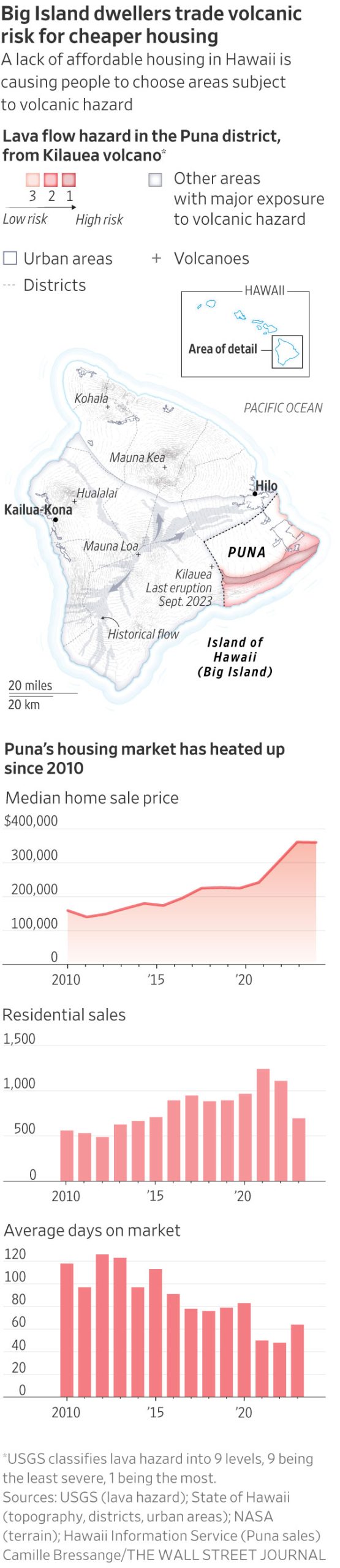

NOT EVEN MOLTEN LAVA CAN COOL THIS HOT HOUSING MARKET

The eastern section of Hawaii’s Big Island continues to attract home buyers searching for a cheap piece of paradise

5 min

5 min

PUNA, Hawaii—In 2018, a large volcanic eruption spewed lava, rock and ash into the middle of a subdivision here, gobbling up more than 700 homes and displacing thousands of residents in a slow-motion disaster. Today, it is Hawaii’s fastest-growing region.

Land in an active lava zone, it turns out, is relatively cheap. Lured by a shot at attainable homeownership in paradise, island dwellers and mainland transplants alike have been flocking to this area in the shadow of Kilauea, driving up prices in the Puna District. Still, the area remains one of the last affordable refuges on the cheapest island in Hawaii, America’s most expensive state.

“In terms of the last bastion of affordability, Puna is it,” said Jared C. Gates, a Realtor who was raised on Oahu and came to the Big Island for college in the 1990s. He purchased his first home in 2005, a modest fixer-upper in Puna, on his salary as a waiter.

Over the past few years, he has been getting more business in Leilani Estates, the neighborhood where the 2018 eruption began.

None of the homes that were inundated by lava have been rebuilt. Many homeowners have sold their properties to Neighbours or the county in a federally funded buyback program, but that land remains vacant for now. The land has been so transformed that it is hard for remaining owners to know even where their property begins and ends.

“It took out roughly a third of the subdivision; totally surreal,” Gates said last fall. “And houses are selling there again.”

Among Gates’s listings that day was a three-bedroom, two-bath home with lush landscaping, two blocks from the mile-wide lava field where heat and steam still radiate from vents in the petrified landscape. “It’s a beaut,” he said. “It will sell.”

Three weeks later it did, for $325,000, cash.

The story of how serene-looking slices of suburbia came to inhabit an active volcanic rift zone is well-known here. In the 1960s, land speculators—aided by a new county government hungry for tax revenue—bought thousands of acres and carved it into lots of an acre or more that were snapped up by investors.

There were virtually no requirements that developers pave roads, place utility lines or build other essential infrastructure. To this day, there is no wastewater treatment plant or hospital. Many of the district’s 51,000 residents rely on filtered rainwater and cesspools to dispose of sewage.

Early buyers included Native Hawaiians looking for an affordable place to call home and mainland hippies intent on off-grid living. As home prices rose in Hawaii and across the nation, however, more working families and mainland retirees went hunting for deals on the Big Island.

County Councilwoman Ashley Kierkiewicz, who represents Puna, said rush-hour traffic on the rural, two-lane highway that connects Puna to Hilo, the county seat roughly 20 miles away, is so bad that she leaves her home 1.5 hours early to get to work.

County officials say rules tied to federal funding bar local government from building affordable housing in lava zones 1 and 2, which are the riskiest and make up most of lower Puna. State law also prohibits them from spending most local money on private subdivisions, meaning that roads are largely maintained by owner associations.

Hawaii County Mayor Mitch Roth said that while the county has added a new firehouse, police station and park facilities there in recent years, the county has limited funds to make major investments in high-risk areas.

“Are we going to invest public money in a high-risk place…knowing that whatever you build could be taken out by lava at any time?” said Roth.

The lack of some modern conveniences has scarcely slowed the flow of newcomers.

Like many places in the U.S., an influx of remote workers during the pandemic has helped send the housing market here into overdrive.

Among the recent arrivals are David Booth and his partner, Juan Polanco. The former Phoenix residents had been brainstorming tropical locations where they could slash their living expenses and ease into retirement.

“The attraction to the Big Island was affordability,” said Booth, 61, who now works remotely. He and Polanco, 59, paid cash for a 1,500-square-foot home that had been split into three units with separate entrances. “You can’t have this on any other island for this price point.”

The property sits on a 1-acre lot in Hawaiian Paradise Park, a subdivision located in the less-risky lava zone 3. Homes with repeated sales in the neighborhood have seen a nearly 800% appreciation in price since 2000, according to data from the University of Hawaii Economic Research Organization.

Properties in lava zones 1 and 2—some with sweeping oceanfront views—were far cheaper, Booth said. In the end, the risk of losing their nest egg to a natural disaster, and the difference in insurance rates, were deal breakers.

They are getting used to bringing in their drinking water and dealing with vicious fire ants. The slow-paced lifestyle and prospect of early retirement are worth it, he said.

They have listed the two other units as vacation rentals, and their first guests arrive next week.

“We are overwhelmed with the amount of beauty here and just how much more relaxed we feel,” said Booth. “We’re building a whole new life here.”

Three years ago, Travis Edwards, 48, was driving delivery trucks and living with his mother in Southern California’s Inland Empire.

He was sick of the traffic, wildfires and car thefts, he said. Upon retiring, his mother sold her house and paid cash for a 1-acre lot with two units in Leilani Estates, surrounded by avocado and citrus trees. Lava insurance rates in lava zone 1, the riskiest area that encompasses the entire subdivision, were so high that they simply stopped paying for it, he said.

He mostly shrugs off the dangers, reasoning that they would be reckoning with fires and earthquakes on top of a lower quality of life back in Southern California.

“It’s just paradise,” said Edwards, who now drives limousines part-time. “The rest of the world doesn’t exist when you’re here.”

Rising prices on the east side have left Puna native Chantel Takabayashi feeling stuck. A single mother of three, she works 16 hours a day as a state prison guard in Hilo. She would like to buy a home closer to work and better schools but has been priced out of most neighborhoods she has considered.

“I make pretty decent money and I work long, endless hours, and I still can’t afford better housing,” she said.

Liz Fusco, who manages more than 100 rental properties for Hilo Bay Realty in Pahoa, said that during the pandemic, she saw three-bedroom homes in parts of Puna that once fetched $1,500 a month rent for as much as $2,300.

Most of the applicants were mainlanders, she said, with stellar rental histories, plenty of income and pristine credit. Units that would typically take more than a month to rent were getting leased in three days.

Tina Garber, who has lived in the Puna area for 21 years, has been displaced twice in the past 18 months after the homes she was renting went up for sale.

Currently, she is paying $750 a month—three-quarters of her monthly income as a housecleaner—for a 400-square-foot studio surrounded on three sides by cooled lava. Her landlord just told her it will be listed for sale in April.

“People that come over here with money, they do not realize that it is so hard to make it here,” Garber said. “They think, ‘Oh, a good deal in Hawaii.’ But it puts a lot of pain and suffering on local folks.”

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Meta is facing one of the biggest legal challenges in its history, with thousands of lawsuits over the safety of young users as it ramps up investment in artificial intelligence. The company could face billions of dollars in damages and mounting pressure to make significant changes to its platforms.

Automobili Lamborghini has named Francesco Milicia as its new Marketing Director, effective September 1, 2026. Joining from Ducati, Milicia will lead the brand’s global marketing strategy and strengthen Lamborghini’s position across international markets.

Alphabet and Tesla kick off this week’s earnings season, with investors closely watching whether heavy AI spending is delivering sustainable returns. Analysts say the results will offer fresh insight into the future of AI investment, cloud growth, and Tesla’s long-term strategy beyond electric vehicles.

Artificial intelligence is making it easier than ever to build a business without building a team. As AI takes over coding, customer support, marketing, administration, and other day-to-day tasks, a growing number of solo founders are scaling startups to millions in revenue with few—or even no—employees. While the trend is lowering barriers to entrepreneurship, it is also reshaping hiring, raising questions about the future of work and how businesses will grow in the AI era.

5 min

Ben Broca launched a company last December that offers AI tools to entrepreneurs. He’s already added 10,000 paying customers and is on track to bring in $10 million in revenue this year.

One thing he hasn’t added: any other employees.

The 40-year-old is part of a class of entrepreneurs who are launching, and then often running, new companies on their own. Artificial intelligence tools answer Broca’s emails, help write and debug code, field requests from customers, sign up new subscribers and grant refunds when issues arise.

Broca relishes his ability to make whatever decisions he wants on his own, often from his sun-drenched Sausalito, Calif., living room. “I think compromises make lukewarm results,” he said.

Once upon a time, running a business of a certain size required a team. AI is turning that assumption upside down, and more aspiring entrepreneurs are going it alone.

An analysis by the payments company Stripe shows there are thousands of solo operators on the company’s platform that are generating over $1 million in revenue, with their ranks doubling between 2023 and 2025. The number of solo operators crossing the $10 million threshold nearly tripled in that same span.

In the past, people without business contacts or particular savvy might not have known how to get their ideas off the ground, said Ernie Tedeschi, Stripe’s chief economist. “Now, AI can be a built-in business partner,” he said.

AI’s ability to handle various administrative tasks makes it potentially useful for launching solo businesses in many fields. But the technology’s ability to also handle key tasks in tech, like coding, make that field a particular hot spot.

Analyzing Census Bureau data, Bank of America Institute economist Taylor Bowley found that among all industries, new business applications in the information sector have seen the biggest percentage increase—nearly 45%—over the past year. At the same time, the rate of information-sector applicants saying they plan to hire workers has experienced the sharpest decline of any measured industry.

This Census dataset doesn’t track solo-operated businesses. But the numbers broadly show—in tech and beyond—that applications are flat among businesses likely to hire workers, but generally rising elsewhere. Economists say that’s a strong sign that solo operators are on the upswing.

“The bar for getting started has never been lower,” said Julian Weisser, who runs a San Francisco-based accelerator for solo founders working in tech. The accelerator—which offers founders seed money and mentorship in exchange for an equity stake—attracted 4,500 applicants for 10 slots made available in its most recent cycle, nearly five times the number it drew when it launched last May.

Going it alone with AI can still be surprisingly expensive. Broca said he was losing money on many customers’ accounts while paying to access Anthropic’s Claude to run his clients’ requests—that AI company, as well as others, charges based on usage. He has since switched to free open-source AI models from China.

Broca said he has raised $30 million from investors and, at the same time, has saved millions in salary since he hasn’t needed a team of software engineers.

Another risk: If it’s easy for one entrepreneur to launch an AI-assisted business, copying them can be easy, too. This creates anxiety for founders like Troy Johnston, who runs an AI-assisted business alone in Orlando, Fla.

“Everybody has the sword and we all have the ability to unsheathe Excalibur now,” said Johnston, 40, who used AI to code an app that helps people get the most out of credit card benefits. The company makes around $3,000 a month in profit, with no employees, and is continuing to grow.

What one-person businesses will mean for the labor market remains to be seen. Polling has shown Americans are worried that AI will replace jobs, and top economists are wrestling with that possibility, too. But AI is also creating lots of new jobs, and the go-it-alone entrepreneurs show how the technology can both open doors and limit employment opportunities.

“If everyone’s hiring less, but you get four times more firms, what does that do to head count?” said Rembrand Koning, an associate professor at Harvard Business School who studies entrepreneurship. He co-authored a recent study that found that among 50,000 startups the researchers examined, those focused on AI tended to operate with 25% fewer employees.

Koning also believes a soft hiring environment that’s left some people mired in long job searches has encouraged more to try their hand at launching businesses.

Some founders cite different motives. “It’s a perfect storm of post-pandemic burnout and a re-evaluation of one’s priorities, and also booming AI and a sense of what’s possible,” said Samir Ahmad, 39, who lives in Breinigsville, Pa.

Two years ago, Ahmad decided to leave the corporate job he had worked at Verizon for almost two decades to start a solo coaching and consulting business. He had been seeing social-media posts touting the ease and virtues of AI, which he used to chart a business plan and help with marketing. “It was like my chief of staff, a second in command,” he said.

The business ultimately petered out within months, though, and Ahmad is now back to a full-time corporate role with a utility company.

For Claire Vo, 41, AI helped her turn a passing impulse into a business. She was working full-time as a tech executive when she tapped AI in late 2023 to help code an app that would help her manage documentation and design for new products, with customers ranging from financial services to healthcare firms.

“I was copying and pasting from ChatGPT,” said Vo, who lives in San Francisco.

She put the app online for $1 a month, and within weeks people downloaded it thousands of times. Nearly three years later, Vo’s company—which she ran solo for nine months before hiring an engineer—now has 100,000 users and is on track to make seven figures in profit this year. AI handles the company’s marketing, sales and customer support.

While AI is a shortcut, Vo said her network and credibility in the industry were key. “I think people over-index on how easy AI is and under-index on how much I did to get to this point,” she said.

Many of the most-important events have slipped from our collective memories. But their impacts live on.

New research suggests that bonuses make employees feel more like a mere cog in a wheel.

2 min

2 min

Dubai’s property market has become too large to describe with a single number.

On one side sits the city’s vast off-plan machine: new launches, staged payment plans and buyers committing capital years before handover. On the other is the ready market, where completed apartments and villas can be occupied, leased and valued against a visible trading history.

Both are moving. They are not necessarily moving in the same way.

Gulf Today reported on July 24 that Dubai recorded 87,800 real-estate transactions worth AED291.7 billion during the first half of 2026. Citing analysis released by developer MERED, it said off-plan property represented 71 per cent of transactions, while average property prices increased 9 per cent over the half.

Those figures present the familiar Dubai story: buyers remain prepared to enter early, developers continue to bring major projects to market and confidence in the city’s longer-term growth has not disappeared.

Yet a daily market review published the same day by Wakhan Properties provides a useful counterweight.

Using Dubai Land Department data for transactions registered on July 23, Wakhan reported AED913.72 million in total deal value. Ready property accounted for AED505.13 million, or 55.3 per cent, while off-plan sales contributed AED408.59 million, or 44.7 per cent.

One day does not overturn a half-year trend. It does, however, show why transaction count and transaction value should not be treated as interchangeable.

Off-plan apartments can generate enormous volume because the entry price is lower, payment is spread across construction and developers release inventory in concentrated campaigns. Completed homes can produce fewer transactions but greater value, particularly when larger apartments and villas change hands.

The strongest common thread is the apartment market. Wakhan said apartments generated AED740.11 million across the ready and off-plan segments on July 23, equal to 81 per cent of total value. Villas were a secondary contributor, while commercial property and hotel apartments represented relatively modest shares.

For investors, that concentration matters. A market can be liquid in aggregate while behaving very differently by location, developer, completion status and price bracket.

There is also a discrepancy worth acknowledging. Other recent analyses based on Dubai Land Department records have produced different first-half totals, depending on whether they count all real estate, residential sales only, registrations or completed transactions. Projectory, for example, reported 79,698 residential sales worth AED227.1 billion, while other market summaries have placed total sales closer to 86,000 transactions and AED286 billion.

That does not make the market story less compelling. It makes definitions more important.

The more useful conclusion is that Dubai is not choosing between off-plan and ready property. It is supporting two sizeable markets at once.

Off-plan remains the engine of transaction volume and the clearest expression of confidence in future supply. Ready property provides immediate utility, visible rental evidence and a clearer basis for comparison. In a mature market, buyers need to understand the difference before being impressed by the headline.

Two coming 2027 models – the first of the “Neue Klasse” cars coming to the U.S. early next year – have been revealed.

Parts for iPhones to cost more owing to surging demand from AI companies.

The Lighting Innovation Summit returns to Abu Dhabi for its 2nd Edition. Following a successful inaugural edition, the summit is back to bring together lighting designers, architects, consultants, engineers, developers, government authorities, and technology providers for another day of insightful discussions, networking, and innovation. Co-located with the Modern Buildings Summit, attendees will benefit from access to a broader community of built environment professionals and decision-makers.

< 1 min

Following the success of its inaugural edition, the 2nd Lighting Innovation Summit Abu Dhabi will return on 9 September 2026, bringing together lighting professionals, architects, consultants, developers, technology leaders, and industry experts to discuss the innovations and trends shaping the future of intelligent and sustainable lighting.

Co-located with the 2nd Modern Buildings Summit Abu Dhabi, the event will provide a platform for exploring key topics including connected lighting, smart controls, human-centric design, energy efficiency, digital integration, and sustainable lighting solutions. Together, the co-located events will offer attendees a broader perspective on the technologies transforming today’s built environments.

The summit will feature keynote presentations, panel discussions, case studies, and networking opportunities, providing practical insights into the latest advancements in lighting technology and design. Attendees will have the opportunity to engage with industry peers, discover emerging solutions, and explore strategies that enhance performance, sustainability, and user experience across commercial, residential, hospitality, healthcare, and public infrastructure projects.

Bringing together stakeholders from Abu Dhabi’s construction, real estate, infrastructure, hospitality, healthcare, and public sectors, the summit aims to foster collaboration and knowledge exchange while supporting the adoption of innovative lighting technologies and best practices across the built environment.

Event: 2nd Lighting Innovation Summit Abu Dhabi

Date: 9 September 2026

Location: Abu Dhabi, United Arab Emirates

Co-Located With: 2nd Modern Buildings Summit Abu Dhabi

Many of the most-important events have slipped from our collective memories. But their impacts live on.

The sports-car maker delivered 279,449 cars last year, down from 310,718 in 2024.

Meta is facing one of the biggest legal challenges in its history, with thousands of lawsuits over the safety of young users as it ramps up investment in artificial intelligence. The company could face billions of dollars in damages and mounting pressure to make significant changes to its platforms.

5 minMeta Platforms is facing one of the most serious legal threats of its 22-year history—and it couldn’t come at a worse time for the company as it navigates a tricky and costly transition to the artificial-intelligence era.

In March, the company suffered defeats in landmark court cases in California and New Mexico that accused it of giving priority to growth over the safety of its underage users. Thousands more lawsuits by individuals, school districts and more than 40 state attorneys general are pending in state and federal courts. Together, they could put the company on the hook for many billions of dollars in damages and weaken the federal protections that have historically shielded it from liability for harmful content on its platform.

Meta is currently in the midst of a trial over claims by the attorney general of Tennessee, one of dozens of states that have said the company misled its users about the safety of its platform. In August, Meta will go to trial in federal court in Oakland over claims from four attorneys general. In that litigation, the states have asked for damages of up to $1.4 trillion—a sum nearly equivalent to Meta’s $1.5 trillion market capitalization. Another trial in that consolidated set of cases is slated for February.

Recent cases have brought mixed results. In May, Meta settled with a Kentucky school district ahead of a trial planned in Los Angeles. It notched a win this month after the teenage plaintiff in another case dropped his suit without receiving any payment from Meta, after settling with co-defendants YouTube, Snap and TikTok. Meta said it would continue to fight “baseless” lawsuits, noting the plaintiff had created his account only six months before filing the suit.

The lawsuits, which argue that social-media services are designed in ways that cause mental-health problems in young people, are finally getting in front of juries after working their way through courts for years and overcoming attempts by the companies to have them dismissed.

While the personal-injury lawsuits seek only monetary damages, the state and school district cases go further, asking courts to order Meta to alter some of the features and dynamics that have made its products sticky enough to attract 3.5 billion users. With user growth across its family of apps already slowing to a standstill in the first quarter, adverse changes could be punishing to Meta’s core business.

Meta has expressed willingness to work with the states and schools to continue to make its products safe while calling the estimate of more than $1 trillion in damages absurd. “A sanction of that size has no analog in the history of consumer protection enforcement,” the company said in a filing.

Even if that number ends up shrinking, the collective financial impact of the cases could be significant. The company warned investors that a loss in the New Mexico case alone could yield $3.7 billion in damages once the second phase of the trial has concluded.

The timing is far from ideal for Meta, which, after long dominating the market for social-networking services, is racing to retrofit its business to a world in which AI is rapidly becoming the focus of competition. Meta Chief Executive Mark Zuckerberg has said success in this new age is “not a given.”

Meta is planning up to $145 billion in capital spending this year, largely to buy chips and build out its data centers, and earlier this year it laid off 8,000 employees, in part to fund its AI plans. Analysts are expecting the company to report its first quarter of negative free cash flow when it announces its second-quarter earnings Wednesday.

“It comes down to, How can they handle this? How are they prepared to handle this?” said Brian Mulberry, who manages a portfolio at Zacks Investment Management that includes Meta stock. “I do think it’s a real risk for sure.”

Tech analyst Josh Beck, of Raymond James, is taking a wait-and-see approach before deciding what to make of the trials.

“I think it’s something that’s out there. It’s coming up a little bit more,” he said. “But we need to see a little more direction before people become concerned.”

A Meta spokeswoman said in a statement that the company would continue to defend itself vigorously while focusing on providing “safe, age-appropriate experiences parents tell us they want for their teens.”

“Every case is different, and the outcome of one doesn’t dictate the outcome of another,” the spokeswoman said.

Social-media companies have long been insulated from many legal threats because a federal law, Section 230 of the Communications Decency Act, shields them from liability for others’ content on their platforms. Judges around the country, however, are letting many cases go to trial on a theory that says their products are designed intentionally to addict people, sidestepping arguments that rely on claims of harmful content.

Meta has consistently denied wrongdoing in response to lawsuits alleging user harm and in court has pointed to new safety features for teenagers’ accounts and other product changes it has already made as evidence that it is giving priority to safety over growth. It is heavily promoting teen accounts, building stricter supervision controls, putting limits on late-night notifications and installing compulsory break reminders.

Meta has said the litigation is trying to fix a sprawling societal issue with a patchwork of court rulings that, if successful, wouldn’t stop young people from using other types of social media. It has said it would rather address social-media content and design-related issues with federal legislation that applies to the whole industry versus hashing these cases out one-by-one in court. The company plans to appeal the verdicts in Los Angeles and New Mexico.

But the tech giant has shown signs of willingness to compromise. In June, it settled one of the cases slated for trial in federal court, and it raised the prospect of altering some of its platform features as part of the second phase of the trial in New Mexico, where a judge is weighing further damages requested by the state.

Meta’s chief privacy and compliance officer, Michel Protti, testified that the company would be willing to consider changes requested by the state, including making all users under 18 private by default and requiring parent consent to be public and to block notifications during school hours by default, with some exceptions. Meta called many of the requests technically unfeasible, and Protti testified that some had “high potential to grind all our global product development to a halt.”

For Meta, the damages awarded to plaintiffs to date—$6 million to the 20-year-old woman in Los Angeles (split between Meta and YouTube) and $375 million to the state of New Mexico—are a small drop in the bucket for a company that brings in more than $200 billion a year. But it is the precedent the verdicts set that might become an issue.

“You wouldn’t want to keep losing these cases in a row. They make a ton of money, but they could be looking at billions in liability,” said data-privacy lawyer Phil Yannella, who isn’t involved in the lawsuits. “No company is going to ignore that.”

New research suggests that bonuses make employees feel more like a mere cog in a wheel.

Following the successful launch of its Palais Collection, MAISON de SABRÉ has unveiled a new modular handbag system offering more than 720 styling combinations.

Automobili Lamborghini has named Francesco Milicia as its new Marketing Director, effective September 1, 2026. Joining from Ducati, Milicia will lead the brand’s global marketing strategy and strengthen Lamborghini’s position across international markets.

2 minAutomobili Lamborghini announces the appointment of Francesco Milicia as Marketing Director, following Christian Mastro’s transition to his new role as CEO of Automobili Lamborghini America. Effective 1 September 2026, Milicia will lead the brand’s global marketing strategy, contributing to the consolidation of its positioning across international markets.

Francesco Milicia joins Automobili Lamborghini with significant international experience gained in the automotive sector, particularly within Ducati, a company within the Volkswagen Group. During his career he has led business development, commercial growth, digital transformation and organizational change initiatives across global markets. He also lived and worked in Asia for several years, developing a deep understanding of the dynamics and cultures of international markets.

“We welcome Francesco Milicia to Lamborghini as Marketing Director,” said Federico Foschini, Chief Marketing & Sales Officer of Automobili Lamborghini. “His managerial experience, gained in an environment of excellence such as Ducati, combined with the international vision and strategic expertise he has developed throughout his career, will make a valuable contribution to the further strengthening of the brand’s positioning and to supporting the development of our global marketing strategy.”

Holding a degree in Mechanical Engineering from the University of Bologna and a Master of Business Administration, Francesco Milicia completed his executive education across Europe and China at INSEAD, CEIBS and the London Business School.

After beginning his professional career at Ducati in the Operations area, from 2005 to 2012 he gained significant international experience holding various managerial positions in China within a multinational group. At the end of 2012, he returned to Ducati as Managing Director of Ducati Motor Thailand, where he led the implementation of a cutting-edge vertical production process. Returning to Italy in 2015, he joined the Ducati Board of Management as Purchasing Director, before taking on global responsibility for Sales and After Sales activities in 2018.

“Joining Automobili Lamborghini is an honor and a privilege,” said Francesco Milicia. “I have always admired the brand and I am thrilled to contribute to the journey of a company that inspires people around the world through innovation, audacity and uncompromising excellence. I look forward to working alongside the Lamborghini team, learning from their experience and contributing together to writing the next chapter of the brand’s growth and success.”

In his role as Marketing Director, Francesco Milicia will contribute to translating the vision and values of Automobili Lamborghini into marketing strategies capable of enhancing its uniqueness, its constant capacity for innovation, and the distinctive connection the brand creates with customers and enthusiasts around the world.

Parts for iPhones to cost more owing to surging demand from AI companies.

Paine Schwartz joins BERO as a new investor as the year-old company seeks to triple sales.

Alphabet and Tesla kick off this week’s earnings season, with investors closely watching whether heavy AI spending is delivering sustainable returns. Analysts say the results will offer fresh insight into the future of AI investment, cloud growth, and Tesla’s long-term strategy beyond electric vehicles.

2 minAlphabet and Tesla will headline this week’s earnings calendar, with investors looking beyond headline numbers to determine whether billions of dollars in artificial intelligence (AI) investment are translating into sustainable growth, according to Josh Gilbert, Lead Market Analyst, APAC & Middle East at eToro.

“The Magnificent Seven have carried markets for the past two years, but investor patience is clearly wearing thinner,” said Gilbert. “The equal-weighted Magnificent Seven ETF has returned just 1.5% this year compared with 8.7% for the S&P 500, while recent weakness in semiconductor stocks has put AI spending firmly under the microscope.”

Alphabet: AI returns take center stage

Alphabet enters earnings following the strongest market reaction of any Magnificent Seven company last quarter, yet its shares have gained only 1.2% since reporting, well behind the broader market.

Consensus forecasts second-quarter revenue of around USD 117 billion, up 21% year-on-year, with earnings per share expected at USD 2.89.

“For Alphabet, Cloud remains the key growth engine,” Gilbert said. “Cloud revenue grew 63% in the first quarter, and the company’s AI infrastructure backlog has expanded dramatically. Investors will want to see that demand converting into recognized revenue.”

Markets are also expected to focus on Alphabet’s substantial investment program after the company increased annual capital expenditure guidance to USD 180–190 billion and signaled even higher spending next year.

“Three months ago investors were comfortable funding aggressive AI investment,” Gilbert added. “Today they’re asking tougher questions. Markets now want proof that this level of spending will generate durable returns.”

One bright spot remains Alphabet’s AI monetization strategy, with Gemini now exceeding 900 million monthly users.

“The big question is whether AI expands Google’s advertising opportunity or gradually cannibalizes it,” Gilbert said. “That’s likely to be one of the defining themes of this earnings report.”

Tesla: Margins matter more than deliveries

Tesla heads into earnings as the weakest-performing Magnificent Seven stock this year, down 18% year-to-date, despite reporting second-quarter deliveries well ahead of expectations.

The market expects Tesla to report USD 26.3 billion in revenue and earnings per share of USD 0.50.

“Strong deliveries weren’t enough to satisfy investors last quarter,” Gilbert said. “This time the focus shifts squarely to margins and whether the core automotive business remains healthy enough to fund Tesla’s increasingly ambitious AI strategy.”

Consensus expects automotive gross margins, excluding regulatory credits, of 19.5%, although investors will closely examine whether those margins are supported by underlying operations rather than one-off benefits.

“Tesla is increasingly valued as an AI and robotics company rather than simply a car manufacturer,” Gilbert said. “Investors are already paying today for businesses like Optimus and Cybercab, even though meaningful revenues remain several years away.”

With annual capital expenditure expected to reach USD 25 billion, Tesla is prioritizing long-term growth over near-term cash generation.

“Elon Musk has always encouraged investors to think in decades rather than quarters,” Gilbert concluded. “But with AI investment now facing greater scrutiny than at any point in this cycle, this earnings report will test just how much confidence investors still have in Tesla’s long-term vision.”

Two coming 2027 models – the first of the “Neue Klasse” cars coming to the U.S. early next year – have been revealed.

Chris Dixon, a partner who led the charge, says he has a ‘very long-term horizon’

Meta has been dismissed from a lawsuit filed by a Florida teenager who claimed social media harmed his mental health, with the company saying the case was dropped without any payment. The move comes as thousands of similar lawsuits against major social media platforms continue across the US.

2 min

A Florida teen suing social-media platforms over claims their design led to mental health issues dropped his lawsuit against Meta Platforms ahead of a trial slated to begin next week in Los Angeles.

The boy, referred to as R.K.C. in court documents, had previously settled his personal injury lawsuit out of court with TikTok, Snap, and Alphabet’s YouTube. The terms of those settlements weren’t disclosed.

Meta was the only remaining defendant in the trial that was slated to begin Monday. The company said he dropped his case “without receiving any payment.”

“The claims never held up, and this outcome makes clear that we will not back away from defending ourselves against baseless lawsuits,” a Meta spokeswoman said in a statement.

The company previously argued in court documents that R.K.C. used Facebook and Instagram for less than 10 minutes a day on average and had created the accounts only six months before filing the lawsuit.

Lawyers for the plaintiff said in a statement, “R.K.C. came into this process wanting to hold social media companies accountable and push for changes to protect young people like himself. He did that. In light of the overall successful result of the litigation and his concerns about enduring a grueling weekslong trial, he has elected to withdraw his claims against Meta.”

The trial was one of several planned in Los Angeles state court, as more than 3,000 consolidated cases make similar claims against the social-media company. In March, a jury found Meta and YouTube liable for harm to a young woman who testified that her constant use of the platforms led to severe psychological damage. Snap and TikTok also settled that case ahead of trial. A separate jury in New Mexico ruled against Meta as well, for a fine of $375 million. A state court judge there is weighing further damages against the company that could mean it’s forced to potentially pay more and change the way it operates.

Separately, thousands of lawsuits are also consolidated in federal court, where school districts, attorneys general, and individuals make similar claims about the products’ harm to young people. Meta and the other companies settled with a Kentucky school district, averting a trial slated for June.

The first federal trial in the Northern District of California against Meta, YouTube, Snap, and TikTok is scheduled to begin Aug. 18. The trial will center on claims filed by attorneys general in California, Colorado, Kentucky and New Jersey. A total of 29 states are involved in the broader litigation consolidated in the Northern District of California, along with thousands more from school districts and individuals.

Several other states are suing Meta individually, including Tennessee, where a trial began jury selection this week.

Paine Schwartz joins BERO as a new investor as the year-old company seeks to triple sales.

Americans now think they need at least $1.25 million for retirement, a 20% increase from a year ago, according to a survey by Northwestern Mutual

The growing use of GLP-1 weight-loss drugs is raising concerns among eating disorder specialists, who warn they may trigger or worsen anorexia in vulnerable individuals. While medications such as Mounjaro, Wegovy, and Ozempic have transformed obesity treatment, experts say proper screening and monitoring are essential to ensure they are used safely and appropriately.

4 min

When Molly Taylor started taking Mounjaro in the fall of 2024, she marveled at the speed of results. She wasn’t overweight, but she hadn’t been comfortable in her body. Now, she could eat whatever she wanted, just in smaller portions, and people were complimenting her looks. She no longer felt self-conscious.

Then her mindset began to shift.

“I gradually started to worry about what I was eating, how many calories were in it, if it was going to stop me from losing more weight,” said the 23-year-old nanny, who is studying to be a nurse in London. “I think that’s when I was starting to develop anorexia.”

GLP-1s have been hailed as miracle drugs, their rise leading to critical breakthroughs in America’s fight against obesity. Roughly 13 million Americans are now on them, according to research from JPMorgan published in February. The drugs mimic naturally occurring hormones to suppress appetite and cravings and make people feel full. For those who’ve struggled with restrictive eating and anorexia, that can be a tantalizing proposition—and a dangerous one.

Anorexia kills a higher percentage of patients than any other eating disorder, and it is the second most deadly mental illness after opioid addiction, according to data compiled by the nonprofit National Association of Anorexia Nervosa and Associated Disorders.

“I recovered from anorexia myself many years ago, and had this been on the market, I think I certainly would have tried to access it,” said Jennifer Rollin, therapist and founder of the Eating Disorder Center, which is based in Rockville, Md., and provides therapy for patients in seven states.

“Seeing all of the celebrities on the red carpet and so many friends and family members, kind of, bragging about weight loss—that has been a huge trigger for many of the clients I work with,” she said.

Rollin’s business has helped treat people with eating disorders who’ve obtained GLP-1 medications to suppress their appetites, as well as those who were triggered into disordered eating while taking the drugs for approved conditions.

The popularity of Novo Nordisk’s Ozempic, approved for use in 2017 to treat Type 2 diabetes, helped usher in a new wave of GLP-1 drugs that are helping people address chronic weight issues and related problems like sleep apnea and adverse cardiovascular events. Researchers are probing for other applications.

Some doctors say the drugs have as much potential to hurt people with certain eating disorders as to help people with others. The drugs have been used off-label to help with conditions like binge eating and bulimia, which are notoriously difficult to treat.

Jamie Thayer, 48, was prescribed Wegovy for weight loss. “It was like a miracle at first,” she said.

She weighed 240 pounds when she started taking the drug in March 2023, and she rapidly started to shed pounds. She also experienced very low energy, hair loss, severe dizziness, fainting spells from low blood sugar and brain fog. Her son, who had recovered from anorexia, shared his concern with her that Thanksgiving.

“I was really proud of my weight loss at that point,” said Thayer, a Title IX coordinator in Frederick, Md. “I thought I was doing a really good thing.”

When her insurance stopped covering brand-name GLP-1s, she started buying a compounded powder version from China and reconstituting it at home. Meanwhile, her eating became more disordered, governed by strict rules.

“I wouldn’t eat Monday or Tuesday, then on Wednesday I could get a pastry,” she said. “My shot would start to wear off around Saturday, so I usually got some calories on Saturday and Sunday.”

In July 2024, after losing 100 pounds, she checked into a residential treatment center in Connecticut, where she was diagnosed with atypical anorexia and, soon after, re-feeding syndrome, which endangers malnourished people who take on food too fast. She said it saved her life.

Sam DeCaro, director of clinical outreach and education at the Renfrew Center, described a common misconception: that undereating is fine for people who are not considered underweight. In fact, it can be a sign of atypical anorexia, where someone has all the hallmarks of anorexia but is not underweight by body-mass index standards.

“Their undernourishment is causing them all these medical issues, heart issues,” DeCaro said. “It affects every system in the body.”

The rise of telehealth has made it easier than ever for people to obtain pharmaceuticals. Taylor, the nanny in London, said she submitted a doctored photograph of herself that made her look heavier to obtain her prescription. Jessica Scheer, CEO of National Eating Disorders Association, said the organization has heard that some providers don’t screen for a history of disordered eating before prescribing GLP-1s.

The makers of popular GLP-1 drugs have condemned the use of their medications for cosmetic weight loss. The medications don’t warn against using the drugs if you have a history of eating disorders. As with all prescriptions, it is up to care providers to determine whether a medication is right for a particular patient.

“We support our medicines being prescribed to patients who meet the indicated criteria and only promote the FDA-approved indications of our medicines for appropriate patients,” a Novo Nordisk spokesperson said in a statement.

“Patient safety is Lilly’s top priority,” an Eli Lilly spokesperson said in a statement. “As part of our routine safety review process for obesity management and Type 2 diabetes medications, we are working closely with regulators regarding potential safety topics, and we will continue to review data, including any data regarding eating disorders.”

Taylor, who began injecting in October 2024, was hospitalized in May 2025, soon after returning from a vacation. She’d gone about two weeks without eating, and her weight had dropped from 147 pounds to 103.

“I had to slowly re-feed myself and also get all my electrolytes and everything replenished,” she said. She didn’t tell the hospital about her GLP-1 use. “I wanted to carry on losing weight.”

When Mounjaro became harder to get, she sought out the medication through a friend of a friend. This January, she stopped the injections and began going to eating disorder treatment several times a week.

“I still struggle massively, and my weight has continued to go down,” she said. She currently weighs 88 pounds and plans to seek inpatient treatment, as soon as a room becomes available.

Parts for iPhones to cost more owing to surging demand from AI companies.

Interior designer Thomas Hamel on where it goes wrong in so many homes.

Saudi Arabia is strengthening its AI leadership by embedding AI literacy into its national strategy. Backed by Vision 2030 and initiatives such as NSDAI and SDAIA’s SAMAI program, the Kingdom is expanding AI skills nationwide while aligning workforce development with governance, regulatory compliance, and long-term economic growth.

2 min

Saudi Arabia stands out in the GCC for its regulatory maturity and AI readiness, according to a new report from Coursera, which finds that the Kingdom is embedding AI literacy into its national strategy to support economic growth, workforce upskilling, and responsible AI adoption. Initiatives such as the National Strategy for Data and AI (NSDAI), which links national competitiveness to large-scale AI and digital skills development, underscore Saudi Arabia’s advanced policy framework and long-term commitment to AI-driven growth.

The report, Navigating GCC AI Regulation: A Playbook for Building an AI-Literate & Compliant Workforce, examines the regulatory landscape in Saudi Arabia, the UAE, Qatar, Bahrain, and Kuwait. It highlights a distinctive regional approach in which AI literacy is treated not as a standalone skills initiative, but as a strategic pillar that helps organizations meet governance mandates while strengthening the capabilities needed to realize digital transformation ambitions.

Unlike many approaches to AI regulation in Europe and North America, where talent development and policymaking often progress independently, Saudi Arabia’s approach directly links AI literacy to the national goals of Vision 2030, positioning digital skills and workforce preparedness as core drivers of economic diversification.

Kais Zribi, Coursera’s General Manager for the Middle East and Africa, said: “In Saudi Arabia, successful AI adoption is fundamentally dependent on having a workforce equipped with the skills to use these technologies responsibly. With foundational AI proficiency becoming a critical driver for both regulatory readiness and organizational resilience, businesses that proactively prioritize upskilling will be better positioned to navigate evolving regulations, accelerate innovation, and unlock AI’s full value.”

The report notes that organizations are increasingly expected to integrate regulatory requirements into their AI systems, processes, and learning programs from the outset, rather than addressing compliance after deployment. This includes role-based training tailored to privacy obligations, cybersecurity standards, and model governance expectations.

Saudi Arabia is also translating its strategy into action through nationwide initiatives. The Kingdom’s national AI curriculum, introduced in 2025, is reaching six million students and includes guidance on the responsible use of Generative AI (GenAI). Meanwhile, SDAIA’s SAMAI initiative aims to train one million Saudis, with more than half a million already registered. Public-private partnerships are also helping expand access to AI training, with national programs targeting millions of individuals by 2030.

Organizations that fail to invest in AI literacy risk widening internal skills gaps and signaling misalignment with government objectives. In Saudi Arabia, where the government plays a central role as both regulator and a leading adopter of AI, this can affect compliance readiness, procurement opportunities, and long-term competitiveness.

To help businesses respond, the report outlines nine best practices for building an AI-literate workforce. These include embedding AI literacy into governance structures rather than treating it solely as a learning function, assessing AI-related risks and capability gaps, and ensuring learning programs reflect emerging regulatory guidelines.

A central recommendation is to align AI training with Saudization goals and broader workforce planning. By connecting AI upskilling to national talent priorities, companies can strengthen government relationships, support local expertise development, and drive sustainable business value. The report also emphasizes the importance of fostering a culture of continuous learning as technologies advance and regulatory expectations evolve.

Many of the most-important events have slipped from our collective memories. But their impacts live on.

Following the devastation of recent flooding, experts are urging government intervention to drive the cessation of building in areas at risk.

Breitling and Aston Martin have unveiled the Top Time B01 Chronograph 41 Tribute to Aston Martin DB5, a limited-edition collection inspired by the legendary grand tourer. Available in three exclusive versions, the timepieces combine classic automotive design with Swiss watchmaking, powered by Breitling’s Manufacture Caliber 01 movement and featuring handcrafted details that pay tribute to the iconic DB5.

3 min

Introduced in 1963, one of the world’s most iconic on-screen cars, the Aston Martin DB5, became synonymous with British culture, design, and innovation, firmly establishing Aston Martin as one of Britain’s most desirable luxury brands. Today, Aston Martin and Breitling proudly bring that shared legacy to the wrist with the Top Time B01 Chronograph 41 Tribute to Aston Martin DB5, presented in three distinct limited editions.

In the 1960s, the Top Time was Breitling’s unconventional chronograph, created for a new, youthful, speed-driven audience. When a Top Time ref. 2002 appeared on Sean Connery’s wrist in Thunderball (1965), worn alongside the Aston Martin DB5, two icons of the era shared a defining moment in design history. It marked the first Q-modified watch in the James Bond series, and a chapter where speed and style found a common language.

That moment is reinterpreted here through material and form. Wood-inlayed details, hand-colored gradient leather straps, and refined dial executions echo the interiors of the Aston Martin DB5. The result is a watch that captures the feel of being behind the wheel of Aston Martin’s classic grand tourer.

“The Aston Martin DB5 is one of those rare designs that never fades. It still feels as relevant today as it did in the 1960s,” says Georges Kern, CEO of House of Brands (Universal Genève, Breitling, and Gallet). “With this Top Time, we capture that sense of timeless style.”

Marek Reichman, Executive Vice President and Chief Creative Officer at Aston Martin adds: “These editions represent something truly distinct from anything we’ve created before. The collaboration with Breitling brought together two brands with a shared appreciation for timeless design, craftsmanship, and innovation, allowing us to exchange ideas in a way that felt both natural and ambitious. Inspired by the enduring elegance of the Aston Martin DB5 and our shared heritage of iconic design, the watch captures a balance of beauty, precision, and performance. Every detail has been carefully considered to reflect the character and authenticity synonymous with both brands. The result is a watch that feels contemporary today, yet timeless for generations to come.”

Inspired by the timeless elegance of the Aston Martin DB5, every detail of the Top Time Tribute to Aston Martin DB5 brings together two design legacies: the tactile richness of Aston Martin interiors and the modern-retro codes of the Top Time. The cushion-shaped case, grooved corners, and mushroom pushers recall the distinctive profile of the 1960s chronograph, while the “squircle” subdials capture the look of classic car dashboard gauges.

A wooden inner ring draws on the DB5’s steering wheel, and the hand-colored gradient leather strap reflects the depth and tone of fine automotive upholstery. Together, these elements create a watch shaped with the same attention to detail.

“This chronograph blends form with true function,” says Breitling’s Head of Product Design Pablo Widmer. “As with the Aston Martin DB5, its beauty lies in its lines, materials, and finishings.”

The collection is offered in three editions:

- Stainless steel with a silver dial, limited to 1,022 pieces, offers a balanced take that’s closest in spirit to the original Top Time ref. 2002.

- Steel and platinum with a black lacquered dial, limited to 315 pieces, introduces contrast and depth, with the platinum bezel adding weight and presence against the high-gloss black surface.

- 18k red gold with onyx dial, limited to 250 individually numbered pieces, brings an even more elevated expression. The dial is cut from natural onyx, the first use of the stone by Breitling, revealing a unique depth and luster.

Across all three, the design details translate the Aston Martin DB5’s interior craftsmanship into a contemporary chronograph.

Manufacture performance

The engine of the watch is the Breitling Manufacture Caliber 01, a COSC-certified chronograph movement designed for precision and reliability. Its column-wheel architecture and vertical clutch ensure smooth, accurate operation, while a 70-hour power reserve supports extended wear.

Visible through the open sapphire-crystal caseback, the movement is finished with a dedicated Aston Martin–engraved rotor – rhodium-plated or 18k red gold, depending on the version. Each edition pairs this performance with a design language rooted in one of the most recognizable cars ever made.

The Top Time Tribute to Aston Martin DB5 revisits a moment when two distinct approaches to design aligned. One shaped in performance and proportion, the other in precision and form. Together, they continue to be markers of style, that stand the test of time.

Following the successful launch of its Palais Collection, MAISON de SABRÉ has unveiled a new modular handbag system offering more than 720 styling combinations.

Spain defeated defending champions Argentina 1-0 after extra time to lift their second FIFA World Cup title. Ferran Torres’ decisive goal sealed victory in a dominant display, ending Lionel Messi’s World Cup career and capping Spain’s remarkable era as reigning world, European and Olympic champions.

4 min

Ninety minutes of the World Cup final had come and gone, and Argentina—the defending champion, unbeaten at any major tournament since 2019, and blessed by the existence of Lionel Messi—hadn’t managed a single shot.

And yet, on a baking afternoon in front of a hostile crowd, a vastly superior Spain couldn’t find a way to punish them. Even when Argentina was reduced to 10 men, the wave of Spanish jerseys kept crashing into the same resolute defense. Nerves crept in, and as the match entered extra time, Spain began to fear that this final would go down as un robo, a robbery.

Instead, it will be retold as something far more epic than that. This was the day when Spain downed Argentina 1-0 and won the World Cup for the second time.

“Even against 10 men at the end we had to suffer,” Spain coach Luis De La Fuente said. “But, we like to suffer, and I’ll say it again, we were prepared for everything.”

Sixteen years after first lifting the trophy in South Africa, La Roja demonstrated without a doubt that no country commands the world’s most popular sport quite like Spain. With an approach so complete, so technically sound that its players look permanently untroubled, they have shown the world how it looks when cool competence is elevated to high art.

It’s no coincidence that Spain is now a simultaneous Olympic, European, and world champion, or that it currently holds both the men’s and women’s World Cups. This is a nation that has worked out how to develop soccer players as plentifully as it grows oranges and lemons.

When the breakthrough finally came, it arrived with Spain’s 20th shot of the match. After 104 games, the largest World Cup in history had required an extra half-hour to decide its champion and now, in the 16th minute of extra time, Ferran Torres was the man to enter the history books. After a high ball to the back post, headed down by Nico Williams, the 26-year-old Torres lashed it home.

This was the one effort that Argentina goalkeeper Emiliano Martinez, who set a World Cup final record for saves, couldn’t keep out.

But if Spain’s tactics revolved around control, patience, and invention, Argentina’s approach to Sunday focused more squarely on intimidation. And with a permissive referee running the show, Argentina took every inch of latitude—at least until Enzo Fernandez was ejected in second-half stoppage time for a second yellow card.

Over 120 minutes, the defending champions produced just one shot on target but committed 25 fouls. And Messi found himself with precious little to work with—in the first 15 minutes, he had touched the ball just once on the opening kickoff.

Back in 2010, the Netherlands had tried a similar tack against Spain in a World Cup final. Faced with a peak version of the pretty-passing, high-possession, tiki-taka style, the Dutch realized that they simply couldn’t out-soccer La Roja. Their response was to make the match as physical as possible and hope for the best. That time, Spain found a winner in the 26th minute of extra time.

On Sunday, the decisive moment arrived slightly earlier, as the center of the soccer universe migrated to an NFL bowl in a New Jersey parking lot. All at once, it contained President Trump, the King of Spain, and half the royalty of American entertainment.

Mostly, though, the stands heaved with fans from Argentina. Just as they did in Qatar—and more recently in Atlanta and Dallas and Kansas City—supporters in sky blue and white swarmed the stadium, outnumbering Spain fans by at least three-to-one. This is a country where adoration of the national team is so fervent that many fans build their financial planning around the World Cup, taking out loans to buy tickets every four years. It’s also the country with the most psychologists per capita in the world. These facts are perhaps not unrelated.

“The fans are absolutely crazy, different to other countries,” Argentina’s Martinez said before the game. “Seeing them celebrate at 2 a.m. in the cold Argentine weather means a lot.”

But there would be no repeat of those scenes on Sunday night as it lost a World Cup final for the fourth time in its history. Instead, Argentina could only look on as Messi’s World Cup career came to a close with his second defeat in three finals, 12 years after losing his first against Germany.

Only now, the country that defined Messi’s club career over two decades at FC Barcelona, was the one doling out the punishment.

Parts for iPhones to cost more owing to surging demand from AI companies.

Customers can now configure their ideal BMW through natural conversations using the new BMW plugin in ChatGPT. Instead of navigating menus, users simply describe what they’re looking for—whether it’s performance, space, all-wheel drive, or budget—and receive personalized vehicle and configuration recommendations. The AI can refine options, compare models, and link directly to the BMW Configurator or similar in-stock vehicles, making the car-buying journey faster and more intuitive.

2 min

BMW is expanding its digital customer communications by making its vehicle configurator available directly via OpenAI’s ChatGPT. Using the BMW plugin in ChatGPT, customers can now engage in a natural conversation to configure their dream car. The plugin combines the dialogue capabilities of generative AI with the BMW product and configuration knowledge base, and is available on both mobile devices and desktop computers.

Dialogues rather than menu navigation.

Generative artificial intelligence is changing the way people search for information online and make decisions. Dialogue-based systems are increasingly replacing traditional navigation via search engines or websites. Picking up on this trend, BMW is the first car manufacturer to offer digital vehicle advice directly via ChatGPT.

Generative AI meets BMW knowledge base.

The BMW plugin in ChatGPT is focused on AI dialogues. Instead of step-by-step navigation through menus and submenus, users describe their requirements in natural language – for example, in terms of spaciousness, ground clearance, powertrain or intended use. They are then given suggestions of suitable models and configurations based on this information. This also makes it very easy to compare different configurations.

The recommendations can be adjusted, compared and refined at any time in the dialogue. Factors like running costs, driving dynamics, colour, model or all-wheel drive can be specifically taken into account during the consultation. For complex specification requirements in particular, dialogue-based interaction opens up new, easy and intuitive ways to refine individual vehicle configurations. The desired vehicle specification can then be opened in the BMW Configurator. Customers can also view stock vehicles that have a similar spec.

All recommendations are based on the latest BMW Configurator data. Should any questions arise that go beyond its database, ChatGPT can also access up-to-date information from the internet, to the extent the relevant functions are available and enabled.

Easy access via ChatGPT.

The BMW plugin is integrated directly into ChatGPT. On chatgpt.com, it can be accessed by going to the “Plugins” menu item and then searching for “BMW”. On mobile devices, access is much the same when logged in, via the “Plugins” option in the main menu.

New research suggests that bonuses make employees feel more like a mere cog in a wheel.

Parents and educators across the United States are increasingly calling for the return of longer school recess periods, as growing evidence highlights their role in improving children’s mental well-being, concentration, and social development. With several states introducing laws to expand recess time, experts argue that play is no longer a luxury but a fundamental part of learning and academic success.

4 min

When Kathryn Truman’s son Sawyer enrolled in kindergarten, she was surprised to discover his school only gave him 20 minutes of recess a day. The 40-year-old nurse worried he wouldn’t get enough of a mental and physical break.

Truman wasn’t the only one who felt this way. She teamed with other parents to help revive recess throughout Tennessee, which went on to pass a law last year requiring at least 40 minutes of recess in elementary schools. Now, Truman is looking to expand recess in middle schools and helps lead a nonprofit—Say Yes to Recess—with chapters in 20 states.

“Of course we want our kids to be good at math and reading, but what kind of people will they grow up to be? That’s determined at recess,” said Truman, explaining the benefits for children’s social development.

In Michigan, Shanel Talbert said she got involved in the fight for recess when her daughter’s elementary school reduced it last year. While her daughter wasn’t struggling academically, Talbert could see that she was burned out from her seven-hour school day.

Talbert and other parents launched a petition, calling for at least 60 minutes of recess, that has garnered over 1,300 signatures. They are working with a state legislator on a bill that would require 40 minutes of recess in elementary school, which Talbert said they thought was more likely to pass.

Morning and afternoon recesses were common in U.S. elementary schools during the post-World War II decades. But as pressure mounted on schools to improve test performance in the 2000s, many reduced or eliminated recess in favor of more instructional time in subjects such as reading and math. States often prescribe minimum instructional hours, and recess generally doesn’t count.

Chicago Public Schools was among the first big-city school districts to restore daily recess in 2012, after many of its elementary schools did away with it. But the effort was slow to catch on broadly.

Pediatricians have been sounding the alarm, saying recess has both mental and physical benefits. In May, the American Academy of Pediatrics expanded its endorsement of recess beyond elementary schools to include middle and high schools. Research suggests that at least 20 minutes a day with multiple breaks is best, the AAP says.

Catherine Ramstetter, co-author of that recommendation, said recess helps children remember information and learn better. It also allows young children to develop interpersonal skills.

Ramstetter upholds the Finnish model in which students typically get 15 minutes of recess multiple times a day. “The importance of recess as time to connect with one another cannot be understated,” she said. “Adults ideally are not intervening in the play but close by so they can intervene when necessary.”

In Oklahoma, legislators recently pushed for more recess time as part of an effort to improve learning and test results that has also included banning cellphones during school and emphasizing phonics, according to Republican state Sen. Ally Seifried.

Seifried drafted a law that passed in April requiring 40 minutes of daily recess in kindergarten through fifth grade, up from 20 minutes. “Parents who had little boys definitely recognized the importance of this,” she said.

Krissy West, a school physical therapist and mother from New Hampshire, started advocating for more recess last year, after seeing her daughter Daisy get overwhelmed, sometimes resulting in tantrums after school.

“She would say that [her] whole body is just ready to run,” said West. As a coping mechanism later on, her daughter, now 10 years old, would ask the teacher for permission to take bathroom breaks, time she would then use to take a walk through the hallways.

A bill West championed, which would have required 45 to 60 minutes of recess for K-6 students, was defeated on New Hampshire’s House floor earlier this year amid concerns it would violate existing teacher contracts by requiring extra staff.

The “Say Yes to Recess” initiative calls for at least 60 minutes of screen-free time daily when children get to pick their activities, and that it isn’t withheld as punishment. The hourlong recommendation is based on research from Texas Christian University on the optimal time needed for children to reduce stress and anxiety, improve test scores and fight obesity.

West and other parents have helped push for change locally at Valley View Community School in Farmington, N.H. This past academic year, the elementary school added a 25-minute recess block starting from 7:30 a.m., when parents can drop their children off. The start of classes was moved 10 minutes later to help accommodate it.

West said recess first thing in the day isn’t ideal and noted part of it became optional in practice because some children wouldn’t arrive until later. But she is encouraged that the school is trying to find solutions.

The school’s principal, Mark Dangora, said adding more downtime is still a work in progress. He is trying to bring daily recess time to a total of 50-55 minutes. Losing a bit of class time, so far, hasn’t affected learning, he said.

“Children need play,” said Dangora.

The sports-car maker delivered 279,449 cars last year, down from 310,718 in 2024.

KnowBe4 and AWS have signed a multi-year strategic agreement to strengthen digital workforce security, helping organizations protect both employees and AI agents while simplifying the deployment of cybersecurity solutions through AWS Marketplace.

< 1 min

KnowBe4, a leader in digital workforce security, securing both AI agents and humans, today announced it has signed a multi-year strategic collaboration agreement (SCA) with Amazon Web Services (AWS) to help organizations worldwide adapt to an evolving cybersecurity landscape, while simplifying how they procure, deploy and scale security solutions.

As cyber threats become more sophisticated and AI adoption accelerates, workforces are expanding to include both humans and AI agents. At the same time, security teams are under pressure to improve outcomes and operate more efficiently. By accessing KnowBe4’s industry-leading portfolio in AWS Marketplace, customers can streamline procurement and accelerate deployment at a time when speed is more critical than ever.

“Today’s workforce consists of both humans and AI agents working side by side, and securing both is the defining challenge of this moment,” said Marco Muto, SVP of Strategy at KnowBe4. “This agreement reflects a shared commitment from KnowBe4 and AWS to meet that challenge together. We’re jointly investing in the go-to-market, our technology, and the broader industry ecosystem to ensure our customers have what they need to stay ahead of an evolving threat landscape. When two industry leaders align around a common mission, customers win.”

KnowBe4 will collaborate with AWS on global go-to-market initiatives, sales enablement and customer adoption programs designed to help organizations proactively manage risk across their evolving workforce while simplifying procurement in AWS Marketplace. It also creates new opportunities for KnowBe4’s global ecosystem of channel partners, helping to align security investments with broader cloud strategies.

New research suggests that bonuses make employees feel more like a mere cog in a wheel.

Don’t just hear about the future of longevity, experience it. Revive ME returns to Abu Dhabi, bringing together the innovators, leaders, investors, policymakers, and visionaries shaping the next era of healthy lifespan. This is where breakthrough science meets transformative innovation. Where meaningful conversations spark collaboration, new ideas become actionable opportunities, and the global longevity ecosystem comes together under one roof.

< 1 min

Abu Dhabi will welcome healthcare innovators, investors, policymakers, researchers, and technology leaders when Revive ME 2026 returns to ADNEC Marina on 11–12 November 2026, bringing together the latest advances in longevity science, regenerative medicine, biotechnology, AI-powered healthcare, and personalised wellness.

Positioned as the Middle East’s premier longevity and health technology exhibition and conference, the two-day event aims to showcase how scientific breakthroughs and emerging technologies are transforming the future of healthy ageing. Building on the success of its inaugural edition, Revive ME 2026 will provide a platform for collaboration between clinicians, startups, investors, research institutions, healthcare providers, and government stakeholders to accelerate innovation across the sector.

Visitors can expect an extensive exhibition featuring next-generation health technologies, live product demonstrations, expert-led conference sessions, startup showcases, networking opportunities, and discussions exploring the future of preventive healthcare, precision medicine, regenerative therapies, digital health, biotechnology, and artificial intelligence. The event is designed to foster partnerships that drive innovation while addressing one of healthcare’s fastest-growing global priorities: extending healthy lifespan.

As governments and private sector organisations continue investing in healthcare innovation, events such as Revive ME reinforce Abu Dhabi’s position as a regional hub for medical technology, life sciences, and future-focused healthcare solutions. By bringing together global experts under one roof, the exhibition seeks to encourage knowledge exchange, investment, and cross-sector collaboration that can shape the next generation of health and wellness technologies.

Registration for Revive ME 2026 is now open.

New research suggests that bonuses make employees feel more like a mere cog in a wheel.