Europeans Are Becoming Poorer. ‘Yes, We’re All Worse Off.’

An ageing population that values its free time set the stage for economic stagnation. Then came Covid-19 and Russia’s war in Ukraine.

8 min

8 min

Europeans are facing a new economic reality, one they haven’t experienced in decades. They are becoming poorer.

Life on a continent long envied by outsiders for its art de vivre is rapidly losing its shine as Europeans see their purchasing power melt away.

The French are eating less foie gras and drinking less red wine. Spaniards are stinting on olive oil. Finns are being urged to use saunas on windy days when energy is less expensive. Across Germany, meat and milk consumption has fallen to the lowest level in three decades and the once-booming market for organic food has tanked. Italy’s economic development minister, Adolfo Urso, convened a crisis meeting in May over prices for pasta, the country’s favourite staple, after they jumped by more than double the national inflation rate.

With consumption spending in free fall, Europe tipped into recession at the start of the year, reinforcing a sense of relative economic, political and military decline that kicked in at the start of the century.

Europe’s current predicament has been long in the making. An ageing population with a preference for free time and job security over earnings ushered in years of lacklustre economic and productivity growth. Then came the one-two punch of the Covid-19 pandemic and Russia’s protracted war in Ukraine. By upending global supply chains and sending the prices of energy and food rocketing, the crises aggravated ailments that had been festering for decades.

Governments’ responses only compounded the problem. To preserve jobs, they steered their subsidies primarily to employers, leaving consumers without a cash cushion when the price shock came. Americans, by contrast, benefited from inexpensive energy and government aid directed primarily at citizens to keep them spending.

In the past, the continent’s formidable export industry might have come to the rescue. But a sluggish recovery in China, a critical market for Europe, is undermining that growth pillar. High energy costs and rampant inflation at a level not seen since the 1970s are dulling manufacturers’ price advantage in international markets and smashing the continent’s once-harmonious labor relations. As global trade cools, Europe’s heavy reliance on exports—which account for about 50% of eurozone GDP versus 10% for the U.S.—is becoming a weakness.

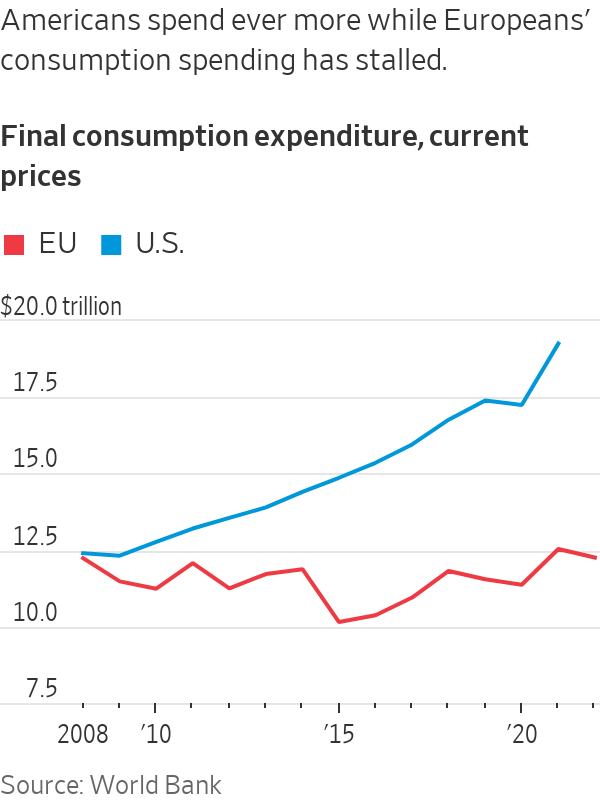

Private consumption has declined by about 1% in the 20-nation eurozone since the end of 2019 after adjusting for inflation, according to the Organization for Economic Cooperation and Development, a Paris-based club of mainly wealthy countries. In the U.S., where households enjoy a strong labor market and rising incomes, it has increased by nearly 9%. The European Union now accounts for about 18% of all global consumption spending, compared with 28% for America. Fifteen years ago, the EU and the U.S. each represented about a quarter of that total.

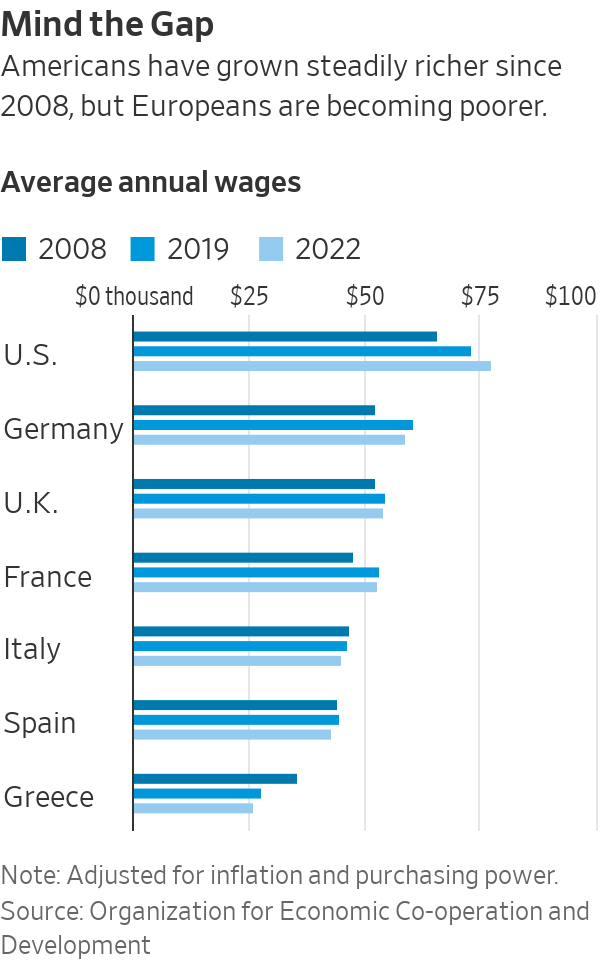

Adjusted for inflation and purchasing power, wages have declined by about 3% since 2019 in Germany, by 3.5% in Italy and Spain and by 6% in Greece. Real wages in the U.S. have increased by about 6% over the same period, according to OECD data.

The pain reaches far into the middle classes. In Brussels, one of Europe’s richest cities, teachers and nurses stood in line on a recent evening to collect half-price groceries from the back of a truck. The vendor, Happy Hours Market, collects food close to its expiration date from supermarkets and advertises it through an app. Customers can order in the early afternoon and collect their cut-price groceries in the evening.

“Some customers tell me, because of you I can eat meat two or three times per week,” said Pierre van Hede, who was handing out crates of groceries.

Karim Bouazza, a 33-year-old nurse who was stocking up on half-price meat and fish for his wife and two children, complained that inflation means “you almost need to work a second job to pay for everything.”

Similar services have sprung up across the region, marketing themselves as a way to reduce food waste as well as save money. TooGoodToGo, a company founded in Denmark in 2015 that sells leftover food from retailers and restaurants, has 76 million registered users across Europe, roughly three times the number at the end of 2020. In Germany, Sirplus, a startup created in 2017, offers “rescued” food, including products past their sell-by date, on its online store. So does Motatos, created in Sweden in 2014 and now present in Finland, Germany, Denmark and the U.K.

Spending on high-end groceries has collapsed. Germans consumed 52 kilograms of meat per person in 2022, about 8% less than the previous year and the lowest level since calculations began in 1989. While some of that reflects societal concerns about healthy eating and animal welfare, experts say the trend has been accelerated by meat prices which increased by up to 30% in recent months. Germans are also swapping meats such as beef and veal for less-expensive ones such as poultry, according to the Federal Information Center for Agriculture.

Thomas Wolff, an organic-food supplier near Frankfurt, said his sales fell by up to 30% last year as inflation surged. Wolff said he had hired 33 people earlier in the pandemic to handle strong demand for pricey ecological foodstuffs, but he has since let them all go.

Ronja Ebeling, a 26-year-old consultant and author based in Hamburg, said she saves about one-quarter of her income, partly because she worries about having enough money for retirement. She spends little on clothes or makeup and shares a car with her partner’s father.

Weak spending and poor demographic prospects are making Europe less attractive for businesses ranging from consumer-goods giant Procter & Gamble to luxury empire LVMH, which are making an ever-larger share of their sales in North America.

“The U.S. consumer is more resilient than in Europe,” Unilever’s chief financial officer, Graeme Pitkethly, said in April.

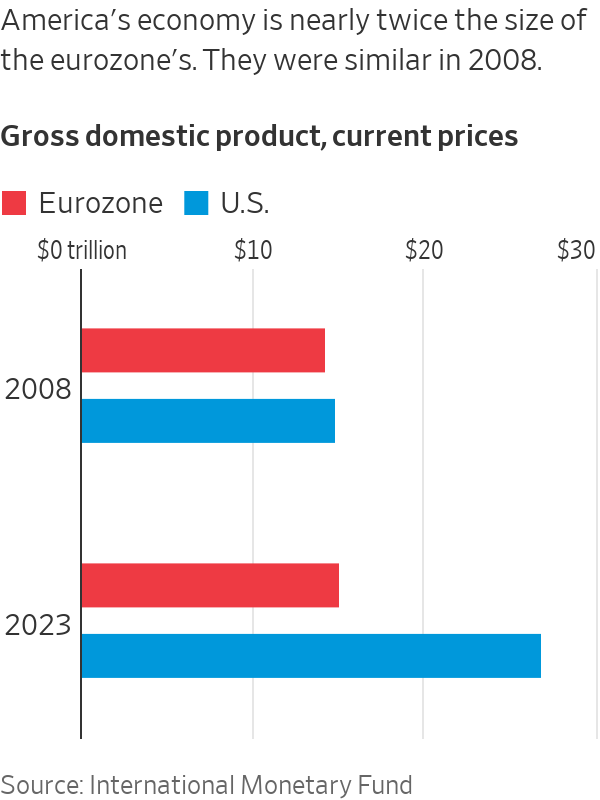

The eurozone economy grew about 6% over the past 15 years, measured in dollars, compared with 82% for the U.S., according to International Monetary Fund data. That has left the average EU country poorer per head than every U.S. state except Idaho and Mississippi, according to a report this month by the European Centre for International Political Economy, a Brussels-based independent think tank. If the current trend continues, by 2035 the gap between economic output per capita in the U.S. and EU will be as large as that between Japan and Ecuador today, the report said.

On the Mediterranean island of Mallorca, businesses are lobbying for more flights to the U.S. to increase the number of free-spending American tourists, said Maria Frontera, president of the Mallorca Chamber of Commerce’s tourism commission. Americans spend about €260 ($292) per day on average on hotels compared with less than €180 ($202) for Europeans.

“This year we have seen a big change in the behaviour of Europeans because of the economic situation we are dealing with,” said Frontera, who recently traveled to Miami to learn how to better cater to American customers.

Weak growth and rising interest rates are straining Europe’s generous welfare states, which provide popular healthcare services and pensions. European governments find the old recipes for fixing the problem are either becoming unaffordable or have stopped working. Three-quarters of a trillion euros in subsidies, tax breaks and other forms of relief have gone to consumers and businesses to offset higher energy costs—something economists say is now itself fuelling inflation, defeating the subsidies’ purpose.

Public-spending cuts after the global financial crisis starved Europe’s state-funded healthcare systems, especially the U.K.’s National Health Service.

Vivek Trivedi, a 31-year-old anaesthesiologist living in Manchester, England, earns about £51,000 ($67,000) per year for a 48-hour workweek. Inflation, which has been about 10% or higher in the U.K. for nearly a year, is devouring his monthly budget, he says. Trivedi said he shops for groceries in discount retailers and spends less on meals out. Some colleagues turned off their heating entirely over recent months, worried they wouldn’t be able to afford sharply higher costs, he said.

Noa Cohen, a 28-year old public-affairs specialist in London, says she could quadruple her salary in the same job by leveraging her U.S. passport to move across the Atlantic. Cohen recently got a 10% pay raise after switching jobs, but the increase was completely swallowed by inflation. She says friends are freezing their eggs because they can’t afford children anytime soon, in the hope that they have enough money in future.

“It feels like a perma-freeze in living standards,” she said.

Huw Pill, the Bank of England’s chief economist, warned U.K. citizens in April that they need to accept that they are poorer and stop pushing for higher wages. “Yes, we’re all worse off,” he said, saying that seeking to offset rising prices with higher wages would only fuel more inflation.

With European governments needing to increase defence spending and given rising borrowing costs, economists expect taxes to increase, adding pressure on consumers. Taxes in Europe are already high relative to those in other wealthy countries, equivalent to around 40-45% of GDP compared with 27% in the U.S. American workers take home almost three-quarters of their pay checks, including income taxes and Social Security taxes, while French and German workers keep just half.

The pauperisation of Europe has bolstered the ranks of labor unions, which are picking up tens of thousands of members across the continent, reversing a decades long decline.

Higher unionisation may not translate into fuller pockets for members. That’s because many are pushing workers’ preference for more free time over higher pay, even in a world of spiralling skills shortages.

IG Metall, Germany’s biggest trade union, is calling for a four-day work week at current salary levels rather than a pay raise for the country’s metalworkers ahead of collective bargaining negotiations this November. Officials say the shorter week would improve workers’ health and quality of life while at the same time making the industry more attractive to younger workers.

Almost half of employees in Germany’s health industry choose to work around 30 hours per week rather than full time, reflecting tough working conditions, said Frank Werneke, chairman of the country’s United Services Trade Union, which has added about 110,000 new members in recent months, the biggest increase in 22 years.

Kristian Kallio, a games developer in northern Finland, recently decided to reduce his working week by one-fifth to 30 hours in exchange for a 10% pay cut. He now makes about €2,500 per month. “Who wouldn’t want to work shorter hours?” Kallio said. About one-third of his colleagues took the same deal, although leaders work full-time, said Kallio’s boss, Jaakko Kylmäoja.

Kallio now works from 10 a.m. to 4.30 p.m. He uses his extra free time for hobbies, to make good food and take long bike rides. “I don’t see a reality where I would go back to normal working hours,” he said.

Igor Chaykovskiy, a 34-year-old IT worker in Paris, joined a trade union earlier this year to press for better pay and conditions. He recently received a 3.5% pay increase, about half the level of inflation. He thinks the union will give workers greater leverage to press managers. Still, it isn’t just about pay. “Maybe they say you don’t have an increase in salary, you have free sports lessons or music lessons,” he said.

At the Stellantis auto factory in Melfi, southern Italy, employees have worked shorter hours for years recently due to the difficulty of procuring raw materials and high energy costs, said Marco Lomio, a trade unionist with the Italian Union of Metalworkers. Hours worked have recently been reduced by around 30% and wages decreased proportionally.

“Between high inflation and rising energy costs for workers,” said Lomio, “it is difficult to bear all family expenses.”

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Bahrain’s Electricity and Water Authority (EWA) has named ACWA Power as the sole bidder for the Hidd Independent Water Project. The new seawater desalination plant will have a capacity of 11,364 cubic meters per hour, strengthening the kingdom’s potable water supply and supporting growing residential, commercial, and industrial demand through advanced water treatment technology.

Eurozone inflation eased to 2.8% in June as lower energy prices cooled consumer costs, strengthening expectations that the European Central Bank will keep interest rates unchanged at its July meeting.

GCC banks are expected to post strong profits in 2026, led by Al Rajhi Bank with forecast earnings growth of 13.6%, according to S&P Global Market Intelligence.

Paramount’s $80 billion merger with Warner Bros. Discovery promises a new era for Hollywood—but also leaves the combined media giant with nearly $80 billion in debt. As David Ellison bets on growth, streaming and blockbuster content, analysts say delivering $6 billion in promised synergies will be critical to easing the financial burden.

3 min

When Paramount PSKY -1.91%decrease; Chief Executive David Ellison unveiled his company’s $81 billion deal for Warner Bros. Discovery WBD 0.11%increase; he touted a new golden era for Hollywood—one built on scale, technology and a promise to release at least 30 theatrical movies a year.

His plan has little margin for error.

The combined company is set to emerge with nearly $80 billion in debt—a burden that could weigh on decisions ranging from content spending and streaming investments to news operations and sports rights.

Its net debt is projected to equal roughly 6.5 times annual earnings before interest, taxes, depreciation and amortization after the deal closes as soon as this month, a level that analysts consider high for a media company. Industry analysts at MoffettNathanson called the figure “staggering” in a note shortly after the deal.

The challenge for Ellison will be to cut costs without the sort of austerity measures that defined Warner’s debt-reduction effort under Chief Executive David Zaslav. Thousands of employees were laid off, and high-profile movie and TV projects were scrapped.

Many current and former Warner executives said repeated rounds of cost-cutting have already eliminated much of the obvious savings, leaving them wondering what is left to prune. Paramount has been through several cycles of cost-cutting in recent years, both before and after the sale to Ellison’s Skydance.

Much of Ellison’s financial flexibility—and the combined company’s prospects for success—depend on delivering the $6 billion in promised synergies within three years, a target some analysts view as ambitious given the scale of the integration.

The debt and looming cuts are a shadow hanging over a company that will house two of Hollywood’s founding movie studios, several famed TV brands, including CNN and MTV, and a supersize streaming service.

David Ellison, backed by his billionaire father, Larry Ellison, is making a huge bet on content as the entertainment and media landscape faces higher sports-rights costs, a competitive streaming market and a risky box-office environment.

The younger Ellison has promised that there will be no asset sales or cuts to content spending. The deal has been approved by the Justice Department, and the company is trying to get regulatory clearance in Europe.

“This transaction is premised on growth, not cost-cutting,” Paramount said in a statement, adding, “We will be reducing debt while continuing to invest in the business and content for the long term.”

Paramount said that having the Ellison family as controlling owners with significant skin in the game is an advantage. Executives at Paramount said the company has increased movie production and sports-rights acquisitions while approaching $3 billion in efficiencies.

“This is a key advantage of a creative-first owner-operator,” said Paramount, calling its strategy for the Warner deal “the same proven playbook we have successfully executed at Paramount.”

For now, Paramount is limited in what it can do. Until the deal closes, the company has only a partial view of Warner’s operations and is restricted in how deeply it can examine the business.

There could be hidden land mines. Discovery executives said they uncovered a number of unexpected challenges, including the high costs of the short-lived streaming service CNN+, only after taking control of WarnerMedia following the 2022 merger.

Paramount has said much of the savings will come from consolidating streaming services’ technology platforms and eliminating overlapping operations with Warner, a process expected to result in significant job cuts.

Paramount is projecting that the combined company will generate about $69 billion in annual revenue. After achieving its synergies, it expects adjusted Ebitda of about $18 billion. Paramount is projecting a content budget of more than $30 billion for the combined company at closing.

Paramount has told investors it will lower the debt ratio to three times annual Ebitda within three years, which MoffettNathanson said is too optimistic in its note.

The assets producing much of the cash to pay the debt are themselves under pressure. The combined company won’t be relying on a stable business to pay down debt. It will be primarily relying on television networks, whose revenue continues to decline.

While the combined company’s network holdings, which include CNN, CBS, MTV and Nickelodeon, still generate about $35 billion in annual revenue, the sector remains under pressure from cord-cutting and ad declines. Moody’s Ratings estimates that revenue will fall at an average annual rate of almost 10% for the foreseeable future.

Ellison is betting heavily that the combination of the streaming platforms Paramount+ and Pluto TV with Warner’s HBO Max will create a more formidable streaming competitor and generate more cash.

“We estimate it will take at least five years until the streaming business earnings matches the scale of TV media,” Moody’s said.

Paine Schwartz joins BERO as a new investor as the year-old company seeks to triple sales.

The sports-car maker delivered 279,449 cars last year, down from 310,718 in 2024.

SpaceX will officially join the Nasdaq-100, prompting index-tracking funds to buy its shares. Despite its $2.1 trillion valuation, the company will initially account for less than 1% of the index due to its limited public share float.

2 min

SpaceX (SPCX -0.98%) decrease; will officially join the Nasdaq-100 and investors holding some funds tied to the index will end up exposed whether they like it or not.

Mutual and exchange-traded funds with a collective $800 billion in assets under management that track Nasdaq’s flagship tech index, including the popular Invesco QQQ ETF, are set to buy SpaceX shares at Monday’s closing price in order to mirror the index’s performance.

That comes after Elon Musk’s artificial-intelligence and-rocket-making company was fast-tracked into the Nasdaq-100 under new rules that aim to include newly public megacap companies sooner. Here’s what you need to know:

SpaceX will be a small component, for now

Even though SpaceX’s $2.1 trillion market cap makes it one of the most-valuable companies in the U.S., it won’t enter the cap-weighted index as one of the top components.

That’s because SpaceX sold less than 5% of its total shares in last month’s public offering. Combined with lockup rules that prevent employees from selling the stock for several months or more, that means a small fraction of the company’s shares are currently circulating publicly.

The Nasdaq adjusts index weights by a company’s so-called free-float, or the number of shares available to trade publicly, capping the weight at three times a company’s float-adjusted market capitalization. For SpaceX, that means it will initially be treated more like a $300 billion company than a $2 trillion one, and have an initial index weight of less than 1%.

QQQ is the biggest fund adding SpaceX, but not the cheapest

With roughly half a trillion dollars in assets, Invesco’s QQQ ETF is the biggest fund tracking the Nasdaq-100 and the fifth-largest ETF overall. A long-running marketing campaign has made QQQ a favorite fund among individual investors, but those seeking the lowest fees now have cheaper options.

State Street’s newly launched SPDR Portfolio Nasdaq 100 fund is charging holders a 0.1% annual fee on their assets—or $10 on a $10,000 investment—undercutting QQQ’s 0.18% fee. A new BlackRock fund tracking the index is set to launch shortly, and Invesco also offers the QQQM ETF at a 0.15% annual fee.

Index inclusion can boost a stock

SpaceX advisers reached out to index providers earlier this year seeking early inclusion for a reason: The trillions of dollars parked in passive, index-tracking funds create automatic demand for included stocks, an important source of support for share prices.

When an ETF has more buyers than sellers, the fund manager creates shares to fill that demand. QQQM, for instance, has reported a net inflow of $16 billion so far this year, meaning the fund has purchased billions of dollars in additional shares of the companies it tracks.

The opposite is true if a fund has net outflows, of course, but U.S. equity ETFs have been posting net inflow records year after year.

But gains are far from guaranteed

As employee lockup periods end over the next year, index funds are likely to help absorb some of the selling from employees looking to cash out—a phenomenon that analysts say has weighed on shares of newly public companies like Facebook in the past.

Still, the float adjustments are keeping a lid on how much SpaceX Nasdaq-100 funds will need to buy, and the company won’t be joining the most widely tracked index, the S&P 500, for at least a year.

While index inclusion can provide important support for a stock in its early days, analysts said the company’s financial performance and the number of investors who want to buy its shares directly are likely more important drivers of long-term performance.

Two coming 2027 models – the first of the “Neue Klasse” cars coming to the U.S. early next year – have been revealed.

New research suggests that bonuses make employees feel more like a mere cog in a wheel.

ADX will remove daily trading limits on ETFs and futures from 3 August 2026, aiming to boost liquidity, improve price discovery, and give investors greater trading flexibility. The move supports the exchange’s strategy to build a more efficient and modern market.

< 1 min

The Abu Dhabi Securities Exchange (ADX) Group today announced the removal of daily price limits for Exchange Traded Funds (ETFs) and futures contracts listed on the Exchange, reinforcing its commitment to a more efficient, liquid, and investor-responsive market.

This will be in effect from 3rd August 2026.

The initiative is designed to support more efficient price formation, more continuous liquidity provision, and smoother trading for investors. By allowing ETFs and futures prices to reflect new information in real time, ADX is reducing trading disruptions such as trading halts and pauses caused by daily bands, while strengthening quality of market price formation and efficiency.

As the most liquid ETF hub in the MENA region, ADX offers a broad and diverse range of products, including thematic and Sharia-compliant funds. The removal of price limits further enhances the advantages of the platform for investors seeking efficient investment execution and diversified exposure.

The move also supports the continued development of ADX’s derivatives market. Removing price limits gives investors greater flexibility to hedge exposures and implement investment strategies without restrictions caused by trading price limits.

The removal of price limits for ETFs and futures contracts is aligned with ADX’s broader strategy to provide investors with greater agility and modern market infrastructure that supports efficient capital allocation, enhanced liquidity, and advanced risk management.

ADX will continue to manage intraday volatility, including temporary trading pauses in exceptional circumstances to maintain an orderly market.

Following the successful launch of its Palais Collection, MAISON de SABRÉ has unveiled a new modular handbag system offering more than 720 styling combinations.

Parts for iPhones to cost more owing to surging demand from AI companies.

Bahrain’s Electricity and Water Authority (EWA) has named ACWA Power as the sole bidder for the Hidd Independent Water Project. The new seawater desalination plant will have a capacity of 11,364 cubic meters per hour, strengthening the kingdom’s potable water supply and supporting growing residential, commercial, and industrial demand through advanced water treatment technology.

< 1 minBahrain’s Electricity and Water Authority (EWA) has announced that top Saudi utility developer Acwa has emerged as the sole bidder for Hidd Independent Water Project. The key facility will boast a 11,364 cu m per hour capacity, thus contributing substantially to the kingdom’s potable water supply.

A major seawater reverse osmosis (SWRO) desalination plant in the kingdom, Hidd IWP will be implemented on a Build-Own-Operate (BOO) basis.

The key facility will have a Guaranteed Net Contracted Water Capacity (GNCWC) of 11,364 cu m per hour, contributing substantially to Bahrain’s potable water supply and supporting growing residential, commercial, and industrial demand, said EWA in its tender notification.

The Hidd IWP Project reflects Bahrain’s continued commitment to expanding its desalination capacity through private sector participation and advanced water treatment technologies, ensuring long-term sustainability and reliable water supply for the kingdom, it added.

Many of the most-important events have slipped from our collective memories. But their impacts live on.

Chris Dixon, a partner who led the charge, says he has a ‘very long-term horizon’

Eurozone inflation eased to 2.8% in June as lower energy prices cooled consumer costs, strengthening expectations that the European Central Bank will keep interest rates unchanged at its July meeting.

2 minCooling energy prices helped push eurozone inflation lower in June, increasing the likelihood that the European Central Bank will hold rates steady later this month after raising them at its last meeting.

Inflation in the 21-nation currency area fell to 2.8% from 3.2% in May, the first decline since January, the European Union’s statistics agency Eurostat said Wednesday. A consensus of economists polled late last week by The Wall Street Journal expected consumer-price growth at 3.0%.

Energy prices were 1.7% cheaper in June than in May, the data showed, as oil prices declined throughout the month after tensions in the Middle East eased. Annual services inflation also cooled, suggesting that recently higher energy costs aren’t passing through significantly into other areas of the economy that could push up wages. Core inflation—which strips out more volatile energy and food prices—fell back to 2.4% in June from 2.6% in May.

“Inflation in the eurozone is falling—and falling significantly,” Stephanie Schoenwald, an economist at KfW Research said. “Provided the situation in the Middle East remains stable, the peak of the energy-driven price surge is now behind us.”

The print suggests the ECB won’t rush into another rate hike, allowing policymakers to wait for fresh macroeconomic forecasts at its meeting in September, when the impact of the Iran war on supply infrastructure could become clearer. The bank raised its key rate by a quarter-point to 2.25% in June.

“The data cements the now-consensus view that the ECB will hold fire this month,” Claus Vistesen, chief eurozone economist at Pantheon Macroeconomics, said in a note to clients.

“It would take a remarkable rally in oil prices to convince the governing council later this month that the outlook has shifted…sufficiently to justify a hike,” he added.

Nevertheless, ECB rate setters have in recent weeks been balancing the discomfort of inflation still above the bank’s 2% target alongside signs that the impact of the surge in energy prices is softening. Oil prices in the last week returned to prewar levels, after the tentative deal announced between the U.S. and Iran to halt fighting. Investors still expect at least one more rate hike before the end of the year, according to LSEG data.

At the ECB’s forum in Sintra, Portugal, on Monday, President Christine Lagarde reiterated that the bank’s rate rise at its meeting last month was based on forecasts that put inflation above target until 2028, rather than a pre-emptive “insurance hike.”

However, she contended that the central bank need not now “act with the same force” it used following the dramatic increases in energy prices in 2022-23 after Russia’s full-scale invasion of Ukraine. The ECB eventually raised rates to record highs to try to bring inflation under control.

Parts for iPhones to cost more owing to surging demand from AI companies.

Americans now think they need at least $1.25 million for retirement, a 20% increase from a year ago, according to a survey by Northwestern Mutual

GCC banks are expected to post strong profits in 2026, led by Al Rajhi Bank with forecast earnings growth of 13.6%, according to S&P Global Market Intelligence.

< 1 minThe top four lenders in the GCC are expected to report strong profits in 2026 despite the US and Iran struggling to end the war that has roiled the region’s economies, S&P Global Market Intelligence said in a report.

Saudi-based Al Rajhi Bank is expected to record the largest year-on-year profit rise among all six banks in 2026, at 13.6%, with earnings rising further in 2027 and 2028, the report said, citing Visible Alpha consensus estimates.

Visible Alpha fintech is a part of S&P Global Market Intelligence.

Saudi National Bank, Qatar National Bank and Abu Dhabi Commercial Bank are forecast to report higher profits. However, Emirates NBD Bank and First Abu Dhabi Bank (FAB) are expected to report low-single-digit profit declines, though earnings will still be above 2024 levels.

In 2027, all six banks are projected to report profit growth between 7% and 18%.

Although aggregate revenue growth is expected to slow in 2026, net interest income (NII)– the banks’ main revenue driver that is boosted by higher interest rates–will exceed 2025 levels, according to Visible Alpha estimates.

Total NIIs are expected to reach $47.56 billion in 2026, $51.42 billion in 2027 and $55.35 billion in 2028, compared to $42.82 billion in 2025, the report said.

The sports-car maker delivered 279,449 cars last year, down from 310,718 in 2024.

Interior designer Thomas Hamel on where it goes wrong in so many homes.

Millions of houses, thousands of jets, every NFL and NBA team—imagine the things a trillionaire could buy.

3 min

The initial public offering for SpaceX could make Elon Musk the world’s first trillionaire. Just how wealthy is the tech founder?

His fortune now stands at roughly $970 billion, mostly in stock, according to a Wall Street Journal analysis.

Accumulating that amount over his career averages out to $992 a second.

Musk’s wealth includes $538 billion for his pre-IPO stake in SpaceX, $167 billion for his stake in Tesla , and another $150 billion or so for stock options in those companies he could exercise just about any time, the Journal analysis found.

Then there is $5 billion apiece for The Boring Company, which drills tunnels, and Neuralink, the brain-implant firm he founded, and $104 billion in property, aircraft and other investments and assets as estimated by Altrata, a wealth-intelligence firm

He has made about $3.6 million an hour over 31 years

Musk is 54 years old and co-founded the first of his many U.S. tech- and engineering-oriented companies in 1995, 31 years ago. To amass $970 billion in that time meant accumulating roughly:

An American household earning the median U.S. income ($83,730 in 2024) would have to work more than 11 million years to make his wealth.

To be sure, the success of Tesla and SpaceX also has made billions of dollars for investors who bet on Musk and made millionaires of employees who got shares in the businesses.

Ingrid Robeyns, a philosopher and economist, has written that the wealth of the world’s richest has soared so much it is nearly incomprehensible for laypeople to grasp.

She recently estimated that Musk would make about $4.2 million an hour in his career, if he worked 70 hours a week without vacations until he is 75 years old.

Musk, of course, is known for sleeping on factory floors and rarely taking vacations. After buying Twitter, he has said, his work exploded to more than 120 hours a week from about 80 hours before.

Buy 2.4 million U.S. homes or 10,000 private jets

Most of Musk’s wealth is tied up in his companies. He famously said in 2020 that he would “own no house” and sold off several California properties, only to later buy homes in Texas.

Musk can borrow billions against his holdings in SpaceX and Tesla, but much of his wealth is on paper—not cash he can easily spend.

Here are some things a person with $970 billion could do with that amount of money:

$970 billion is bigger than the yearly output of most countries

Musk’s net worth eclipses the annual economic activity of more than 125 countries, including Norway, Thailand, Argentina and South Africa.

His self-made fortune, built on electric vehicles rocket ships and artificial-intelligence ambitions amounts to about 3% of U.S. gross domestic product today. On that basis, he easily surpasses John D. Rockefeller , the richest American who ever lived before Musk.

A century ago, Rockefeller rode the wave of industrialisation by building Standard Oil into a behemoth, wielding influence over railroads and pipelines. The monopoly was ultimately broken up by the federal government.

Rockefeller amassed a fortune of about $1.4 billion by 1937—roughly 1.5% of U.S. GDP at the time. Here is how that compares in terms of today’s economy:

This explanatory article may be periodically updated.

Sources: Altrata (Musk net worth excluding options; Bezos, Ellison and Zuckerberg net worth); Securities and Exchange Commission filings (Tesla and SpaceX stock options); Census via St. Louis Fed (2024 median U.S. annual household income, first-quarter 2026 median U.S. house sale price); Forbes (NFL and NBA team values); Liberty Jet (G700 operating costs); International Monetary Fund (2026 GDP by country); Harvard Business School case study (Rockefeller wealth) undefined Photos: Getty Images (Musk); Associated Press (Musk, Bezos, NBA, NFL); Reuters (Zuckerberg, Ellison); Bloomberg (homes, jet)

Following the successful launch of its Palais Collection, MAISON de SABRÉ has unveiled a new modular handbag system offering more than 720 styling combinations.

Following the devastation of recent flooding, experts are urging government intervention to drive the cessation of building in areas at risk.

The AI-driven chip rally still has room to run, according to analysts, with companies such as Nvidia, AMD, Broadcom, Taiwan Semiconductor, and Micron positioned to benefit from surging demand for AI infrastructure. While concerns over valuations and market exuberance persist, growing investment in AI data centers and the rise of AI agents are expected to support long-term growth across the semiconductor sector.

8 min

Chip stocks used to be the gritty part of the tech complex. In trading patterns and profit margins, they had more in common with cyclical commodities than software. But as with so many things, artificial intelligence changed everything. Almost overnight, chips became the accelerant for the technology—and the market.

Supply constraints compounded the excitement. During one stretch this spring, the PHLX Semiconductor Sector Index, or SOX, rose for 18 straight days, for a gain of 47%. The index is up 80% since March 30, leading to worries about a new dot-com-style bubble with chips looking like the 2026 version of fiberoptic stocks.

Indeed, the gains have been indiscriminate. While Nvidia is up 30%, low-margin chip makers like On Semiconductor and STMicroelectronics have each risen 122%.

These stocks trade at huge multiples of earnings, way above historical trends, while Nvidia looks cheap by any historical measure.

“The multiples cannot all be accurate,” Gavin Baker, chief investment officer of Atreides Management, says of the wide range of price/earnings ratios across the AI landscape. “You have memory makers at low- to mid-single-digit P/Es, you have Nvidia at a low P/E, you have other accelerator companies at reasonable multiples. And then most everything else—power, cooling, optical, and semi-cap equipment—are at dramatically higher multiples.”

The disconnect sets up an opportunity for investors. As the market corrects its math, the quality names should outperform. Investors should focus on Advanced Micro Devices, Broadcom, Taiwan Semiconductor Manufacturing, and, yes, $5 trillion Nvidia.

In the world of semiconductors, quality means having technological advantages that are durable and enable better products and high gross margins. Quality also means having nimble executives who can identify and react to changes in a fast-moving environment. Think Nvidia’s Jensen Huang and Broadcom’s Hock Tan. The quality focus becomes more important as subsidized Chinese manufacturers increase the supply of chips made using older technologies.

All indications point to accelerating demand for AI computing. This year, the five so-called hyperscalers— Microsoft, Amazon.com, Google parent Alphabet, Meta Platforms, and Oracle —could combine to spend over three-quarters of a trillion dollars on AI data centers.

Even after its massive expenditures, Microsoft recently said its cloud-computing capacity was so constrained that it had to forsake external cloud sales to run its own operations.

But the demand trend is shifting, and investors need to pay attention to the nuances.

Early in the AI boom, growth was tied to training new models, a slow, resource-intensive process. Now workloads are moving toward running those models, a process known as inference.

The inference trend is being supercharged by the rise of AI agents, software that can use AI models to complete a complex series of tasks from a simple conversational prompt. Agents chew through computing at a rate no person could match. If predictions are correct, it won’t be too long before they outnumber humans on enterprise networks.

Nvidia already won the battle for training, but inference opens the door to new competition. Moreover, agents are software and run on traditional server central processing units, or CPUs, which should also see increasing demand in the coming years.

Even AI can’t change the fundamentally cyclical nature of semiconductors, but it can—and will—lengthen the cycle. Right now, anyone close to the AI supply chain will tell you that the industry is nowhere close to satisfying demand. That’s why Micron Technology has seen its forward P/E multiple expand from an industrial-like single-digit figure. It’s still undervalued. So are the shares of Nvidia, AMD, Broadcom, and Taiwan Semi.

Relative to expected earnings growth over the next two years, all five stocks trade at a PEG, or price-to-earnings growth ratio, of less than 0.6 times. By comparison, the S&P 500 index fetches a two-year PEG of 1.

All five companies are pillars of the new economy—ones that have lasting value and staying power, even as the momentum inevitably fades from the broader chip trade.

The Leader

Nvidia has been developing hardware and software tools for AI computing for nearly two decades, giving it the pole position when generative AI caught fire. Adjusted earnings per share have grown from 33 cents in fiscal 2023 to $4.77 in fiscal 2026, which ended in January. Over the next two years—a critical period in the AI transition—Wall Street analysts expect Nvidia’s EPS to hit $12.37, giving the stock a P/E of 17 times.

Nvidia’s graphics processing unit chips, or GPUs, are the workhorses of AI computing, and they’re the company’s main source of sales. Just as important, though, is the company’s two-decade focus on AI bottlenecks.

The sports-car maker delivered 279,449 cars last year, down from 310,718 in 2024.

With US$40 million already committed, the Global Talent Fund is attracting investor attention with a strategy focused on building globally scalable consumer brands alongside high-profile talent.

2 min

A new investment fund targeting celebrity-founded consumer brands has secured US$40 million in commitments and is rapidly approaching its US$50 million fundraising target, signalling growing investor appetite for alternative opportunities beyond traditional asset classes.

The Global Talent Fund, which has a maximum raise of US$100 million, focuses on building and investing in consumer businesses alongside celebrities, athletes, and influential personalities who play an active role as co-founders rather than simply endorsing products.

The strategy is based on the belief that changes in consumer behaviour, particularly the rise of social media and digital engagement, have fundamentally altered how brands are built and scaled.

GTF founding partner Jeremy Hunt, who is helping lead the fund\’s strategy, said consumers increasingly feel connected to personalities they follow online and are more willing to support products developed by those individuals.

\”Consumers are searching for content to engage with, and when a celebrity they like or follow takes them on the journey of creating a product or brand, they genuinely feel part of that process,\” he said.

The fund is targeting high-growth consumer sectors including wellness, hydration, beauty and recovery, areas Hunt believes continue to benefit from strong global demand and ongoing innovation.

Rather than backing celebrity endorsement deals, the fund is seeking businesses where talent is deeply involved in product development, brand creation and long-term growth.

According to Hunt, authenticity remains one of the biggest differentiators between successful celebrity-backed brands and those that fail.

\”The consumer can see clearly if someone is simply being paid to promote a product,\” he said. \”The winners are typically the brands where the celebrity has genuinely helped build the business from the ground up.\”

The model has attracted support from several prominent Australian investors and business families, reflecting broader interest in alternative investments with global growth potential.

Hunt said consumer brands offered a level of tangibility that many investors found appealing.

\”Consumer brands are what we touch, feel, smell and taste every day,\” he said. \”Our investors understand the growth potential in the model, but they also want to be part of the journey.\”

The fund\’s rapid progress towards its fundraising target comes amid growing recognition that celebrity influence, when combined with strong commercial execution and scalable business models, can create significant enterprise value.

With several high-profile celebrity-founded businesses generating billion-dollar exits in recent years, supporters of the strategy believe the opportunity remains in its early stages.

Following the successful launch of its Palais Collection, MAISON de SABRÉ has unveiled a new modular handbag system offering more than 720 styling combinations.

Major U.S. banks remain upbeat about second-quarter performance despite geopolitical tensions, higher fuel prices, and ongoing disruptions in the Strait of Hormuz. Strong trading, investment banking, lending activity, and rising AI-related investment are helping drive revenue growth, while resilient consumer spending continues to support the sector.

2 min

Big banks’ profit engines are humming along even as geopolitics keep threatening to gum up the works.

Several of the nation’s largest lenders this week gave investors updates on how their businesses have fared in the second quarter, and the consensus was overwhelmingly positive.

That is despite blockages in the Strait of Hormuz continuing during the period, and a succession of false starts on Iran peace talks that have whipsawed markets. Higher gasoline prices have started to seep into other parts of the economy, and consumer sentiment has reached all-time lows.

But from where banks sit, dealmaking, trading and lending appear to all be going as planned.

“It’s gung ho,” said JPMorgan Chase Chief Executive Jamie Dimon. “There’s a lot of exuberance out there.”

Dimon said his bank might even slightly outperform the 11% and 10% increase in markets and investment-banking revenue, respectively, that analysts are expecting for the current quarter. Guidance for net interest income, a measure of profit in a bank’s core lending business, is unchanged for the bank, Dimon said.

Wall Street has been raking in bigger profits under President Trump, with uncertainty over his tariffs and other policies driving up market volatility and revenue on trading desks. Dealmaking has also sprung back to life, generating more fees for investment-banking divisions.

Banks are also benefiting from the mad dash by companies to invest in infrastructure and technology related to artificial intelligence, executives said.

Goldman Sachs President John Waldron told investors that merger-and-acquisition volume was on track to be near or break the record set in 2021, and that the volume of initial public offerings was up about 80% so far this year. Waldron added Goldman was working on large infrastructure financings that would rank among the biggest transactions involving the bank.

Wall Street has been fixated on the coming IPO of Elon Musk’s SpaceX, which is expected to generate hundreds of millions in fees with a valuation north of $1.5 trillion. Also on the horizon are public-market debuts for artificial-intelligence behemoths Anthropic and OpenAI, at similarly eye-catching valuations.

Consumer spending appears to be holding up, too, despite souring sentiment.

Bank of America CEO Brian Moynihan said his bank is seeing consumers continuing to spend, including on travel and restaurants, despite dealing with higher gas prices. He said the company expects second-quarter sales and trading revenue to be up about 15% from the same quarter last year.

“Things are still extremely, extremely strong,” said Wells Fargo CEO Charlie Scharf, referring to consumers. “It’s really hard to find pockets of weakness in the actual results, put aside surveys of how people are feeling for a second.”

Scharf said loan growth was outperforming expectations from the start of the year. Wells Fargo’s markets and investment-banking revenue were both expected to increase by percentages in the midteens from a year earlier, he said.

Paine Schwartz joins BERO as a new investor as the year-old company seeks to triple sales.

Fitch Ratings warned that ongoing regional conflict are increasing pressure on Middle East credit ratings, disrupting supply chains and raising economic risks across the GCC. While no issuer downgrades have been recorded so far, several ratings have been placed on negative watch regarding several sectors.

< 1 min

The war and effective closure of the Strait of Hormuz have disrupted economic activity, but the negative rating actions for Middle East issuers for the March-April period were limited to outlook revisions and placements on the Rating Watch, stated a new report from Fitch Ratings.

The Middle East has been subject to heightened uncertainty and disruption since end-February, due largely to the war. There have been no Middle East issuer downgrades since end-February, but Fitch has placed several ratings on Rating Watch Negative and revised some Outlooks to Negative from Stable, or to Stable from Positive.

These actions point to the persistence of significant risks around the war that, if crystallized, could lead to broader rating downgrades.

The effective closure of Hormuz has led to supply chain disruptions. These have been exacerbated by damage to Qatar’s LNG infrastructure and volatile funding conditions in the region, said Fitch in its statement.

Fitch recently revised its 2026 base-case brent oil price assumption to $87/barrel. This is now based on an assumption that the strait will begin reopening around July, extending the closure to about five months, from one to two months expected previously.

Oil prices average about $100/barrel in 2026 under Fitch’s adverse scenario, with Hormuz not returning to near normal flows until later in Q3 or possibly early Q4. The scenario highlighted material risks to several sectors in the Gulf Cooperation Council (GCC), including airlines, hotels, chemicals and homebuilders.

The ability of hydrocarbon producers to increase revenue and margins due to higher prices is conditional on their independence from Hormuz.

The ratings of 85% of GCC banks and of many corporate government-related entities in the region rely on sovereign support. These ratings are therefore likely to move in tandem with the Issuer Default Ratings of the relevant sovereigns.

New research suggests that bonuses make employees feel more like a mere cog in a wheel.

Qatar Investment Authority (QIA) has joined as an anchor investor in the capital increase of Greece’s Public Power Corporation (PPC), reinforcing its strategy of investing in long-term infrastructure and energy transition opportunities. The oversubscribed offering raised €4.25 billion and supports PPC’s expansion across renewable energy, grid modernization, and data center development in Southeastern Europe.

< 1 min

Qatar Investment Authority (QIA) announced Monday its participation as an anchor investor in the share capital increase of Public Power Corporation S.A. (PPC), the leading integrated energy group across the broader Southeastern Europe, listed on the Athens Stock Exchange.

The offering was multiple times oversubscribed, raising 4.25 billion euro from primary shares and an additional 250 million euro through a secondary placement of treasury shares, priced at 18.63 euro per share.

The share capital increase was supported by cornerstone investments from the Greek state, which subscribed for approximately 1.3 billion euro, and Aeolus Holdings S.a r.l., an entity owned by funds advised by CVC Advisers Greece S.M.S.A. and/or its affiliates, which subscribed for approximately 1.2 billion euro.

The new shares, each with a nominal value of 2.48 euro, attracted significant demand from a number of global, long-term institutional investors as well as K Group Capital Partners, the private equity fund controlled by the Kyriakou family, which has QIA as a strategic partner and focuses on investment activities in Greece.

QIA and K Group Capital Partners, discussed the opportunity for this investment during the recently held Europe Gulf Forum in Greece.

QIA’s participation reflects its strategy of deploying patient, long-term capital into essential infrastructure and businesses well-positioned to benefit from structural trends, including the global energy transition.

As a strategic platform at the forefront of Greece’s energy transition, energy security and infrastructure modernization, PPC is uniquely positioned to lead the energy transition in Southeastern Europe through targeted investments in renewables, flexible generation, distribution network modernization, and data center development.

The investment also reinforces QIA’s broader commitment to Greece as well as expanding the collaboration with K Group Capital Partners.

New research suggests that bonuses make employees feel more like a mere cog in a wheel.

Stablecoins are increasingly being positioned as the future of digital payments, promising faster and more efficient transactions than traditional banking systems. But as governments move to regulate the sector and bring crypto further into the mainstream, concerns remain over financial stability, market fragmentation, and the risks tied to privately issued digital money. With adoption growing globally, the debate is shifting from whether stablecoins will survive to how they can be integrated safely into the broader financial system.

4 min

“Private money” sounds like an oxymoron. Surely the currency on which our economy runs is the epitome of a public good?

In fact, the U.S. has had private money before, in the 1800s. And private money is now making a comeback, in the form of stablecoins: cryptocurrencies intended to maintain a fixed value against the dollar.

To proponents, stablecoins are crypto’s killer app. They will make payments faster and more efficient, especially across borders, than the legacy banking system makes possible.

With that promise, though, comes the risk that this could lead to a financial crisis, much like some past experiments with private money.

Both the Genius Act, signed into law last year, and the Clarity Act now making its way through the Senate, aim to make stablecoins safer and more mainstream. But no legislation can fully remove risk that is intrinsic to the design of stablecoins.

Stablecoin issuers and affiliated platforms are private enterprises driven to increase usage and profit via the assets they hold to back their coins, the “rewards” they pay to users, and the sorts of activity they tolerate.

Of course, profit and risk-taking are core to how all innovation happens, and that’s a good thing. In finance, though, innovation routinely leads to excesses that can lead to a sudden loss of confidence, runs and contagion that spills over to the broader economy.

What is money?

Money serves several purposes: a store of value, a unit in which to price transactions, and a medium to carry out those transactions. U.S. dollars meet all these criteria. Today, the Federal Reserve controls the issuance of dollars.

But nothing bars private actors from trying to create their own versions of money. Crypto long aspired to be just that. But the first cryptocurrencies such as bitcoin weren’t backed by anything, and thus their value fluctuated wildly.

Stablecoins back themselves with tangible assets such as Treasury bills that can be sold to redeem coins one for one for dollars. CoinMarketCap puts stablecoins outstanding at roughly $300 billion, led by Tether ($190 billion) and Circle ($76 billion).

Stablecoins promised the best of both public and private money: as interchangeable and reliable as dollars but, thanks to the blockchain, faster and cheaper than the dollar-based banking system.

But that promise embodies a contradiction. “Stablecoins attempt to import credibility from public money while operating outside the established settlement system,” Pablo Hernández de Cos, general manager of the Bank for International Settlements, noted in a recent speech.

An essential quality of money is “singleness,” meaning a dollar must always equal a dollar no matter when, where or with whom it is used. Bank deposits are a form of private money, but because banks can borrow from the Federal Reserve to redeem deposits, and dollars move between banks via the Fed, their dollars exhibit singleness.

By contrast stablecoins move through proprietary, fragmented infrastructures. They don’t exhibit singleness. Though coins issued by Tether and Circle are intended to stay fixed to the U.S. dollar, they often deviate from that value, albeit usually by tiny amounts.

Unlike the Fed, stablecoins seek to make a profit. One way is by expanding usage, such as by paying interest, as bank deposits do. The Clarity Act would prohibit payment of deposit-like interest, but permit rewards based on usage.

Historically, crypto has pushed the legal envelope, and may design rewards to mimic interest without violating the law. “I don’t see any reason they’d completely change their tactics and become conservative about interpreting the law when that has not been the pattern thus far,” said Molly White, who writes the Citation Needed newsletter on crypto and technology policy.

Stablecoins also have an incentive to “reach for yield,” that is to back their coins with slightly riskier or less liquid assets with higher returns. But if those assets’ value declines, stablecoins may not be able to maintain par value. Holders could rush to sell or redeem, triggering forced sales of the assets and spillover to other markets, even banks.

Last year’s Genius Act requires stablecoins that cater to Americans be backed with safe, liquid assets such as treasury bills and bank deposits. But Fed governor Michael Barr noted last year the law has loopholes. The bank deposits may be uninsured. The law allows stablecoins to receive money, including foreign money, through “repo” loans, and that could include bitcoin, which El Salvador recognizes as money, Barr noted.

And the law doesn’t cover coins that operate outside the U.S. such as Tether’s main coin, dubbed USDT, though Tether has launched a compliant U.S. coin, USAT.

We’ve been here before

During the free banking era from 1837 to 1863, banks could issue their own currency. But the system was inefficient, with currency values that fluctuated against each other.

“All states maintained a range of requirements for banks to collateralize their notes, but many proved ineffective; fraud was widespread, and the system was fragmented—banknotes of one bank were often not accepted by other banks outside the local area; bank failures were widespread,” the Andersen Institute for Finance and Economics writes in a report on stablecoins. Nonbanks, such as railroad companies, issued their own currency.

Money-market funds are a type of private money, promising to redeem shares at a dollar each, on demand. But during the global financial crisis, one fund couldn’t honor that value—it “broke the buck”—because it held devalued assets. A broader panic ensued.

Those cases showed how a loss of confidence can cause the volume of private money to contract, amplifying economic stress. Fabio Natalucci, chief executive of the Andersen Institute, notes that is the opposite of public money, which is “elastic”: The Fed expands its supply at times of stress.

Stablecoins are here to stay

Stablecoins are a natural evolution of payments technology, so it makes sense to find a way to integrate them into the economy. That’s what the Genius and Clarity acts attempt to do, which stablecoin advocates hope will encourage adoption.

That really hasn’t panned out yet, though. Japan boasts a “carefully designed regulatory framework” for crypto, but yen-based stablecoins’ market cap is less than 0.01% of dollar coins’, Hernández de Cos noted.

The vast majority of stablecoins are linked to the dollar, and those are largely held outside the U.S., often as a means of skirting laws or capital controls. Stablecoins account for 84% of illicit crypto activity such as sanctions evasion and money laundering, according to Chainalysis. Trading crypto remains the primary use of stablecoins. Today, less than 1% of stablecoin usage is for real-economy payments, a Kansas City Fed study concluded.

Meanwhile, banks are beginning to offer an alternative: “tokenized deposits,” which they think offer the “singleness” of dollars with the benefits of the blockchain.

Banks, of course, have caused their share of crises, which is why over time they became so tightly regulated and integrated with the Fed. Stablecoins may have to follow the same path.

Many of the most-important events have slipped from our collective memories. But their impacts live on.

EFG Holding reported strong revenue growth during Q1 2026, with revenues rising 18% year-on-year to EGP 6.6 billion, supported by solid performance across investment banking, non-bank financial services, and commercial banking operations. The group also recorded strong momentum in treasury and capital markets activity, while subsidiaries including Valu and Bank NXT delivered notable growth in revenues and profitability despite rising operating costs.

< 1 min

EFG Holding, Cairo-based financial services group, recorded revenues of EGP 6.6 billion ($124.8 million) for the three months ending March 31, 2026, up 18% YoY

Growth was supported by solid performance across its investment banking, non-bank financial services, and commercial banking businesses. Operating profit rose to EGP 2.5 billion, increasing 20% YoY (+37% QoQ), with an operating margin of 38%.

However, net profit fell to EGP 1.0 billion, down 14% YoY. The strong performance was mainly driven by treasury and capital markets activity. Revenues from this segment jumped 84% YoY, helped by foreign exchange gains after the Egyptian pound weakened by about 14% in March.

The investment banking division reported revenues of EGP 3.1 billion, rising 9% YoY. Brokerage activity improved, with revenues increasing 4% YoY to EGP 1.6 billion, while asset management and private equity posted steady growth.

EFG Finance, the group’s non-bank financial arm, reported revenues of EGP 1.6 billion, up 20% YoY. This growth was mainly driven by Valu, the consumer finance platform, where revenues surged 85% YoY to EGP 895 million.

Bank NXT, the group’s commercial banking unit, delivered strong results, with revenues reaching EGP 1.9 billion, up 34% YoY. Net profit at the bank rose 39% YoY to EGP 691 million, supported by strong loan growth. The bank’s loan portfolio increased 52% YoY, while deposits grew 22% YoY, keeping the loan-to-deposit ratio at 63%.

At the same time, costs continued to rise. Operating expenses increased to EGP 4.1 billion, up 16% YoY (-33% QoQ).

The sports-car maker delivered 279,449 cars last year, down from 310,718 in 2024.

Qatar continued to strengthen its position as a regional hub for investment and business after attracting more than 3,290 non-Qatari companies during Q1 2026, marking a 66% increase compared to the same period last year. The country also recorded growth in new commercial registrations, patents, and trademark activity, reflecting rising confidence in Qatar’s economy and its business environment focused on innovation, expansion, and long-term growth.

2 min

Qatar attracted more than 3,290 non-Qatari companies during the first quarter (Q1) of 2026, reflecting growing international confidence in the country’s investment environment and economic outlook.

In a post on its X platform, the Ministry of Commerce and Industry (MoCI) released the new data showing strong growth across foreign investment commercial registrations, and intellectual property indicators.

Foreign investment saw substantial growth during the quarter. The post revealed a total of 3,295 non-Qatari companies established operations in the country during Q1 2026, reflecting a 66% increase compared to the first quarter of 2025.

The strong increase in foreign company registrations highlights Qatar’s continued efforts to position itself as a leading regional hub for trade, investment, and commercial expansion.

Qatar’s modern infrastructure, strategic geographic location, and policies are aimed at facilitating international investment and commercial partnerships.

Meanwhile the info graphic shared with the post revealed the new commercial registrations surged by 18.5% to 6,328 in Q1 this year compared to the last year. The Commercial Affairs Sector demonstrated significant progress across its key performance indicators.

The rise reflects growing entrepreneurial activity and increasing confidence in Qatar’s business environment. It also highlights the country’s continued efforts to strengthen the investment climate and support private-sector growth.

The info grapic also showed notable progress in intellectual property protection, an area considered essential for encouraging innovation and attracting investors. A total of 43 copyrights were granted during the quarter, marking a 16% increase compared to Q1 2025.

Trademark registrations also remained strong, with 1,661 trademarks granted during Q1.

One of the most significant increase was recorded in the patents sector. The ministry reported that 145 patents were granted during Q1 2026, representing a remarkable 134% increase over the same period last year. The surge points to growing investment in research, technology, and innovation-driven industries.

The figures send a positive signal about the resilience and competitiveness of Qatar’s economy amid ongoing global economic shifts. With momentum building across multiple sectors, Qatar’s commercial and investment activity will remain strong throughout the remainder of the year.

Many of the most-important events have slipped from our collective memories. But their impacts live on.