prepared more than 70 paint colors, giving Kongo complete creative freedom to bring his artwork to life. Each composition was applied using a combination of sponges, airbrushes and brush tools.

After painting the Starlight Headliner, Kongo worked closely with Bespoke engineers to define the precise placement and color of all ‘stars’. Each ‘star’ was counted and individually marked by the artist before being painstakingly hand-punched and placed by the marque’s artisans. Each Starlight Headliner features various combinations of Blue, Phoenix Red, Forge Yellow, Cobalto Blue, Twickenham Green or Lime Green illuminations and eight Shooting Stars, including a final ‘star’ that spans the entire length of the ceiling – a Rolls-Royce first.

As a final, hidden detail, Kongo’s signature ‘tag’ motif is painted on the leather lining inside the sun visor and inside the luggage compartment lid. This hallmark design is also faithfully recreated in fine embroidery on the door leather.

Hand-painted interior surfaces: a continuous composition

“We talked about how to make the piece groove, how to keep the rhythm inside the motor car. For me, painting is like jazz. You move, but everything stays connected,” Cyril Kongo, Artist.

Each Black Badge Cullinan by Cyril Kongo features a Bespoke woodset individually hand-painted by the artist, extending across the fascia, center console, rear console, Picnic Tables and the Waterfall between the rear seats. Together, these elements form a single, continuous composition within the motor car.

Ahead of Kongo’s arrival, the Interior Surface Centre prepared each of the 19 veneered pieces by painting them in black and mounting them on specially created fixtures within the marque’s paint laboratory. Working directly onto these surfaces, Kongo applied his signature Kongoverse designs using airbrushes of varying sizes to achieve different levels of detail.

To enhance and protect the artworks, Rolls-Royce artisans applied ten layers of lacquer to each surface. Each piece was then sanded and polished to a brilliant finish, ensuring the depth and durability expected of a Rolls-Royce interior.

Bespoke Exterior: A Powerful Canvas

“I want people to discover this artwork step by step. The more you explore, the more you see. The exterior should only hint at the universe inside,” Cyril Kongo, Artist.

Each Black Badge Cullinan by Cyril Kongo motor car is presented in a rich Blue Crystal Over Black finish: the deep black paint is further elevated with a lacquer infused with blue particles that shimmer in sunlight, allowing the surface to appear almost blue in certain light. In a Rolls-Royce first, each features a Gradient Coachline: Phoenix Red transitions to Forge Yellow along the left side, Mandarin fades into Turchese along the right, with Kongo’s distinctive ‘tag’ symbol incorporated as a Bespoke motif within both. In another Rolls-Royce first, behind each 23-inch Part Polished Black Badge alloy wheel is a different coloured brake calliper: Phoenix Red, Turchese, Forge Yellow and Mandarin – colours selected to match the Coachline and the vivid colour accents in the interior.

The Phoenix Red ‘tag’ graphic used in the exterior Coachline is carried through to the Bespoke Illuminated Treadplates and the black Bespoke umbrellas concealed in the doors, where it appears as a subtle motif on the canopy.

Curated by Private Offices: The Power of Connection

The Black Badge Cullinan by Cyril Kongo project has been curated by Rolls-Royce Private Offices in Seoul, New York, and the original at Goodwood. Private Offices are creative hubs, available by invitation only, which serve as extensions of the Home of Rolls-Royce and further elevate the experience of commissioning a Bespoke Rolls-Royce motor car.

Each Private Office has a dedicated Rolls-Royce team based permanently in the region. Their deeply personal relationships with clients give them a unique insight into the cultural cues, passions, and interests of local collectors. It is through this lens that the Cyril Kongo collaboration took shape as both an artistic statement and a reflection of contemporary collector culture.

All five Black Badge Cullinan by Cyril Kongo motor cars are allocated to collectors worldwide.

Two coming 2027 models – the first of the “Neue Klasse” cars coming to the U.S. early next year – have been revealed.

Interior designer Thomas Hamel on where it goes wrong in so many homes.

AI chatbots are becoming more personalized through memory features, but experts warn that outdated or misunderstood information can quietly influence future responses, raising concerns around privacy, bias, and emotional reinforcement.

5 min

Brian Del Rosario, a software engineer and part-time city-council member in a small town in Utah, uses AI chatbots for everything from meal planning to managing his schedule. In some of those conversations, he revealed he had a spouse and three children.

Then, after he and his wife separated, Del Rosario had to mention it to the chatbot so it wouldn’t include his wife when planning a future trip. But once he did, the chatbot latched onto the divorce.

When he asked for help managing his schedule, it suggested he might be stretching himself thin because of the divorce. When he vented about a frustrating day at work, it tied his stress back to the divorce.

He says he told the chatbot, “I wasn’t trying to have you opine about my divorce at every chance.” The chatbot, says Del Rosario, “wouldn’t let go of it.”

One of the best things about chatbots is that they have a long memory, learning more about you from one conversation to the next. The result is a smarter assistant that knows your writing style, remembers your dietary restrictions or picks up a project where you left off.

But that great memory also carries some drawbacks. It can get stuck on misunderstood or outdated information. It can feel invasive. And it can make it harder to turn a new page in your life.

In other words, you may be over it, but your chatbot isn’t.

Forever facts

Since ChatGPT introduced memory in early 2024, Google’s Gemini, Anthropic’s Claude and Microsoft’s Copilot have all added their own versions. Their approaches differ, but the basic idea is the same: The chatbot remembers what you have told it and uses that to shape future responses. Google’s Personal Intelligence feature can even pull from a user’s Gmail, Photos and YouTube activity.

One problem: It may be remembering things that aren’t about you at all. For instance, a health question asked on behalf of a child or parent can be mistaken for your own. Ask about symptoms of ADHD for your child, and weeks later when you ask for productivity advice, the chatbot may tailor its suggestions around attention difficulties it thinks you have.

Google, an Alphabet unit, acknowledged a version of this problem in a blog post about its Personal Intelligence feature, describing a hypothetical case where the system saw hundreds of photos of a user at a golf course and assumed he loved the sport, when really he was just there for his son. (In the hypothetical, the user had to tell the chatbot he doesn’t like golf.)

Google says it has introduced a feature that lets users keep personalization on but block specific information from resurfacing in conversations with the chatbot. OpenAI, meanwhile, says it has shipped an update for Plus and Pro users that improves how memory finds and retrieves details. Microsoft says that users can update or delete specific memories (or everything, if they choose). They can also turn personalization and memory off entirely at any time. Anthropic declined to comment.

In a shared account, common enough between partners or in small businesses, the risks multiply. One person uses the chatbot to polish a résumé. Later, when someone else on the account asks an unrelated question, the chatbot might reference that person’s recent career move or suggest next steps for a job search as part of the answer.

Memories can also go stale. Say you told the chatbot you were training for a marathon six months ago. Since then you tore your ACL, but you never mentioned that. Now every meal plan and fitness suggestion is calibrated for someone who’s highly active. You’re following advice built for a version of you that no longer exists.

A real downer

Del Rosario experienced something similar. He had mentioned he was trying to lose weight, and the chatbot started bringing up that fact everywhere, including when he was looking for restaurant recommendations while out of town.

“It was like, ‘Thanks for being the buzzkill about my vacation,’ ” he says. “I wasn’t actually planning to stick to my diet on this trip.”

Similarly, Mike Taylor, a tech consultant for media and software company Every in Hoboken, N.J., once mentioned to a chatbot that he was a British expat. Subsequently, he says, the chatbot recommended a “proper pint” at a local bar, a tip he didn’t find useful. “I’m here for American dive bars, not the British ones,” he says. “That’s why I moved here.”

Taylor has turned his AI chatbot memory off, so that he knows exactly what’s shaping how it responds to him. “The LLM [large language model] doesn’t know who you are, and therefore it won’t bias the results you get,” he says.

Indeed, AI memory can shape results in ways that can be hard to detect. Joshua Joseph, the chief AI scientist at Harvard University’s Berkman Klein Center, compared the effect to a social-media feed and the way a few posts you linger on can quietly reshape everything you see afterward.

Say you mention you’re stressed about money in a conversation about something else entirely. Weeks later, you ask the chatbot for career advice, and it steers you toward higher-paying jobs rather than roles that might be a better fit, because it “knows” you’re financially anxious. You would never know why the advice felt off, because the chatbot hasn’t flagged which memories it is drawing on.

“It definitely steers, it definitely impacts results,” Joseph says. “And we don’t really know how much.” He keeps memory turned off on his own chatbot accounts.

A chatbot that remembers everything can also make it harder for people to move on from their own past. Lucy Osler, a philosophy lecturer at the University of Exeter who studies how artificial intelligence shapes cognition, says chatbots use facts to construct a narrative about who you are, and feed that narrative back to you as though it were fact. If you tell your chatbot you’re feeling insecure and anxious, that becomes how it sees you, and may keep reminding you of that even if you’ve moved on.

“That might confirm certain self-narratives I have about myself and make them sound more real,” Osler says. “They can box you in.”

Negative patterns

Being reminded you were anxious months after the fact can be upsetting. But it can also do real harm. Chatbots are designed to be agreeable, to build on your version of reality rather than question it. Osler says this makes chatbots capable of reinforcing delusional thinking.

This concern has led the Electronic Privacy Information Center to draft legislation around chatbot safety for teenagers, a population particularly vulnerable to the sycophantic tendencies of these tools. A key provision calls for wiping memory between sessions, specifically to prevent chatbots from building on harmful mental states over time.

Del Rosario eventually came up with his own approach. After the divorce kept leaking into unrelated conversations, he started dedicating separate chatbots to separate parts of his life and using anonymous mode for anything sensitive.

He still values it when it works, like when it knows his children need car seats on a road trip, or when it reminds him he has a lot on his plate. His mom died two years ago, and between that, the divorce, the children and work, the chatbot is sometimes the only thing that gets the full picture.

“It feels good to be seen, even if it is by an AI chatbot,” he says.

Major AI assistants let users turn off memory entirely, and each offers some way to view, edit or delete what’s been stored. But many users don’t know about these newer capabilities, or never check these settings. Here are some tips for making sure the memory feature works to your advantage:

Learn what your chatbot knows about you. Go to your settings—in ChatGPT it is under Personalization, in Claude and Gemini it is in the memory section—and review what’s there and delete if necessary.

Use temporary chats for anything sensitive. Or just don’t tell it anything sensitive. The controls—and names—for temporary chat can differ from app to app, but there is often a button at the top of the page.

Try turning memory off entirely to see how it changes your results. You might find you prefer the trade-off.

Treat it like a social-media profile. It is worth checking in and updating on occasionally, because it is shaping what you see whether you look at it or not.

New research suggests that bonuses make employees feel more like a mere cog in a wheel.

Following the devastation of recent flooding, experts are urging government intervention to drive the cessation of building in areas at risk.

Saudi Arabia’s GACA has issued the first operational permit for drone-based delivery of medicines and medical supplies during the 2026 Hajj season in Makkah’s holy sites. The move reflects the Kingdom’s push to adopt advanced technologies in serving pilgrims while improving the speed and efficiency of medical and logistics operations under Saudi Vision 2030.

< 1 min

The General Authority of Civil Aviation (GACA) has issued the first operational permit for limited drone-based delivery of medicines and medical logistics to Terra Drone Arabia within the holy sites in Makkah during the 2026 Hajj season.

This reflects the authority’s commitment to adopting advanced technologies in the service of pilgrims.

The permit supports GACA’s efforts to advance the aviation sector, localize innovative solutions, and improve operational efficiency and response speed for medical and logistics services under the highest safety and quality standards.

The move builds on pilot operations conducted during last year’s Hajj, paving the way for the first permit of its kind, supporting Saudi Vision 2030 and the Aviation Program’s objectives.

Parts for iPhones to cost more owing to surging demand from AI companies.

Towell Auto Group has introduced the legendary 212 off-road SUV brand to Oman, launching the Adventurer and flagship Navigator models built for rugged terrain, desert driving, and extreme 4×4 performance. Designed with authentic body-on-frame engineering and advanced off-road technologies, the 212 range brings over six decades of off-road heritage to Oman’s adventure-driven market.

3 min

Towell Auto Group officially introduced the legendary 212 4×4 SUV brand to Oman, bringing with it a heritage of true off-road capability engineered for enthusiasts who demand far more than conventional urban SUVs.

Purpose-built to conquer Oman’s diverse landscapes, from towering mountains and rugged wadis to deep desert terrain and rocky trails, the 212 arrives as a serious body-on-frame off-road SUV designed for adventure-seekers who value uncompromising capability, durability and adventure. The launch introduces two distinct models to Oman — the 212 Adventurer and the flagship 212 Navigator, both engineered to deliver robust 4×4 performance with advanced off-road technologies and inspiring mechanical engineering.